Economics for Managers

Economic Indicators

Power consumption as Economic Indicator

Rescission & Recovery

MOAT

Headwind vs Tailwind

Understanding Economic Jargon : Central Banks

Explain how fiscal policy affects aggregate demand and aggregate supply.

Fiscal expansion: An increase in government spending or a decrease in taxes (i.e., a budget deficit) leads to an increase in GDP and an increase in prices. Fiscal restriction or contraction: A decrease in government spending or an increase in tax leads to lower prices and lower output/GDP. (The aggregate demand curve shifts left.) Counter cyclical: Change in policy (i.e., budget deficit or surplus) by government will offset changes in aggregate spending by consumers and investors and lead to smooth fluctuations in the business cycle. For example, if an economy is in recession then plan a budget deficit.

Describe why fiscal policy should be timed properly and why timing is difficult.

There's usually a time lag between when policy is needed and when its recognized by policy makers; there's also a lag between when the need is recognized and when its instituted, and a lag between when policy is adopted and when its impact is felt. The use of fiscal policy to calm the business cycle is very difficult; it may accentuate the corrective action of the economy rather than correct the problem for which it was intended. Automatic stabilizers are built in fiscal devices which ensure deficits in a recession and surpluses during a boom. Three types: unemployment compensation; corporate profit taxes and progressive personal taxes (e.g. In a recession, when tax receipts are low, increasing transfer payments and reducing tax revenue will cause an automatic deficit to occur and therefore help to alleviate high unemployment).

Discuss the impact of expansionary fiscal policy based on:

The basic Keynesian model: An increase in government spending and/or a decrease in taxes (i.e., a budget deficit) will be magnified by the multiplier process and lead to an increase in aggregate demand. If the economy is operating below full capacity, this will lead to an increase in GDP and employment.

The Crowding-Out model: The effect of an increase in the budget deficit will be dampened as borrowing for the deficit will increase interest rates and crowd out private spending and investment, leading to a decrease in investment. In an open economy the increase in interest rates leads to an increase in foreign investment--capital inflow--and an increase demand for domestic dollars, producing an increase in exchange rates--currency appreciation--and a decline in net exports and a decrease in aggregate demand.

The New Classical model: The effect of an increase in the budget deficit will be dampened because households will anticipate higher future taxes implied by the debt and reduce their spending and increase their saving to pay for them; this will crowd out private spending. An alternative explanation - an increase in government spending leads to increase in aggregate demand, which is crowded out by a decrease tax effect. A decrease in taxes leads to an increase in savings (as consumers expect tax to increase) and therefore leads to a decrease in consumption. A decrease in taxes leads to an increase in loanable funds, leading to an offset government demand for money. A decrease in taxes leads to unchanged aggregate demand and interest rates.

The Supply-Side model: A decrease in marginal tax rates leads to increase in investment and savings, an increase in work and productivity, a decrease in leisure, and a decrease in tax sheltering, leading to an increase in aggregate supply in the long run (LR), an increase in GDP, a decrease in unemployment and a decrease in prices.

Keynesian model: Increase in government spending or decrease in taxes will be magnified by the multiplier and lead to an increase in aggregate demand.

Crowding out model: Effect of increase government spending is dampened because borrowing to finance the budget deficit will push up interest rates and crowd out private spending and investment.

New classical model: Effect of increase government spending is dampened because households anticipate higher future taxes implied by the debt and reduce their spending to pay for them, which will crowd out private spending.

Supply-side model: A decrease in marginal taxes will increase the increase the incentive to earn and improve the efficiency of resource use, leading to an increase in output in the long run.

Identify the relationships among budget deficits, inflation, and interest rates.

An increase in government spending (i.e., a budget deficit) leads: (1) to an increase in the demand for loanable funds, placing upward pressure on the real rate of interest (according to crowding out model) and (2) with higher expected taxes, to a decrease in spending and the stimulation of savings, thereby permitting government to expand its borrowing at an unchanged interest rates (according to New Classical model). There is a mixed opinion on the relationship between a budget deficit and interest rates.

Central Bank is said to have taken a "dovish stance" if it believes that low interest rates are necessary in order to promote growth in the economy. In such a scenario, the bank is not particularly worried that low interest rates may cause inflation down the road.

Repo (Repurchase) rate is the rate at which the RBI lends shot-term money to the banks. When the repo rate increases borrowing from RBI becomes more expensive. Therefore, we can say that in case, RBI wants to make it more expensive for the banks to borrow money, it increases the repo rate; similarly, if it wants to make it cheaper for banks to borrow money, it reduces the repo rate

Reverse Repo rate is the rate at which banks park their short-term excess liquidity with the RBI. The RBI uses this tool when it feels there is too much money floating in the banking system. An increase in the reverse repo rate means that the RBI will borrow money from the banks at a higher rate of interest. As a result, banks would prefer to keep their money with the RBI

Monetary Policy Committee Minutes

Posted by Neil Irwin on December 16, 2013 http://www.washingtonpost.com

Slowdown, Recission

Tailwinds & Headwinds

Monetary Policy : Central Bank Stance on Interest rates : Dovish vs Hawkush , hard landing vs soft landing

Central Banks can take either a Dovish or Hawkish stance towards interest rates.

Central Bank is said to have taken a "dovish stance" if it believes that low interest rates are necessary in order to promote growth in the economy. In such a scenario, the bank is not particularly worried that low interest rates may cause inflation down the road.

The opposite of a dove is a "hawk".Hawks are very worried about inflation and will usually advocate higher interest rates in an effort to head off said inflation.

How Easy is it to identify whether a bank is Hawkish or Dovish

Often central banks give a dovish guidance going forward but remain hawkish for the time being or vice versa. Sample the below words from interview by Raghuram Rajan , Governer Reserve Bank of India :

To a specific question as to why the policy stance is hawkish while its guidance dovish, Rajan said his deputy, Urjit Patel, referred to the central bank as being neither a hawk nor a dove but an ‘owl’, signifying wisdom and alertness, when it comes to monetary policy formulation.

Often central banks give a dovish guidance going forward but remain hawkish for the time being or vice versa. Sample the below words from interview by Raghuram Rajan , Governer Reserve Bank of India :

To a specific question as to why the policy stance is hawkish while its guidance dovish, Rajan said his deputy, Urjit Patel, referred to the central bank as being neither a hawk nor a dove but an ‘owl’, signifying wisdom and alertness, when it comes to monetary policy formulation.

Hard Landing of interest rates vs Soft Landing

The economy of a country is healthy when it experiences good levels of consumption and

investments and when the mood of the people is exuberant. These are times when the economy experiences growth. As growth rates increase due to high consumer demand, prices of goods and services start to rise. This is an inflection point because the gates of the economy open up to inflation. Hereafter the central bank starts to apply the brakes by raising interest rates to start slowing down the economy gradually. Here the word, "gradually" assumes a lot of significance because the job of regulating interest rates by the central bank is indeed a very delicate one.

To understand this a little better, just imagine if the pilot were to inadvertently apply the brakes of the aircraft too hard. The consequences of such an action could be very damaging and the pilot could lose control over the aircraft causing it to skid and crash. Thus the pilot needs to regulate the brakes in such a manner that the aircraft lands smoothly.

In the same way, the central bank raising interest rates is akin to applying the brakes of the aircraft. If an increase in interest rates are regulated well, then slowly but steadily the economy will slow down and inflation will gradually get harnessed. Otherwise, the economy can go out of control and experience a sudden slowdown caused by undue negative sentiments, sudden slowdown in investments and slowdown in consumption and so on and so forth. This would cause immense pain in the economy due to low capacity utilization, job losses, and defaults, etc. This pain caused by mismanagement of the monetary policy is termed as "hard landing" of the economy.

What is Repo rate and Reverse Repo rate?

Repo (Repurchase) rate is the rate at which the RBI lends shot-term money to the banks. When the repo rate increases borrowing from RBI becomes more expensive. Therefore, we can say that in case, RBI wants to make it more expensive for the banks to borrow money, it increases the repo rate; similarly, if it wants to make it cheaper for banks to borrow money, it reduces the repo rate

Reverse Repo rate is the rate at which banks park their short-term excess liquidity with the RBI. The RBI uses this tool when it feels there is too much money floating in the banking system. An increase in the reverse repo rate means that the RBI will borrow money from the banks at a higher rate of interest. As a result, banks would prefer to keep their money with the RBI

Thus, we can conclude that Repo Rate signifies the rate at which liquidity is injected in the banking system by RBI, whereas Reverse repo rate signifies the rate at which the central bank absorbs liquidity from the banks.

The Reserve Bank of India (RBI) has increased repo rate (rate at which banks borrow from RBI for short-term) by 25 bps to 6% and reverse repo rate (rate at which RBI borrows money from banks) by 50 bps to 5%.

The Reserve Bank of India (RBI) has increased repo rate (rate at which banks borrow from RBI for short-term) by 25 bps to 6% and reverse repo rate (rate at which RBI borrows money from banks) by 50 bps to 5%.

Manoj: I have heard recently that Mr. Rajan has reduced Repo Rate by 50 basis points and everyone is saying that this is good for the market. Loan EMI may also come down. What is this rate cut means actually? I want to understand this.

Vinit: To understand this you first need to know, how does a bank function.

Manoj: Why?

Vinit: Because all these are inter-related. Tell me – what does a bank do?

Manoj: Bank takes money from depositors and gives loan to earn interest. That way they keep everyone happy and make a profit also.

Vinit: Correct, but there are more to it. Let me explain this in a very simplistic way. Bank needs money. Bank can get money from depositors like you and me and also from RBI. But bank also needs to pay certain interest to us and also to RBI.

Manoj: Ok.

Vinit: Let us try to understand first – what happens when we deposit, say, Rs. 100 with a bank.

Manoj: I know that. Bank gives that Rs. 100 to someone who needs a loan.

Vinit: No, it is not that simple. Remember, though bank can earn interest by giving away loans, but it is also very risky. There are many cases of loan defaults. This way banks can put all our money into high risk areas. It has to be protected.

Manoj: How?

Vinit: Ok, RBI has made it mandatory that upon receiving, say, Rs. 100 – banks first have to deposit Rs. 4 with RBI. RBI keeps this Rs. 4 in its current a/c and hence banks do not receive any interest on this money. This is known as Cash Reserve Ratio or CRR, which is currently at 4%.

Manoj: Hmmm, then?

Vinit: RBI has also made it mandatory that upon receiving, say, Rs. 100 – banks need to compulsorily buy central and state govt. securities of Rs. 21.50. Of course banks will earn some interest income here. This is known as Statutory Liquidity Ratio (SLR), which is currently at 21.50%.

Manoj: Ok, so you mean to say that upon receiving Rs. 100, banks can spend only Rs. 74.50 at its own will.

Vinit: Correct. 100 – (4 + 21.50) = 100 – 25.50 = 74.50

Manoj: But you were saying that banks can also borrow from RBI. What interest banks pay to RBI?

Vinit: Before 30th September, banks were paying 8.25% interest to RBI when it borrows money from RBI. Now this rate has been reduced by 50 basis points. So banks now need to pay interest to RBI, if it borrows from RBI, at the rate of 7.75%. This is known as Repo Rate.

Manoj: Can fixed deposit rate be affected by reduction of Repo Rate?

Vinit: Of course. If banks get money from RBI @7.75%, why will banks pay higher interest to you and me? One year FD rate is already revised by many banks and it is equal to or very close to 7.75%.

Manoj: But as now banks are getting money at a cheaper rate, then they should reduce the loan interest rate i.e. passing on the benefits it receives.

Vinit: Correct. They should. And on that hope market is cheering. If companies get loan at a cheaper rate, they will likely to expand their businesses. That will create more jobs, more income and boost the economy.

Manoj: How is inflation linked to this?

Vinit: See, when loan becomes cheaper, people tends to borrow more. That means people will have more money to spend. This will increase the demand for goods, and if supply does not increase to match this demand, then prices will increase.

Manoj: So there is a chance, that inflation may rise also?

Vinit: Well, yes. But inflation depends on many other factors as well, like production (industrial and agricultural), manufacturing, export – import, foreign currency movement etc. So inflation may increase or may not.

Manoj: One last question. Like we deposit our money with banks, can banks also deposit their money with someone?

Vinit: Yes, they can deposit with RBI and earn interest too. This interest is typically 1% less than the repo rate. This rate is known as Reverse Repo Rate.

Manoj: Great! So now I understand CRR, SLR, Repo Rate, Reverse Repo Rate and their impact on deposit rate, loan interest rate and on inflation. Thanks.

Its a lengthy post .. but a good read (for all those who arent a master of economics. . Its a fowarded post and to make it more interesting names have been added). Spread the knowledge.

Quantitative Easing

The magic word on Wall Street for much of this year has been "taper." And so it is again this week, as the Federal Reserve meets to consider whether to do exactly that. Here's what you need to know.

What is tapering?

Slow down! First you have to understand the Fed's practice of buying bonds, known as quantitative easing or QE.

Okay, okay. What's QE?

The Fed normally manages the economy by either raising or lowering short-term interest rates. But it can't cut that rate below zero, where it has been for almost five years. So the Fed has tried to stimulate the economy by pumping money directly into the financial system.

It does that by buying longer-term bonds, both U.S. Treasury bonds and mortgage-backed securities issued by government sponsored companies Fannie Mae and Freddie Mac. The Fed creates money out of thin air (the electronic equivalent of printing money) and uses it to buy the bonds on the open market. Then the bonds are on the Fed's books, and the newly created money is out in the banking system.

The hope is that that extra money will find its way into other stuff. The investors who otherwise would have bought those treasury bonds and mortgage-backed securities instead have to by corporate bonds, for example, or invest it in the stock market. This has the effect of making people wealthier (because stock and bond prices are bid up) and encouraging spending and investment (because long-term interest rates are lower, for example on mortgage loans and business borrowing costs).

That's the theory, anyway. The results are more subject to dispute. The Fed's QE policies likely helped end the economic collapse in 2009, but it is less clear how much they have helped in speeding up growth in the years since then.

Currently, the Fed is buying $85 billion worth of bonds each month. The Fed's total holdings, as of Dec. 11, topped $4 trillion, compared with around $800 billion before the financial crisis.

So NOW can you explain what the taper is?

Yes! The Fed doesn't want to end the bond-buying cold turkey. It wants to slow the purchases gradually, and at a pace that can be adjusted depending on how markets and the economy react to the process. It wants to taper them off, not just end them.

The question is when to start tapering. Back in June, Chairman Ben S. Bernanke suggested the Fed would start tapering the bond buying later in 2013 and end them altogether perhaps in the summer of 2014. Markets were ready for the tapering to begin at the September Fed policy meeting, but the committee surprised markets by holding off.

The Federal Open Market Committee is meeting Tuesday and Wednesday, and it will be debating whether to begin tapering QE at the meeting. The committee will announce its decision Wednesday afternoon at 2 p.m. Eastern time, followed by a news conference by Bernanke. Markets will be holding their breath.

What's the case for tapering now?

It goes like this: QE isn't meant to go on forever, and so you need to start winding it down sometime. That sometime may as well be now.

The policy seems to be having diminishing benefits, in the sense that going from, say, $3.5 trillion to $4 trillion in assets on the Fed balance sheet didn't help markets and the economy as much as going from $2.5 trillion to $3 trillion. And it may be creating some unhappy side effects, like bubbles in emerging market bonds or for some types of corporate debt.

And the economic recovery is looking a good bit more solid than it did when the Fed met in September, averaging nearly 200,000 net new jobs a month this past fall. The unemployment rate is down to 7 percent, from 7.6 percent in June. After the confidence-rattling government shutdown in October, there is now a budget deal nearing passage that will prevent more shutdowns for the next two years and lessen the amount of drag fiscal policy is putting on the economy.

And the Fed is looking to shift its approach to stimulating the economy away from bond buying, and toward using communications about the future path of interest rates. In theory, if the central bank can successfully persuade people that it won't raise interest rates until the distant future, that should have the same impact on the economy as buying bonds, without some of the nasty side effects mentioned above.

Back in June, that subtle message wasn't getting through. Markets interpreted any wind-down of QE as also sending a message that rates will be hiked sooner. But in the months since then, dozens of Fed speeches have helped persuade markets that they really are different tools and that the end of QE doesn't mean that higher interest rates are imminent.

Against that backdrop, it's time to start the wind-down. That's what the pro-taper folks will argue at the meeting, anyway.

What are the arguments against tapering now?

Oh, sure, they will say, there have been a couple of months of decent economic data. But we've seen this show before. Every time the economy seems to be getting out of its rut, the Fed starts heading for the exits, and things get worse. We need to see a little more evidence that this faster recovery is truly entrenched before we even think about ending QE.

Second, even with growth looking a little better, inflation is still way too low -- only 1.1 percent by the Federal Reserve's preferred measure (the price index for personal consumption expenditures excluding food and energy). The Fed says it aims for 2 percent inflation; and to start winding down the money-printing operation when inflation is still too low could cost the central bank credibility. People might start to believe that the Fed isn't really serious about maintaining 2 percent inflation, making Japan-style deflation more likely.

Finally, don't be so sure that the battle to separate short-term interest rates from QE is won. Yes, there's been some clear progress on that front in the past few years, but if we seem too eager to pull away the punch bowl of bond buying, markets will inevitably assume we will do the same for low-interest-rate policies.

So is there away the people making these arguments might compromise?

There are. For example, Fed officials could agree to begin tapering bond purchases, but to start small (like reducing from $85 billion to $80 billion or $75 billion). They could announce plans to begin the tapering a month or two down the road, not immediately.

And they could consider tapering the bond buying, but complementing it with new strategies to try to bolster the credibility of their communications. For example, they could say, "Whoops, we're not going to think about raising interest rates when unemployment is 6.5 percent, as we've been saying for the past year. We'll wait until it's 6 percent." Or they could state that they have a lower bound for inflation, that they won't hike rates as long as inflation looks on track to be below, say, 1.5 percent.

In other words, if they do taper, there's a good chance it will be in conjunction with other steps to affirm the Fed's seriousness about trying to stimulate the economy.

Wait, isn't Bernanke on the way out as chairman? How does that affect things?

He is! His term is up Jan. 31, and Janet Yellen, the current vice-chair, is expected to be confirmed as early as this week to follow him. Technically that changes nothing. Bernanke is chairman until he isn't, and has to do what he thinks is best for the U.S. economy. But in practice, Yellen will likely be a more influential voice around the committee table than she would be otherwise (and she was already one of the most influential voices). It's a safe bet that whatever decision the Fed makes on Wednesday, Yellen will agree with it.

So what are they going to do?

Nobody knows for sure! It looks to be a close call. That's what will make Wednesday afternoon interesting for anybody who cares about the economy or markets. Stay tuned!

The dual Mandate of Federal Reserve Bank of US as against Single mandate for other central Banks

The U.S. Constitution gives Congress ultimate power over monetary policy. (“To coin Money, regulate the Value thereof.”) Congress created the Federal Reserve System in 1913 after more than a century of various monetary experiments. The system originally consisted of 12 regional banks, all equal in stature and each with its own board of directors, along with a Federal Reserve Board to coordinate and supervise the regional banks.

Unfortunately, the Fed’s regional, decentralized structure made it difficult, if not impossible, to conduct coherent monetary policy during the Great Depression. This led to reforms enacted in the Banking Act of 1935. In particular, the Federal Reserve Board became the Board of Governors of the Federal Reserve System, with seven members appointed by the president and confirmed by the Senate, and was given power to set national monetary policy. The regional banks became, in effect, branches of the Federal Reserve that carried out the board’s policies.

The Fed conducts monetary policy through open market operations, which consist of buying and selling Treasury securities to maintain a target level of interest rates. The specific interest rate targets are set by the Federal Open Market Committee (FOMC), and are chosen to either speed up or slow down the economy. For instance, by cutting interest rates the Fed makes it cheaper for businesses and households to borrow and thus encourages more spending.

The Fed’s policy objectives were spelled out by Congress in 1978 by what is known as the Humphrey-Hawkins Full Employment Act. The act created what has come to be known as the Fed’s dual mandate, since it requires the Fed to promote both maximum employment and stable prices.

The dual mandate sets the Fed apart from most other central banks, which focus exclusively on inflation in order to maintain stable prices. By contrast, Congress requires the Fed to set monetary policy in such a way as to keep both the inflation rate and the unemployment rate low and stable. The dual mandate also leads to friction within the Fed as governors and presidents put different weights on the importance of inflation versus unemployment in economic health.

Fixation with fixation of fiscal deficit.

Who’s afraid of fiscal deficit?

The fear of rising government deficits is based on a number of dubious assumptions

Why this obsession with fiscal deficit, a layperson tuning into talk shows on the Budget may well wonder.

She would have been surprised by the emphasis on fiscal correction in an election year — a government apparently disinterested in winning elections and focusing on book-keeping niceties instead!

If our layperson had followed Budget discussions over the years, she would have been struck by auto and telecom industrialists ‘expressing concern over fiscal deficit’. Has fiscal deficit (the difference between total government expenditure and total receipts, excluding borrowings) become an intellectual fetish, or is there something more to it?

The Finance Minister said in his Interim Budget, “Analysts and rating agencies had acknowledged our efforts (in containing the ‘twin’ deficits — fiscal and current account) some months ago and no longer speak about a downgrade.”

The statement betrays both a sense of relief and intent to pursue further fiscal correction in future Budgets, so that the ‘global investor’ hangs in there. Why is the global investor fixated about fiscal deficit?

Three reasons

The global investor fears a higher fiscal deficit for its assumed impact on inflation, interest rates and, finally, the domestic currency.

First, she feels that higher government expenditure will drive up interest rates by squeezing the availability of funds for private investors — the ‘crowding out’ effect, in other words. As an equity investor — and there is more foreign money coming into equities than debt — she would be worried about the impact of high interest rates on profitability.

The second fear is of public spending directly causing inflation by injecting money without the matching output, leading not just to an erosion in real returns in the present but also the fear of further erosion in the future. The latter is seen to impact ‘business confidence’.

The third fear is of inflation and general chaos due to a chain effect: higher public spending driving up demand for imported goods and services, widening the current account deficit and depreciating the currency -- impacting dollar returns on every rupee invested.

Hence, a steep fall in the rupee hurts the equity market, as foreign institutional investors expecting a further fall pull out, raising prospects of currency panic as in mid-2013. On the real economy side, inelastic energy imports add to the trade imbalance. In sum, we might be left with a negative spiral in both the real economy and the financial sector.

This is the twin deficit hypothesis — a higher fiscal deficit leads to a higher current account deficit and higher costs for the economy as a whole, besides a sense of uncertainty. Therefore, the industrialists at talk shows, and the FIIs and rating agencies, fear a higher fiscal deficit for its possible impact on inflation, interest rates and the exchange rate. How valid are their concerns?

Shallow basis

Whether public spending leads to ‘crowding out’ or actually spurs private spending (‘crowding in’) depends on the nature of such spending. Alok Sheel, a member of the Prime Minister’s Economic Advisory Council and a reformist like any other, observes that public spending in infrastructure will spur private investment. This could relieve inflation caused by supply constraints.

The belief that public spends in India vanish into a black hole, creating money but no goods, need not always hold true. The improvement in the network of national highways did spur the economy in the Tenth Plan by crowding ‘in’ investment.

If supply-side bottlenecks are addressed, the demand generated by public spending could generate investment, jobs, growth and higher taxes without much of a time lag, thereby ensuring that a higher fiscal deficit in one period is recovered in the next.

So, there is no reason to assume that a deficit will turn into a looming threat. Besides, to forgo the benefits of more jobs now for a vague dread of the future does not seem tenable.

The twin deficit hypothesis is open to question. A higher deficit on government account may not translate into more imports, if the people choose to save rather than spend.

A paper by Suparna Basu and Debabrata Datta (Does Fiscal Deficit Influence Trade Deficit, Economic and Political Weekly, July 23, 2005) shows that the two deficits have not moved together in India between 1985 and 2003. While our savings rate has fallen in recent years, raising twin deficit concerns, the decline can be arrested by generating jobs and keeping food prices in check. An economy where the growth of savings exceeds that of investment will not face a twin deficits problem.

Now, we come to the fear of the future — that we don’t know how a high fiscal deficit could impact us later, even if we are fine with it right now; hence the erosion of ‘confidence’.

It is this undefined dread that drives the ‘austerity’ argument in the US and Europe — and it was taken apart by economists such as Paul Krugman, Robert Pollin, Arjun Jayadev and many others.

Even Sheel observes at a recent lecture at IIM-B: “The last thing that policymakers should do is aggravate an economic slump by cutting back government demand when private demand is slack in an attempt to keep the nominal fiscal deficit unchanged.”

Ethical issues overlooked

It does not end here. There are crucial ethical and ideological debates to be considered. One side argues that government spending alone can reduce inequality (a view in the US), while the other maintains that public spends are unproductive.

There is an ethical and even economic case — the demographic dividend argument — for prioritising outlays on health and education on the same footing as ‘infrastructure’, as Amartya Sen has argued. The Interim Budget does not reflect this philosophy at all.

The mainstream discourse on fiscal deficit is largely confined to the expenditure side. The government is attacked more for raising expenditure on ‘populist’ heads than for its inability to lift the tax-to-GDP ratio. The revenues forgone by announcing tax exemptions run into lakhs of crores.

Are our panelists on the TV show tuned in to all this?

Feb 23, 2014 09:02 PM , By A SRINIVAS . thehindubusinessline.com

Crony capitalism is a term describing an economy in which success in business depends on close relationships between business people and government officials. It may be exhibited by favoritism in the distribution of legal permits, government grants, special tax breaks,. Crony capitalism is believed to arise when political cronyism spills over into the business world; self-serving friendships and family ties between businessmen and the government influence the economy and society to the extent that it corrupts public-serving economic and political ideals.

It is used world wide to describe virtually any governmental decisions favoring "cronies" of governmental officials.

trickle down theory: increases in the earnings of the rich are good for the poor also.

Proponents of these policies claim that if the top income earners invest more into the business and it will in turn lead to more goods at lower prices, and create more jobs for middle and lower class individuals.Proponents argue economic growth flows down from the top to the bottom, indirectly benefiting those who do not directly benefit from the policy changes.

Slowdown, Recission

Concept of Foreign Exchange parity

The term "tailwinds" describes some condition or situation that will help move growth higher. For example, falling gas prices will help a delivery company be more profitable. Lower gas prices is said to be a tailwind for the freight services industry.

"Headwinds" are just the opposite. Its a situation what will make growth more difficult. For example, if the price of beef goes much higher, McDonald's is facing headwinds.

It's a nautical term. If the wind is at your back (tailwind), that will help you move forward more quickly. If you are moving into a headwind, that will only make progress more difficult.

Economic Measures

Can we express all that is happening within a country with just one number : GDP

Forget GDP - Use Big Data

No single number has become more central to society in the past 50 years than GDP — Gross Domestic Product. Throughout the world, it has become a proxy for success and for failure. It is a profoundly important indicator. It is also a profoundly flawed one.

This past Friday, the U.S. government released its revised estimate for GDP for the last three months of 2013. That showed growth to be less than was initially reported last month, with the figure falling to 2.4% from 3.2%.

That is a considerable difference, yet such revisions are hardly unusual. The number will be further revised in the coming months, and may be subject to alteration years, even decades later, as final bits of data get assimilated and as methods of assessing the nation’s output change over time. Last July, after years of work, the Bureau of Economic Analysis declaredthat the U.S. economy was, in fact, hundreds of billions of dollars larger than previously reported because of changes in the way intellectual property and research were counted.

The variability of these numbers should be a hint that they do not capture some sort of absolute reality. They describe this thing we call “the economy,” but the economy is not a physical entity with a set topography. It is itself a product of man-made numbers and statistics, and its contours change and morph. GDP very purposefully excludes whole swaths of human existence, from domestic work to volunteer activities to cash transactions not recorded by the government.

You wouldn’t know that, however, from most popular debates and discussions. While the creators of the national accounts that gave us GDP and Gross National Product understood that these numbers were inventions not intended to measure happiness, well-being, or all aspects of material life, that distinction has inexorably been lost as the number become the primary marker of political success and national greatness.

The limitations of GDP have long been recognized. In 1968, just before his assassination, Robert Kennedy made a passionate plea to stop using GNP (GDP’s older cousin) as an absolute measure of national greatness. As a metric of how much stuff a country makes, it performed its task. But “it does not allow for the health of our children, the quality of their education, or the joy of their play….It measures everything except that which makes life worthwhile.”

In the more than 45 years since that speech, there has been a steady chorus pointing out the limitations of GDP. The Kingdom of Bhutan was the first — and still the only — country to reject GDP as its primary measure and instead developed a Gross National Happiness index. The United Nations, drawing on the work of Nobel economist Amartya Sen, created a Human Development Index that weighted other factors such as education and life expectancy. In 2008, the president of France, Nicolas Sarkozy, convened a commission to go beyond GDPthat recommended a broader “dashboard” of variables to measure the health of a nation.

Academics have also joined the post-GDP party. Innovative economists such as Erik Brynjolfsson of MIT have drawn attention to how the information technologies and services that now contribute substantially to economic dynamism just aren’t adequately captured by GDP. These “free goods of the Internet,” as Brynjolfsson and others have called them, may contribute hundreds of billions to national output but are essentially invisible in our calculations.

And finally there are the endless revisions and tweaking of the number itself. As British economist Diane Coyle has so astutely observed, GDP may often be treated as if it were a natural phenomenon, but it is not. It is an invention, created by all-too human economists and politicians in the crucible of the Great Depression and World War II. It shed light on what had been too mysterious, namely the output of a nation, and it helped the United States and Great Britain fight and win World War II by devoting massive amounts of domestic industry to making machines of war without unduly imperiling domestic economic life.

The largest problem with GDP, however, is not its limitations (however considerable they are) but the maximalist use of it by economists, politicians, and the general public who use it as a stand-in for national success. That is not the fault of the indicator. It is the fault of those who demand that it carry more weight than it can or should bear.

Few if any businesses will see their forward strategy meaningfully determined by GDP. Even large industrial companies such as Caterpillar and GE will find pockets of strength even when GDP is weak, and they will encounter issues even when it is strong. The traditional relationship between GDP and interest rates, inflation, and now employment has clearly broken down. A factory today might employ 500 people and 20 robots and add substantially to GDP, whereas the same factory 40 years ago would have employed thousands. Basing future plans based on those 20 century patterns is likely to be a grave mistake.

It would be an even bigger mistake for disruptive companies such as Amazon or Google. GDP might be weak, and overall advertising spending contracting with it, yet Google can still see massive growth as it disrupts a traditional industry. The same goes for Amazon, which can thrive even if GDP and consumer spending sag as long as that spending shifts away from malls and toward the mailbox.

In short, we are all becoming less dependent on this number called GDP. In an age of big data, companies have a wealth of information at their fingertips. That information — about customers and their behavior, about what clients need and where — matters far more than broad-brush national numbers like GDP.

It’s not that we need new national indicators. We need numbers that matter for the questions we have. No one will win a Nobel Prize for such bespoke indicators, but we will all prosper by using GDP less and using the other numbers around us more.

Zachary Karabell is Head of Global Strategy at Envestnet, a financial services firm, and author of The Leading Indicators: A Short History of the Numbers that Rule Our World(Simon & Schuster, 2014). This essay is adapted from the book and first appeared on theHarvard Business Review site.

Head of Global Strategy at Envestnet, Inc

Inflation measure in India is WPI.It consists of 435 commodities

What is inflation?

Inflation rate is the rate at which prices of goods and services increase in its economy. It is an indication of the rise in the general level of prices over time. Since it's practically impossible to find out the average change in prices of all the goods and services traded in an economy due to the sheer number of goods and services present, a sample set or a basket of goods and services is used to get an indicative figure of the change in prices, which we call the inflation rate.Mathematically, inflation or inflation rate is calculated as the percentage rate of change of a certain price index.

How does India calculate inflation?

In India, inflation is calculated on a weekly basis. India uses the Wholesale Price Index (WPI) to calculate and then decide the inflation rate in the economy.WPI was first published in 1902, and was one of the more economic indicators available to policy makers until it was replaced by most developed countries by the Consumer Price Index in the 1970s.WPI is the index that is used to measure the change in the average price level of goods traded in wholesale market. In India, a total of 435 commodities data on price level is tracked through WPI which is an indicator of movement in prices of commodities in all trade and transactions. It is also the price index which is available on a weekly basis with the shortest possible time lag only two weeks. The Indian government has taken WPI as an indicator of the rate of inflation in the economy.

How is WPI (Wholesale Price Index) calculated?In this method, a set of 435 commodities and their price changes are used for the calculation. The selected commodities are supposed to represent various strata of the economy and are supposed to give a comprehensive WPI value for the economy.WPI is calculated on a base year and WPI for the base year is assumed to be 100. To show the calculation, let’s assume the base year to be 1970. The data of wholesale prices of all the 435 commodities in the base year and the time for which WPI is to be calculated is gathered.Let's calculate WPI for the year 1980 for a particular commodity, say wheat. Assume that the price of a kilogram of wheat in 1970 = Rs 5.75 and in 1980 = Rs 6.10The WPI of wheat for the year 1980 is,(Price of Wheat in 1980 – Price of Wheat in 1970)/ Price of Wheat in 1970 x 100i.e. (6.10 – 5.75)/5.75 x 100 = 6.09Since WPI for the base year is assumed as 100, WPI for 1980 will become 100 + 6.09 = 106.09.In this way individual WPI values for the remaining 434 commodities are calculated and then the weighted average of individual WPI figures are found out to arrive at the overall Wholesale Price Index. Commodities are given weight-age depending upon its influence in the economy.

How is inflation rate calculated?If we have the WPI values of two time zones, say, beginning and end of year, the inflation rate for the year will be,(WPI of end of year – WPI of beginning of year)/WPI of beginning of year x 100For example, WPI on Jan 1st 1980 is 106.09 and WPI of Jan 1st 1981 is 109.72 then inflation rate for the year 1981 is,(109.72 – 106.09)/106.09 x 100 = 3.42% and we say the inflation rate for the year 1981 is 3.42%.Since WPI figures are available every week, inflation for a particular week (which usually means inflation for a period of one year ended on the given week) is calculated based on the above method using WPI of the given week and WPI of the week one year before. This is how we get weekly inflation rates in India.

Characteristics of WPI

Following are the few characteristics of Wholesale Price Index:

• WPI uses a sample set of 435 commodities for inflation calculation

• The price from wholesale market is taken for the calculation

• WPI is available for every week

• It has a time lag of two weeks, which means WPI of the week two weeks back will be available now

Inflation measure in India is WPI.It consists of 435 commodities

What is inflation?

Inflation rate is the rate at which prices of goods and services increase in its economy. It is an indication of the rise in the general level of prices over time. Since it's practically impossible to find out the average change in prices of all the goods and services traded in an economy due to the sheer number of goods and services present, a sample set or a basket of goods and services is used to get an indicative figure of the change in prices, which we call the inflation rate.Mathematically, inflation or inflation rate is calculated as the percentage rate of change of a certain price index.

How does India calculate inflation?

In India, inflation is calculated on a weekly basis. India uses the Wholesale Price Index (WPI) to calculate and then decide the inflation rate in the economy.WPI was first published in 1902, and was one of the more economic indicators available to policy makers until it was replaced by most developed countries by the Consumer Price Index in the 1970s.WPI is the index that is used to measure the change in the average price level of goods traded in wholesale market. In India, a total of 435 commodities data on price level is tracked through WPI which is an indicator of movement in prices of commodities in all trade and transactions. It is also the price index which is available on a weekly basis with the shortest possible time lag only two weeks. The Indian government has taken WPI as an indicator of the rate of inflation in the economy.

How is WPI (Wholesale Price Index) calculated?In this method, a set of 435 commodities and their price changes are used for the calculation. The selected commodities are supposed to represent various strata of the economy and are supposed to give a comprehensive WPI value for the economy.WPI is calculated on a base year and WPI for the base year is assumed to be 100. To show the calculation, let’s assume the base year to be 1970. The data of wholesale prices of all the 435 commodities in the base year and the time for which WPI is to be calculated is gathered.Let's calculate WPI for the year 1980 for a particular commodity, say wheat. Assume that the price of a kilogram of wheat in 1970 = Rs 5.75 and in 1980 = Rs 6.10The WPI of wheat for the year 1980 is,(Price of Wheat in 1980 – Price of Wheat in 1970)/ Price of Wheat in 1970 x 100i.e. (6.10 – 5.75)/5.75 x 100 = 6.09Since WPI for the base year is assumed as 100, WPI for 1980 will become 100 + 6.09 = 106.09.In this way individual WPI values for the remaining 434 commodities are calculated and then the weighted average of individual WPI figures are found out to arrive at the overall Wholesale Price Index. Commodities are given weight-age depending upon its influence in the economy.

How is inflation rate calculated?If we have the WPI values of two time zones, say, beginning and end of year, the inflation rate for the year will be,(WPI of end of year – WPI of beginning of year)/WPI of beginning of year x 100For example, WPI on Jan 1st 1980 is 106.09 and WPI of Jan 1st 1981 is 109.72 then inflation rate for the year 1981 is,(109.72 – 106.09)/106.09 x 100 = 3.42% and we say the inflation rate for the year 1981 is 3.42%.Since WPI figures are available every week, inflation for a particular week (which usually means inflation for a period of one year ended on the given week) is calculated based on the above method using WPI of the given week and WPI of the week one year before. This is how we get weekly inflation rates in India.

Characteristics of WPI

Following are the few characteristics of Wholesale Price Index:

• WPI uses a sample set of 435 commodities for inflation calculation

• The price from wholesale market is taken for the calculation

• WPI is available for every week

• It has a time lag of two weeks, which means WPI of the week two weeks back will be available now

Economics with 2 cows

SOCIALISM

You have 2 cows.

You give one to your neighbour.

COMMUNISM

You have 2 cows.

The State takes both and gives you some milk.

FASCISM

You have 2 cows.

The State takes both and sells you some milk.

NAZISM

You have 2 cows.

The State takes both and shoots you.

BUREAUCRATISM

You have 2 cows.

The State takes both, shoots one, milks the other, and then throws the milk away…

AN AMERICAN CORPORATION

You have two cows.

You sell one, and force the other to produce the milk of four cows.

Later, you hire a consultant to analyse why the cow has dropped dead.

A FRENCH CORPORATION

You have two cows.

You go on strike, organise a riot, and block the roads, because you want three cows.

A JAPANESE CORPORATION

You have two cows.

You redesign them so they are one-tenth the size of an ordinary cow and produce twenty

times the milk. You then create a clever cow cartoon image called ‘Cowkimon’ and market it worldwide.

A GERMAN CORPORATION

You have two cows.

You re-engineer them so they live for 100 years, eat once a month, and milk themselves.

AN ITALIAN CORPORATION

You have two cows, but you don’t know where they are.

You decide to have lunch.

A RUSSIAN CORPORATION

You have two cows.

You count them and learn you have five cows.

You count them again and learn you have 42 cows.

You count them again and learn you have 2 cows.

You stop counting cows and open another bottle of vodka.

A CHINESE CORPORATION

You have two cows.

You have 300 people milking them.

You claim that you have full employment, and high bovine productivity.

You arrest the newsman who reported the real situation.

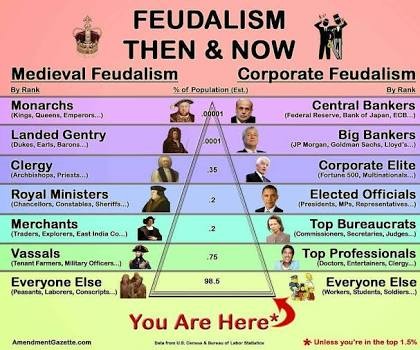

Feudalism

2015 Nobel for Economics

Princeton University economics professor Angus Deaton was awarded the 2015 Nobel Prize in Economic Sciences "for his analysis of consumption, poverty, and welfare," the Royal Swedish Academy of Sciences said Monday. Deaton, born in 1945 in Edinburgh, earned his Ph.D from the University of Cambridge, U.K., in 1974, and has been a professor of economics and international affairs at Princeton since 1983. "To design economic policy that promotes welfare and reduces poverty, we must first understand individual consumption choices. More than anyone else, Angus Deaton has enhanced this understanding," according to a statement from the Nobel committee.

2013 Nobel in Economics

2013 Nobel in Economics

Shiller

The Royal Swedish Academy of Sciences lauded the economists' research on the prices of stocks, bonds and other assets, saying "mispricing of assets may contribute to financial crises and, as the recent global recession illustrates, such crises can damage the overall economy."

"This financial crisis that we've been going through in the last five years has been one that seems to reveal the failure to understand price movements," Shiller said.

Bubbles are created when investors fail to recognize when rising asset prices become detached from underlying fundamentals.

Shiller and other economists warn that prices in some markets have risen too far, too fast due to the Fed's ultra-easy monetary policy. The benchmark U.S. Standard & Poor's 500 index hit a record in September, though it is generally not considered overvalued based on expectations for corporate earnings results or economic growth.

Shiller's work led him to suggest in 2005 that the U.S. housing market might be overheating. He helped create a closely watched gauge of housing prices, the S&P Case/Shiller Index.

In June this year, he pointed to a potential new housing bubble in some of America's largest cities.

"It is up 12 percent in the last year. This is a very rapid price increase right now, and I believe that it is accelerated somewhat by the Fed's policy," he said.

Central bankers traditionally try to avoid targeting asset bubbles with a blunt instrument like interest rates. But the severe harm done when a bubble bursts means that, in the United States at least, they are thinking more broadly about the unintended consequences of their monetary policy decisions.

"When asset prices are getting way out of line it should be cause for alarm. The monetary authorities should lean against extreme asset price movements," Shiller said.

The bubbling housing market is not mainly the result of central bank policy, but reflects a shift toward "a more speculative attitude," Shiller said. "We cannot expect monetary policy to cure all of these problems."

Hansen struck a more cautious note. "We often underestimate how much uncertainty there is in terms of our understanding of the economy," he said. "If you pretend that we know more than we do, you are in danger of constructing policies that can be counter-productive."

FAMA DIFFERENT THINKING ON MARKETS

The Royal Swedish Academy of Sciences said the laureates' insights "provide guidance for the development of theory as well as for professional investment practice".

Fama, tipped as a Nobel winner for many years, has been called the father of modern finance and is well-known for research showing certain groups of stocks tend to outperform over time, and for thinking about markets as efficient.

This view of how assets are priced is at odds with Shiller's belief that investors can fall prey to "Irrational Exuberance," the title of his 2000 book, shortly before the bursting of a global bubble in information technology stocks.

Hansen, who voiced caution about the ability of economists to spot asset bubbles in advance, said there were different ways to interpret evidence.

"In terms of overall understanding I guess there is a sense in which one could view them as complimentary," he said of the research of his co-winners. "But right now, they would both have very different guesses about what is the right set of models going forward," he said in an interview.

Fama and Hansen are professors at the University of Chicago, while Shiller is a professor at Yale University. Collectively, with research spanning decades, their work helped the emergence of index funds in stock markets, the award-giving body said.

Peter Englund, professor of banking at the Stockholm School of economics and member of the prize committee, said their research had deeply influenced modern finance.

"The most obvious application, that follows on from Fama's research, is the insight that you can't beat the market. It is impossible to prove that equity analysis is worth the money," he told Reuters.

"That has led to the development of index funds and that most households actually put their savings in index funds."

Why fall in crude is bad in a way for India - eventhough apperently it is good

Excerpts from the interview to CNBC-TV18 on Tuesday:

"Right now if oil goes to USD 65 or even slightly lower it is not a big negative but it does imply that there is going to be a lot of weakness in external demand and countries in Latin America like Venezuela which already have a very difficult situation, emerging markets like Russia and of course the Middle Eastern countries plus some of the European economies like the UK and Norway that rely on oil exports to a significant extent are going to be facing fairly difficult situations.

This will affect their budgets and their current account balances which in turn will affect their consumption demand. So, softness in consumption demand is ultimately not good for anybody in the world including India. So, there is a point at which falling oil prices are not going to be a net plus even for India. I don‘t think we are quite there yet but we are pretty close."

According to Emkay Global‘s Dhananjay Sinha, the sharp decline in crude oil price will lead to loss of tax revenue and dividend payouts by oil PSU companies, which together will outweigh reduction in oil subsidy.

"Annual contribution of the Oil & gas sector to the exchequer of around Rs 3 lakh crore is much higher than oil subsidy burden," Sinha said in a note to clients last week.

"On an overall basis, every 10 percent decline in global commodity prices results in 600 basis points decline in gross tax collection & rise in the revenue deficit/GDP (States & GoI) by 110 basis points. Meeting the FY15 Budget estimate of 4.1 percent fiscal deficit/GDP would call for cuts in spending or raising taxes, thereby compromising growth," the Emkay note said.

India‘s oil import bill for October fell 19 percent year-on-year, but there was bad news as well by way of lower exports. Exports contracted for the first time this fiscal, declining 5 percent year-on-year.

Most economists expect export growth for the rest of this year to be subdued because of the weakness in Europe, Japan and lastly China, which could try to export itself out of the slowdown it is facing. In addition, low crude prices are hurting oil producing countries, which in turn could further hurt global demand.

A couple of weeks back, Nigeria devalued its currency to offset reduced revenues from oil exports. This led to Bajaj Auto having to hike the prices of its motorcycles sold in Nigeria. Some analysts feel the move could hurt Bajaj Auto‘s sales in that market, which accounts for around 35 percent of its export revenues.

Protectionism for domestic ecosystem, level playing field with foreign rivals

Chinese Dumping in India

Steel 6-Feb-2016

Govt raises the wall for steel imports

The government on Friday imposed minimum import prices (MIPs) on specific steel products to protect domestic players from cheap imports from China and other countries. Integrated domestic primary steel producers such as Sajjan Jindal-led JSW Steel, Jindal Steel & Power, state-owned Steel Authority of India and Tata Steel would be among the largest beneficiaries.

The move, however, would not apply to the stainless steel sector. Also, import for American Petroleum Institute (API)-grade steel used in the petroleum and natural gas industries are exempted from the MIP.

MIPs are valid for six months only, which could trigger uncertainty in the market. But a government official said these may be extended further.

For ingots, billets, blooms and slabs, MIP now stands at $362, $352 and $341 per tonne, respectively. Similarly, various flat-rolled products of iron or non-alloyed steel (of a width of 600millimetres or more) will now attract different MIPs - in the range of $445 to $752 per tonne. Hot-rolled bars and rods, of iron, non-alloyed steel as well as alloyed steel, will also face MIP of around $450 per tonne.

"We certainly welcome the move and hope that they (government) extend it beyond six months," Ravi Uppal, chief executive officer, Jindal Steel told Business Standard. Indian steel companies also hinted at price revision post the MIP imposition. "We will need to check the gap between the MIP level and the distressed local steel price and then perhaps a correction will happen in the local prices," Uppal added. The MIP notification - issued by the Directorate General of Foreign Trade (DGFT) - is valid for six months.

"We certainly welcome the move and hope that they (government) extend it beyond six months," Ravi Uppal, chief executive officer, Jindal Steel told Business Standard. Indian steel companies also hinted at price revision post the MIP imposition. "We will need to check the gap between the MIP level and the distressed local steel price and then perhaps a correction will happen in the local prices," Uppal added. The MIP notification - issued by the Directorate General of Foreign Trade (DGFT) - is valid for six months.

"We may extend the timeline of six months, if needed. It was clear that our domestic industry was not getting the benefit of safeguard duty and anti-dumping duty," said a senior steel ministry official.

On September 14 last year, the government imposed a 20 per cent provisional safeguard duty for 200 days on the import of hot-rolled flat products in coils of a width of 600 mm or more.

Moreover, on December 11 last year, the government imposed anti-dumping duty ranging from 5 to 57 per cent on cold-rolled flat products of stainless steel for a period of five years. The duty was imposed on imports from China, South Korea, European Union, the US, South Africa, Thailand and Taiwan.

Steel companies had witnessed poor earnings in the December quarter as realisations took a hard hit because of increased imports despite a five per cent increase in domestic demand. "With this measure now, domestic steel producers should be able to grab some share in the increasing domestic demand, from which we were completely off due to cheap imports," Uppal said.

N C Mathur, president, Indian Stainless Steel Development Association (ISSDA), said the government's move may "slightly" help the ailing steel sector. However, he was disappointed that the stainless steel sector was left out. "We are again disappointed that stainless steel products have been left out of the ambit of MIP mechanism. It is noteworthy that stainless steel industry faces exactly similar danger of what the carbon steel sector does… As a result of excessive imports, almost all stainless steel players are under severe financial stress," Mathur said.

Meanwhile, Sanak Mishra, secretary general at Indian Steel Association said, the government has covered quite a few important products such as hot-rolled coil, sheets and strips along with cold-rolled products. He said it was the right move for the domestic steel industry.

The consumer segment, however, is not happy with as it fears a price hike in steel products in the range of Rs 3,000-5,000 per tonne in the next 3-5 months. Moreover, the consumer segment, whose input cost will shoot up significantly, also faces the threat of closedown, leading to rise in non-performing assets for the banks.

"MIP imposition is going to show its impact in the next 4-5 months when manufacturing sector shrinks and NPAs rise for banks in a much bigger way," said Nikunj Turakhia, head of the Bombay Iron Merchants' Association board.

ALUMINIUM 8/9/2015

As per the data from industry body Aluminium Association of India in last three years, LME

(London Metal Exchange) prices have come down by 35 percent to USD 1,660 per tonne in June, 2015 from a peak of USD 2,555 a tonne in June 2011.

Total imports to India have grown by more than 159 percent to 1,563 kilo tonnes (KT) in 2015 as against import of 881 KT in 2011, mainly from China and Middle-Eastern nations. This has led to imports accounting for 56 percent of Indian aluminium consumption in 2014-15, while products of Indian producers account for only 44 percent. China, which possesses more than 50 percent of world's aluminium production, is now exporting over 20 percent of its products and their exports to India have surged by 200 percent in 2014-15 fiscal compared to 2010-11.

To capture global markets and gain competitive edge over its rivals, China offers its companies indirect subsidies like power tariff discounts of around USD 200 a tonne to aluminium smelters, 13 percent value added tax rebate on exports and favourable terms of credit. In view of the above the primary producers are urging the government to raise the basic customs duty on aluminium as they are being adversely affected due to cheap imports from China, Middle East.

On 19th Aug 2015,the government said the demand by primary producers to raise import duty is a "tricky" case as the move will help the bigger players - Hindalco , Balco, Nalco and Vedanta - but may hurt smaller firms that import scrap.

The Ministry is reviewing the case for increasing import duty on aluminium and has met with both the primary producers as well as the small companies who import aluminium scrap for various purposes. "In this case there are two things. On one side there are firms who are importing scrap. On the other hand primary players are only four - Hindalco, Vedanta, Balco and Nalco -- who tell us to raise the import duty on Aluminium." "But if we increase it then the firms who import scrap will be adversely affected. They have also come to us and said that import duty should not be increased as it will adversely impact them," Mines Secretary Balwinder Kumar told agency.

He added that the ministry is monitoring the situation and reviewing the demand of both the groups. It is a tricky situation. So there are conflicting interests. We had a meeting with the primary producers and asked them to provide us their results of the first quarter of this fiscal so that we can accordingly decide. "So that we can see what view the ministry has to take. We are awaiting response from the primary metal manufacturers. So we have to see how we have to balance this," Kumar said.

Chinese Dumping in India

The move, however, would not apply to the stainless steel sector. Also, import for American Petroleum Institute (API)-grade steel used in the petroleum and natural gas industries are exempted from the MIP.

MIPs are valid for six months only, which could trigger uncertainty in the market. But a government official said these may be extended further.

For ingots, billets, blooms and slabs, MIP now stands at $362, $352 and $341 per tonne, respectively. Similarly, various flat-rolled products of iron or non-alloyed steel (of a width of 600millimetres or more) will now attract different MIPs - in the range of $445 to $752 per tonne. Hot-rolled bars and rods, of iron, non-alloyed steel as well as alloyed steel, will also face MIP of around $450 per tonne.

Indain Domestic Power Equipment Manufacturers unable to compete with China

To halt Chinese imports, Govt to bar yuan borrowings for power sector

In a move aimed at protecting domestic power equipment manufacturers from the onslaught of cheap Chinese imports funded by low-cost yuan credit, the Government has decided to withdraw the External Commercial Borrowings (ECB) in Chinese currency for power plants.

Currently, Indian companies are allowed to raise such loans up to a limit of $1 billion.

“The Reserve Bank of India will soon issue a notification to this effect,” a senior Government official told Business Line. He also disclosed that RBI Governor D. Subbarao had informed about this move in his reply to a letter from Heavy Industries Minister Praful Patel’s letter, written in May, demanding such a step.

However, the move may not immediately solve the domestic power equipment sector’s woes. The official also disclosed that so far, there has not been even a single proposal for ECB in yuan received by the Government. That is why it was reviewed in a recent meeting of high level committee, which accordingly decided to discontinue it.

Although the Government has always maintained that such borrowings were meant for all purposes, there was a widespread belief that this facility was introduced mainly for the power sector.

In fact, the original decision to allow yuan ECBs was taken considering the huge shortage of power in the country.

“Since power is a basic necessity and a national priority, it was considered important to support ECB in Chinese currency route for the import of capital goods for the power sector,” the official added.

ECB refers to commercial loans from overseas lenders. It can be in the form of bank loans, buyers’ credit, suppliers’ credit or securitized instruments (e.g. floating rate notes and fixed rate bonds, non-convertible, optionally convertible or partially convertible preference shares). The minimum average maturity of such loans is three years. ECB is usually considered cheaper compared with domestic loans.

In his letter to Subbarao, Patel had said, “It is apprehended that availability of long-term, low interest export credit from China will further distort the status in favour of Chinese manufacturers, who have already gained almost 50 per cent share in the Indian power generating equipment market.”

He further mentioned that this matter had already been taken up with the Finance Minister.

“I am bringing this to your notice, as the Master Circular No. 12/2012-13, dated July 2, 2012 on this subject has been issued by the Reserve Bank of India. I would request you kindly to look into the matter and consider withdrawal of the aforesaid circular for power plants with immediate effect,” he said.

Patel’s Ministry is the nodal one for the capital goods industry, which includes power generating equipment companies. Industry sources feel that cheaper imports, funded by cheaper finance for Chinese companies, are adversely affecting domestic manufacturing companies.

Meanwhile, domestic companies got some relief last year, when import duty was raised on imported equipment.

Inter-corporate rivalries and international corporate rivalries at play?

Sajjan Jindal, chairman and managing director of JSW Steel says exports will soar because of the depreciation of the rupee while opposing the reported move to lower duties on iron ore exports. In the course of an hourlong interview with ET's Satish John and Anirban Chaudhary, Jindal criticises tribal affairs minister KC Deo for supposedly seeking to keep tribal communities in a primitive state. Edited excerpts:

Is the manufacturing sector taking advantage of the weakened rupee?

The devalued rupee is a huge fillip. Last year, we exported 1.5 million tonnes of steel. This year, we may cross four million tonnes.

Everybody I was speaking to from my peer group, including Bharat Forge's Baba Kalyani, are all cranking up their manufacturing plants. We are 22% more competitive today because of the depreciating rupee. Steel is a global commodity.

India is not a player of significance in the global market. The total steel traded is 150 million tonnes a year. Japan does 60 million tonnes, South Korea does 30 million tonnes and India does 4 million tonnes. And this year we may do 10 million tonnes.

So, where are these exports happening?

For the first time in our history we are exporting to South Korea and Japan. After a gap of 10 years we are exporting again to China. We are also exporting to Europe and the US.

Doesn't China have an over-capacity?

Today, they are not exporting steel. They are consuming all their steel. Suddenly, the Chinese demand has picked up and their economy seems to have again revived. They consume 10 times more steel than what India consumes.

Do you agree that much of India Inc's problems are its own making?

Inter-corporate rivalry in the corporate sector brings its own pressure in Delhi. You instigate the NGOs and the media picks up. They hype it up. The judiciary picks up and does their bit. Then pressure builds up and investigative agencies get into the act. And, because the leadership is weak, every agency (overreaches).

We have so much of coal in our country (referring to the fallout of the Coalgate scam). We are now importing 200 million tonnes of coal. We are a poor nation and we cannot meet our energy requirement based on imports and we have so much coal deposits lying with us. It will last us for more than 100-200 years. And, coal will lose its relevance in 50 years and it will not be needed because new competing technologies such as nuclear, solar and wind will become more competitive.

Your industry has seen a lot of activity from NGOs. Is it inter-corporate rivalry?

The civil society is needed in every economy. They are a balancing act. They are not there in China. But, at times, they say no tree must be cut and that tribals must remain tribals. Please ask them whether the tribals want to remain a tribal. But the poor tribal does not know. He wants status quo. The case in point is the (Anil Agarwal's) Vedanta Resources in Niyamgiri. In my view, it is a real disaster for all of us.

So, who is behind such NGOs?

There are inter-corporate rivalries at play and there are international corporate rivalries.

International?

India is a country which is best placed to produce aluminium in the world. Two states — Andhra Pradesh and Odisha — are best suited for this. We have the best quality bauxite in the world. We have the largest reserves in steam grade low-quality coal in the world and the cheapest.

These are the two key inputs to make aluminium. And, we have abundant manpower who are keen to have jobs and we have enough water. China never had bauxite and imports coal and produces 20 million tonnes of aluminum and India produces less than two million tonnes of aluminium.

Do you think the Chinese are behind this?

No. It is the Canadians and the Americans. This has been going on for the last fifty years. They don't want this. Late Aditya Birla used to openly say before. Everything is done by the big multinational aluminum companies. It is so cheap to do this. Just imagine you hire 20 NGOs to support them through another NGO. All the names are there.

Which international NGO supports which NGO in India?

The NGOs in America and Canada feed 20 NGOs . They spend Rs 40-50 crore a year. They'll ensure that no aluminum project will come up in India.

What happened to JSW Aluminium. Have you shelved it?

Yes, we have shelved it. Because our tribal affairs minister says tribals must remain tribals. I can't understand this. We have done everything and everyone supported us. We have done gram sabhas, acquired land, given shares of our land to land losers in Andhra Pradesh.

The mining will be done by APMDC and the product will be sold on a cost-plus basis, which is an international concept. Royalty will be paid at international levels. Moreover, there is not a single tree to be cut during the mining activity.

So, there's no ecological impact from the mining. The Supreme Court has approved it and the green bench has approved it. But now ( Krishna Chandra) Deo says tribals will be affected. How will they get affected? Let tribals operate this and get all the money.

There is a feeling that to strengthen the rupee, one strategy is to open up iron ore exports? Are you in favour?

Not at all. India used to export 120 MT. Goa used to export 50 MT. Karnataka exported 40 MT and 30 MT was exported by Chhattisgarh, Jharkhand and Odisha together. Today, Goa is shut for exports, and Karnataka is also shut, because of low production and Odisha is constrained because of the Shah Commission and so, the total mining activity.

The total mining activity currently is 140 MT and if you open up exports again the same thing will happen. The same corruption episodes will recur. At 100 MTof export, India will earn $10 billion. Instead, if we export 10 MT of steel. It will mean $8-9 billion. Which is equivalent to the iron ore exports at its peak.

Right now, there is no ban on iron ore exports. In Karnataka, what the Supreme Court has said is that they don't do over-exploitation of natural resources and they have capped iron ore mining within the state to 35 million tonnes.

Therefore, Karnataka will never be exporting. So, what this mining lobby is trying to push is the 30% disincentive as duty on export of iron ore which the government wants to cut.

Requirement of High Economic Growth for a country and the constraints

Inter-corporate rivalries and international corporate rivalries at play?

Sajjan Jindal, chairman and managing director of JSW Steel says exports will soar because of the depreciation of the rupee while opposing the reported move to lower duties on iron ore exports. In the course of an hourlong interview with ET's Satish John and Anirban Chaudhary, Jindal criticises tribal affairs minister KC Deo for supposedly seeking to keep tribal communities in a primitive state. Edited excerpts:

Is the manufacturing sector taking advantage of the weakened rupee?

The devalued rupee is a huge fillip. Last year, we exported 1.5 million tonnes of steel. This year, we may cross four million tonnes.

Everybody I was speaking to from my peer group, including Bharat Forge's Baba Kalyani, are all cranking up their manufacturing plants. We are 22% more competitive today because of the depreciating rupee. Steel is a global commodity.

India is not a player of significance in the global market. The total steel traded is 150 million tonnes a year. Japan does 60 million tonnes, South Korea does 30 million tonnes and India does 4 million tonnes. And this year we may do 10 million tonnes.

So, where are these exports happening?

For the first time in our history we are exporting to South Korea and Japan. After a gap of 10 years we are exporting again to China. We are also exporting to Europe and the US.

Doesn't China have an over-capacity?

Today, they are not exporting steel. They are consuming all their steel. Suddenly, the Chinese demand has picked up and their economy seems to have again revived. They consume 10 times more steel than what India consumes.

Do you agree that much of India Inc's problems are its own making?

Inter-corporate rivalry in the corporate sector brings its own pressure in Delhi. You instigate the NGOs and the media picks up. They hype it up. The judiciary picks up and does their bit. Then pressure builds up and investigative agencies get into the act. And, because the leadership is weak, every agency (overreaches).

We have so much of coal in our country (referring to the fallout of the Coalgate scam). We are now importing 200 million tonnes of coal. We are a poor nation and we cannot meet our energy requirement based on imports and we have so much coal deposits lying with us. It will last us for more than 100-200 years. And, coal will lose its relevance in 50 years and it will not be needed because new competing technologies such as nuclear, solar and wind will become more competitive.

Your industry has seen a lot of activity from NGOs. Is it inter-corporate rivalry?

The civil society is needed in every economy. They are a balancing act. They are not there in China. But, at times, they say no tree must be cut and that tribals must remain tribals. Please ask them whether the tribals want to remain a tribal. But the poor tribal does not know. He wants status quo. The case in point is the (Anil Agarwal's) Vedanta Resources in Niyamgiri. In my view, it is a real disaster for all of us.

So, who is behind such NGOs?

There are inter-corporate rivalries at play and there are international corporate rivalries.

International?