This is the story of how, in just two months, TFS went from a prospective good second bet in the taxi aggregator business in India, almost on the verge of raising $200 million, to a company that no venture capitalist would touch.

It all started when Ola Cabs (the company’s name is ANI Technologies Pvt. Ltd) turned up the heat—on 22 August 2014.

The company couldn’t have been more wrong. On 28 October, Ola raised $210 million (about Rs.1,281 crore) from SoftBank Internet and Media Inc. (SIMI) and its existing investors—Tiger Global, Matrix Partners India and Steadview Capital. “We never expected that someone would write a $210 million cheque for a cab aggregator company in India so soon,” says Raghu. “With that kind of money on the table, Ola would not stop. That’s when we thought we couldn’t just be on the sidelines and watch. That we would have to fight for our survival.” In the start-up world, whenever there is a large difference between two firms, raising capital becomes very difficult for the laggard. With $210 million at its disposal, Ola had serious potential to outrun TFS. So if TFS had to survive, it needed to grow. And then, because it had only so much cash in the bank ($8-10 million left, part of the $12 million TFS had raised in August 2014 from Accel US), it had to get into the market to raise another round, a big one.

Sometime in the third week of November, TFS started exploring the market to raise funds—around $200 million. Things looked good. In early 2014, skeptics had questioned the size and scale of the Indian taxi aggregation business, but with SoftBank’s $210 million investment in Ola, almost overnight, the market was validated. Everyone agreed that it was a multi-billion-dollar opportunity. Private equity and hedge funds in the US and Hong Kong were excited. “We were bleeding,” says Raghu, “but we took a call to get aggressive. We saw a 4X jump and our investors were so happy. It was amazing. So many investors were interested in participating. And everybody was telling me, this is amazing Raghu, this is great. We can put in a large sum of money.” Over the next couple of weeks, talks between TFS and prospective investors progressed smoothly. The company saw interest from more than 20 investors in the US. Due diligence and number crunching had already been done. Only two steps remained; a partnership meeting with the firm, where the entrepreneur makes a presentation to the firm’s senior team, and the final nod for investment.

Usually, entrepreneurs like to do this face to face. With that in mind, on 6 December (a Saturday), at about 8.30pm, Raghu boarded an Etihad Airways flight from Bengaluru to San Francisco. Only when he landed in the US, on Sunday morning, and connected to the airport Wi-Fi, did he realize that while he was on the flight, an incident with dire implications for the taxi business had taken place in India. Late in the evening, at about 11pm on 6 December, news broke that a Uber cab driver, Shiv Kumar Yadav, had raped a 26-year-old woman passenger in Delhi.

Uber - Bolt from the blue

Once Raghu reached his hotel, he got on to a call with Aprameya and the senior management team from TFS to discuss the Uber incident. In Delhi, things looked grim. There was widespread anger and the air was rife with rumours that all taxi aggregator firms would be banned. Other states, too, such as Karnataka and Maharashtra, were considering a ban. The news of the ban was circulating on social media, but TFS hadn’t received any notice.

Back in San Francisco, Raghu started feeling the pressure. He had lined up almost 20 meetings with VCs and hedge funds the following day, Monday, 8 December. He didn’t want to go in unprepared. So he asked for a breakfast meeting with Arun Mathew of Accel US and Ashish Gupta of Helion Ventures. They met, first thing Monday morning. “And they were like, it has become a big thing,” said Raghu. “Everybody in the Bay Area is discussing this, and just this. That’s when Arun told me it was a really bad time for me to visit because most talks would be on the Uber incident.” Mathew was right. Raghu’s first partner meeting was at 8.30am, and this is how he remembers it going.

First question: What do you think about the Uber incident?

Second question: What will happen to Uber? “I was like, this is the heat of the moment...,” Raghu replied. “Over a period of time, things will settle down. I think, in some part, Uber will have to make some changes in its business model, and stuff like that. But it doesn’t mean things will get eliminated, it is an essential service.” The partners weren’t convinced.

Third question: Have taxi aggregators been banned? Fourth question: What does the law say? Fifth question: Why have you not taken permits? “I told them we had not received any notice,” says Raghu. “It is not a banned service, as long as the regulations governing aggregators are absent. It is a new model, and the government hasn’t thought about this.”

The partners didn’t share Raghu’s optimism. In their mind, regulation was top priority, and they needed more time to figure it out before committing to investing. Over the next five days, every meeting, 23 in all, Raghu had followed a similar script. Even as all this was happening, back in India, Aprameya was facing the music of a government that was desperate to be seen as doing something. In a knee-jerk reaction, it wanted to ban the service.

On Tuesday morning (9 December), Aprameya got a call from the Bengaluru police commissioner to come for a meeting at 11am. Most cab operators were there, except Uber. “They made me stand up and asked me, what is your model? Do you take responsibility?” says Aprameya. But, before he could answer, someone behind him quipped: “Sir, on their website, they are saying they don’t take any responsibility.” As Aprameya tells it, the commissioner was furious, and it felt like being back in school, being reprimanded by the teacher. The same day, news appeared that the home ministry had banned Uber and all other taxi aggregators in Delhi. But there was nothing in writing. “Till date, we have nothing in writing saying we are banning you,” says Aprameya.

But public sentiment was against the aggregators, and they couldn’t make a statement about not actually being banned. TFS was helpless. It wanted clarity, but couldn’t get any as there was no formal paperwork. “The media said the home ministry has banned the service but we were working with the transport ministry. They were saying an internal memo has been sent. So there was no clarity.” Back in San Francisco, Raghu decided to wait it out another week. And seek fresh meetings with VCs who had Indians in their management, with the idea that perhaps they would understand the regulatory flux in India better than the Americans, for whom absolute clarity on regulation was top priority.

But, even in those meetings, nothing changed. “It was sheer bad timing,” says Raghu. “I wasn’t frustrated because I could understand their concern. But there was disappointment.” Raghu could have stayed longer, but the holiday season was about to begin. On 21 December, he got back to Bengaluru. He had no money but assurances from a couple of investors, who were keen to sync back after 7 January, when they would be back from holidays. Back in India, things hadn’t changed much. There was no regulatory clarity in Delhi or Chandigarh, where there was supposedly a ban. “The funny thing is we didn’t stop operations anywhere,” says Raghu. “Because we didn’t have any notice. It was only in the news.” In the second week of January, things became difficult. The firm was losing money every day and it just couldn’t stop the incentives. The investors who had promised hope after 7 January got back and said they were unsure. And the existing investors were not in a position to bring in money. “It needed a big guy to come in and write that cheque. It was a lot of money,” says Raghu.

The inevitable sale

On their part, Daniel and Prakash argued that on the face of it, Accel was interested in talking with Ola but that it was not their decision to make. “They have approached us and we think it is our responsibility to come and tell you guys. So you guys decide,” said Daniel. The meeting lasted about two hours, after which both Raghu and Aprameya went back to office. Once inside the boardroom, they frantically started putting together the names of the investors that they could reach out to at short notice. They were going to ask for some money to “weather the storm to survive”, says Raghu. They cut down on the amount of $200 million. On a piece of paper, Raghu put down 14 names. And over the next few days, he began calling each one of them. It was a futile effort. TFS had very little money left, and absolutely no time. The company had less than $2 million in the bank, which would have lasted only till mid-February. “We ourselves were not convinced (that we would survive),” says Raghu. “I called all the 14 people, and we even convinced two to participate; but it was too little, too late. We could have survived only for two-three months with that kind of money.” After a while, pragmatism won. The firm couldn’t afford a scenario where there would be no money to pay the salaries of the 1,800 employees. Or worse, pay operators. Between 15 and 20 January, the promoters realized selling out to competition was probably their best option. “That’s when we reached out to our investors to reach out to Uber and also began talks with Ola,” says Raghu. Even as all this was happening, on the morning of 28 January, The Times of India ran a story, citing people it didn’t name, that Ola Cabs would acquire TaxiForSure. For $200-250 million. The story said it is a “sealed deal and could be announced in the next few weeks”. Raghu claims the deal was far from being sealed as TFS had just begun talks. And not just to Ola but also Uber. For the outside world, it didn’t matter. At TFS’s office, all hell broke loose. “You know, 28 January was so miserable,” says Raghu. “I walk into office and see Monster.com and Naukri.com pages opened on some of the employees’ monitors. It is an open office, and you feel so bad. And you can’t walk up and say anything. And people are also not going to come up and ask.” Over the next few days, the cross talk among employees increased, so did the speculation. “For a few days after that, people would just leave at 6pm. We’ve never seen our office empty at 6,” he adds. Previously, on 20 January, the firm had “capped marketing expenses and put a freeze on hiring. So now, people started co-relating and jumping to conclusions”. It wasn’t long before the taxi operators started dropping by. Curious to know what’s happening because their livelihood depended on TFS’s existence. Aprameya and Raghu were helpless and frustrated. “We believed we are open and transparent,” says Raghu. “So now what? How do you hold that belief? Some people felt they are getting cheated because they are getting to know things from the newspapers. That phase was really bad—where we had no answers.” It is another matter altogether that concern over the future of the employees was playing on top of their minds in seeing the deal through. And to solve that piece of the puzzle, Raghu turned to Phanindra Sama, the founder of Redbus, for advice. Sama had made a successful exit in 2012, when he sold Redbus to Ibibo, but the exit hadn’t gone as well as Sama would have liked it to. In the first week of February, Raghu and Sama met at a Café Coffee Day outlet in Indiranagar, at 5pm. Raghu had a simple question for him: what are the mistakes he could avoid? Or what is it that Sama would do differently, if given a chance? It was then that Sama shared an interesting anecdote with him. Something that took place after Redbus was acquired by Ibibo. When an employee walked up to him and said: “Phani, just like you, we also gave our blood, sweat and tears for the firm. So why is it that you are the only one making money?” So Sama asked him, “What is it that you want?” And he said: “One month’s salary as bonus will do.” “That’s what Phani told me,” says Raghu. “That if at all, you should give one month’s bonus to all the employees. And I was like, okay, if that’s the case then why one month, we will give two months’ bonus.” That’s how equity stock option (ESOP) acceleration (for TFS stockholders) and two months’ bonus for about 1,800 people became the centre of the conversation and negotiation with Uber and Ola.

With Uber, the discussions went far, before a scary reality emerged. The company globally has 848 people on its rolls. TFS had 1,800 people in India. If the deal was to go through, it would lead to a massive bloodbath. “That’s where we closed it,” says Raghu. “So product, engineering, marketing, analytics, and tech, Uber has its own thing. And also Uber believed only in a driver-led model, so our operators (people who own and run a fleet of cabs) would also go. So it would have been a bloodbath and 90% of our people would have had to go. That’s why we said no.”

After that, it was just Ola. And Bhavish Aggarwal, the founder of Ola, agreed the company would continue to work with operators, and also ensure that none of the people in the team would lose their jobs.

Is Acquisition Of 'TaxiForSure' Good For 'Ola'

A columnist of Your Story quoted, “complete lack of hoopla around the acquisition… may seem intriguing.” Pointing at Ola Cabs’ acquisition of TaxiForSure is not very stable on its part and seems fragile. There are some companies in Indian history that are valued too much although it didn’t gross any profit.

What Next for TFS Promoters

One would think selling the company you co-founded for a neat $200 million (Rs 1,200 crore) would entitle you to a life of leisure. Not if you are Raghunandan G, who seems to be raring to get the adrenaline rush back by launching a start-up in the business-to-consumer (B2C) segment. This is less than a fortnight after his last day at TaxiForSure, the cab aggregator he and Aprameya Radhakrishna sold to bigger rival Ola.

The easier role of a mentor is not for him. Though he has made a few angel investments, the 33-year-old believes "getting your hands dirty is more fun than sitting and giving advice".

In a coffee shop in Koramangala, a favourite Bengaluru neighbourhood for start-ups, a relaxed Raghunandan, former chief executive of TaxiForSure, reveals he is considering several options, though yet to zero in on that one billion-dollar idea. "I can probably build and scale a business in the B2C segment, and I will probably restrict myself to something that I understand," he says. What he is sure of is that it should be bigger than TaxiForSure.

The idea, he says, could be around products or services and, ideally, should solve a problem many people face. Funding, he says, would not be a problem.

"We have access to capital, and all who had invested in us, as well as those we had spoken to but who could not be part of TaxiForSure, are willing to invest." He is also unfazed by the increasing competition in the consumer-facing space. "There are too many people, but who is executing it right," he asks. The conviction comes from experience - when TaxiForSure was launched in 2011, it was not the first or second taxi aggregator app. It was the eighth. Ola, incidentally, was the 10th.

Even as he considers various ideas, Raghunandan has a busy schedule: Meeting entrepreneurs and investors at coffee shops in different parts of the city, mentoring start-up teams, and advising Chinese, Japanese and American venture capital funds looking to enter India and eager to hear his views. He has invested in a few start-ups, too, but he declines to reveal the details. That should be the companies' prerogative, he says. And, he is spending more time with his wife and son, "who is finally realising he has a father (laughs)".

Radhakrishna, his friend of 15 years and co-founder, is on a world tour with his wife, in lieu of the honeymoon that he was not able to take when he got married a year ago.

Ola's acquisition of TaxiForSure in March was the first sign of consolidation in India's growing taxi aggregation business, part of the Rs 11,000-crore taxi market. Originally, Raghunandan and Radhakrishnan were to stay with TaxiForSure for three months after the acquisition in early March and "contribute in advisory roles". However, the transition was wrapped up in half the time, making April 16, 2015, their last day at the company. The two co-founders now own 0.8 per cent in Ola, worth over $19 million (around Rs 120 crore), according to a VCCircle report.

Are there mistakes he will not repeat with his next venture? "Oh, a whole lot," he says immediately. Top of the list is avoiding an excessive inward focus. "TaxiForSure started growing so fast… we did not look at anything outside," he recalls. "When you are driving a car, you need to also look at signals, not just the road." Linked to this is the founders' ability to assess the market accurately. While investors help, they end up saying several things, and it is difficult to always "pick up the signals from the noise", he adds.

He would also be much more careful about the terms of the agreements signed with investors while raising funds. When they set out to raise Rs 50 lakh for TaxiForSure, they wound up with funding of Rs 5 crore - no doubt a heady feeling. "But we got so carried away with the valuation and the money we raised that we did not look much at the term sheet," he recalls. What they did not realise was "the valuation keeps changing every quarter but the terms get carried forward". And with a new investor, they would be offered the same terms.

What Raghunandan will take with him to his next venture, whenever it is launched, is his core team, given his relationship with them and the trust they share. "When we were announcing the Ola deal to our (1850) employees, we had prepared a list of questions we expected they would ask, such as the future of their jobs. Instead, all they wanted to know was what his and Radhakrishna's next venture would be. "We had a brilliant team," Rahgunandan says, with a smile.

Story of another startup : Housing.Com Co-founder sends his resignation to Private Equity Investors

The term Unicorn refers to start-ups that are valued, on paper, at $1 billion or more by investors. The list of future unicorns, published by The New York Times based on data compiled by research firm CB Insights, has been put together taking into account multiple factors such as the capital raised, employee turnover and social media mentions.

Defences against Acquisition

Poison Pill

Integration Issues

Customer Perception Issues

Operational Issues

Cultural Integration Issues

Post Merger Integration

Inorganic growth strategy

Lupin buys out US generics firm Gavis in $880-mn transaction

An expert opinion when Acquisition was announced in Sep 2013. Later in 2015 it was sold off

Nokia Can't Save Microsoft — Only its Geniuses Can!

Vivek WadhwaFellow, Arthur & Toni Rembe Rock Center for Corporate Governance at Stanford University

I believe that the best path forward for Microsoft is to break itself up into a number of stripped-down and aggressive companies. These need to be free to compete with upstarts in Silicon Valley and with each other. These micro-Microsofts need to have the freedom to take risks and cannibalize the company’s core products.

Microsoft could take a massive write-off to the tune of $5.46 billion on its acquisition of Nokia assets as soon as July of this year, according to some industry watchers.

30th Jan 2014: Larry Page, Google's co-founder and chief executive, likes to talk about "big bets" and "moonshots." But the thing about moonshots is that they can crash to Earth.

That appears to be what happened to Motorola Mobility, the cellphone maker owned by Google. The Internet giant announced Wednesday that it would sell Motorola to Lenovo for $2.91 billion, less than two years after paying $12.5 billion to acquire it.

Motorola was Google's biggest acquisition by far and was hailed by the company as an example of the big bets Page was unafraid to make. Yet Motorola has continued to bleed money, aggravating shareholders and stock analysts, and its new flagship phone, the Moto X, did not sell as well as expected.

The deal is not a total financial loss for the extremely wealthy Google. In addition to keeping billions of dollars' worth of patents, Google essentially turned Lenovo into a factory for its Android operating system and also picked up some cash. Still, it is a sign of the fits and starts the company is experiencing as it navigates business in the mobile age, which has upended technology companies of all types.

In addition to using Motorola's patents to defend itself in the mobile patent wars, Google pledged to reinvent mobile hardware with Motorola's new phones and directly compete with Apple by owning both mobile hardware and software.

Yet while Google's business depends on phones getting into the hands of more people around the world, it benefits from selling the ads on those phones, not the phones themselves. Selling Motorola is an acknowledgment that Google is better off focusing on its core competencies - making software and selling ads - particularly as the profit margins for phones are shrinking overall.

"They make their money from people watching YouTube ads and doing searches," said Colin Gillis, an analyst at BGC Partners. "They don't necessarily need to be the hardware maker."

Still, Google will retain about 15,000 of the 17,000 patents it acquired as part of its original deal for Motorola and will grant Lenovo a license to use certain ones. Analysts have described the patents as the most valuable part of the acquisition, worth several billion dollars alone because they are firepower for Google to defend its Android mobile operating system.

Although the patents have not proved to be very helpful to Google in patent litigation, they have helped in cross-licensing agreements with other companies, including one Google and Samsung announced Monday.

Google's share price climbed 2 percent in after-hours trading after the announcement, a day before the company was set to announce its fourth-quarter earnings.

"Motorola's been a millstone and a drag on results," Gillis said. "You're slipping the millstone off your neck."

Lenovo, already the world's biggest PC company, is buying itself a toehold in the fast-growing smartphone business during a worldwide slowdown in PC sales and overnight brand recognition in the West.

In an interview, Wai Ming Wong, Lenovo's chief financial officer, said the deal would feed the company's "PC-plus" strategy.

"The Motorola handset business comes in very nicely to expand our business further," Wong said.

Motorola, which has a storied history as the maker of the first commercial cellphone, more recently fell behind rivals like Apple and Samsung. Page announced the deal to acquire Motorola just months after he reclaimed his position as chief executive of Google, and he appointed Dennis Woodside, who previously ran Google's sales and operations, as Motorola Mobility's chief executive.

Woodside said he would focus on just a few new phones instead of the old lineup of dozens. Yet the phones did not sell as well as expected, and Motorola continued to lose money despite drastic cost-cutting.

The decision to buy Motorola was "the extravagance of being a company with over $350 billion in market cap," said Jordan Rohan, an analyst at Stifel Nicolaus. "I'm not sure Motorola was fixable, and growth is much easier to come by on a company that's not a fixer-upper."

Still, Page said Google remained committed to hardware, a business that it has been entering over the past couple years, most notably with Motorola but also with products like Google Glass and companies like Nest Labs, the maker of smart thermostats and smoke alarms that Google acquired this month for $3.2 billion.

"This does not signal a larger shift for our other hardware efforts," Page wrote in a blog post. "The dynamics and maturity of the wearable and home markets, for example, are very different from that of the mobile industry."

"Lenovo has the expertise and track record to scale Motorola into a major player within the Android ecosystem," Page said.

It is unclear exactly how much money Google lost on the Motorola deal overall. In addition to the patents Google is keeping, Google sold Motorola Home, the portion of the business that made set-top boxes, to Arris in 2012 for $2.35 billion. Motorola also had $2.9 billion cash on hand when Google bought it.

Google is also retaining a small division working on cutting-edge technologies, led by Regina Dugan, who was hired from the government's Defense Advanced Research Projects Agency.

"On the heels of buying Nest and buying all these robotics companies, it makes you worry that they're destroying capital," Gillis said. "But that's what big bets are - some things you lose and this is a losing bet."

Lenovo appears to be building a comprehensive business in computers. Once known primarily as a maker of personal computers, last week Lenovo paid $2.3 billion for a big part of the computer server business of IBM.

Lenovo's shopping spree may be driven by the necessity of moving into other markets. Last year, the world PC market contracted by 10 percent, to 314.5 million units, according to the International Data Corp.

In the smartphone market, Apple and Samsung have taken share from almost all other suppliers. In its home country of China, Lenovo may be concerned about the rise of local smartphone manufacturers.

"It makes strategic sense for both Google and Lenovo," said Andrew Costello, a principal at IBB Consulting. "It will give Lenovo a strong brand in the mobile space outside of China that they don't have today, and it gives them deep operator relationships with AT&T and Verizon. And for Google, they're able to focus on the services side, which is what they're best at, and retain the patent holdings."

The deal marks a dramatic fall for Yahoo, one of the best known names of the early internet era, which had a valuation over $100 billion before the dot-com collapse in 2000 and which in 2008 spurned a $44 billion bid from Microsoft.

Acquire undervalued firms

Firms that are undervalued by financial markets can be targeted for acquisition by those who recognize this mispricing. The acquirer can then gain the difference between the value and the purchase price as surplus.

While the strategy of buying under valued firms has a great deal of intuitive appeal, it is daunting, especially when acquiring publicly traded firms in reasonably efficient markets, where the premiums paid on market prices can very quickly eliminate the valuation surplus. The odds are better in less efficient markets or when acquiring private businesses.

Diversify to reduce risk

Although diversification has benefits, it is an open question whether it can be accomplished more efficiently by investors diversifying across traded stocks, or by firms diversifying by acquiring other firms. If we compare the transactions costs associated with investor diversification with the costs and the premiums paid by firms doing the same, investors in most publicly traded firms can diversify far more cheaply than firms can.

Create Operating or Financial Synergy

The third reason to explain the significant premiums paid in most acquisitions is synergy. Synergy is the potential additional value from combining two firms. It is probably the most widely used and misused rationale for mergers and acquisitions.

Take over poorly managed firms and change management

Some firms are not managed optimally and others often believe they can run them better than the current managers. Acquiring poorly managed firms and removing incumbent management, or at least changing existing management policy or practices, should make these firms more valuable, allowing the acquirer to claim the increase in value. This value increase is often termed the value of control.

Cater to Managerial Self Interest (Not so Noble cause but it happens)

In most acquisitions, it is the managers of the acquiring firm who decide whether to carry out the acquisition and how much to pay for it, rather than the stockholders of the firm. Given these circumstances, the motive for some acquisitions may not be stockholder wealth maximization, but managerial self-interest, manifested in any of the following motives for acquisitions.

Snapdeal

calls off merger with Flipkart; to tweak biz model, lay off staff

Online

retailer Snapdeal has scrapped a proposed merger with bigger rival Flipkart

after months of negotiations and will now tweak its business model, cut costs

and slash headcount in a bid to revive its fortunes.

Snapdeal

had engaged with Flipkart on a merger for the past six months at the behest of

its biggest investor, Japan’s SoftBank Group Corp., after a few unsuccessful

attempts to raise capital. The Delhi-based e-commerce firm, which trails

Flipkart and Amazon, first explored a merger with

rivals about a year ago. It later carried out a rebranding exercise, slashed its workforceand

started serious talks with Flipkart for a sale.

Snapdeal,

which sold its digital payments unit FreeCharge for $60 million to Axis Bank

last week, plans to divest its logistics arm Vulcan Express soon. After raising

fresh capital by selling these subsidiaries, the company wants to chart out a

new journey that it calls Snapdeal 2.0.

A Snapdeal

spokesperson said in the statement that the company has made “significant

progress” towards executing its new strategy by achieving a gross profit this

month. “With the sale of certain non-core assets, Snapdeal is expected to be

financially self-sustainable,” the statement said.

Snapdeal 2.0

Two people with direct knowledge of the company’s plans said Snapdeal now wants

to position itself as a “true marketplace” without any inventory.

Snapdeal,

which originally began as a discount coupon seller 10 years ago, had gone

through several changes in its business model. It later transitioned into an

online deal site. By 2012, it had adopted a pure marketplace model without

managing its own inventory.

After raising around $1.65 billion

from SoftBank, Alibaba and other investors, Snapdeal pivoted to the

capital-intensive inventory-led model. But this has not quite worked out and

the company is now returning to the earlier model, which was championed by its

erstwhile investor eBay.

Redbus.com acquisition by IBibo

Tickets used to be booked through the traditional brick-and-mortar agents till 2005. That is when BITS Pilani alumni Phanindra Sama, Sudhakar Pasupunuri and Charan Padmaraju started Redbus, to sell bus tickets online.

The idea emanated from an experience that Phanindra had in the winter of 2005 in Bangalore, when he struggled to book bus tickets to make it home for Diwali and spend the vacations with his family. Diwali is one of the peak times in the year and every single bus agent in the city seemed to be booked and he could not make it to home in time. Phanindra realised the need for a convenient, hassle-free portal where customers could book their tickets from the comforts of their home. An additional benefit of RedBus was the fact that you could book your ticket for the return journey in advance without having to travel to the destination with the uncertainty of securing a ticket looming over your head. RedBus would provide the same convenience that customers enjoyed while booking tickets for trains or flights to the bus transport business. Phanindra took the idea to his college friends and colleagues and that was the beginning of RedBus.

Phani explains, "Your travel agent may say that the last bus for Cochin today is at 8pm, because that's the last bus of the operator he works with. That doesn't mean there isn't a bus for 10 or 11 pm from another operator. Also, the return ticket is something you'll get only from the place where you visit.RedBus solves these problems by allowing consumers to look at availability across all the operators and book in advance, even across state lines. "We even give a layout of the bus seating, and if you want a return ticket from the present destination, we update our inventory online at the final destination and you can get your ticket,"

Phani and his two co-founders undertook extensive market surveys to understand the market and the aspirations of the customers. Once they felt they understood the business, they developed a plan for the business and submitted it to a TiE (the Indus Entrepreneurs) mentorship competition - where they were among the three winners. The portal was created with the help of the initial seed funding and mentoring that was provided by the competition.

RedBus also sells two cloud based software, called BOSS and Seat Seller which it developed in-house, to bus operators (for managing their operations), and travel agents (to aggregate and sell tickets across multiple operators)

In June 2013, Phanindra Sama and Charan Padmaraju, the engineers from Andhra Pradesh who created the bus ticketing service redBus, sold their stake in the venture to the Ibibo Group, a subsidiary of South Africa's Naspers.

Other investors in the company - SeedFund, Kanwal Rekhi's Inventus, and Helion Ventures also exited for what is said to be an enterprise value of Rs 600-700 crore, making it the biggest overseas strategic acquisition of an Indian internet asset. Estimated value of the deal was said to be Rs 800 crore

Sri Chaitanya Educational Group obtains PE

New Silk Route, a leading private equity firm with USD 1.4 bn of AUM, has invested up to $ 25 mn in Hyderabad-based Sri Chaitanya Educational Group, which claims to be the country’s largest network of private schools and junior colleges.

It is learnt that the money will be infused into the comany in various tranches for a 35%-40% stake in the group, which seems to have been valued at somewhere between Rs 2800 to Rs 3500 crores.

Sri Chaitanya runs around 160 institutions, mostly in Andhra Pradesh, including 116 schools and junior colleges. Started with a small junior college in Vijayawada in 1986, the group has expanded into 7 states and has become the most trusted education brand in Andhra Pradesh.

K12 Techno Services (Gowtham Model Schools) attracts PE

K12 Techno Services Pvt Ltd, runs 70 Gowtham Model School units in Andhra Pradesh.

PE investment of Rs 75 crore made in July 2010, has been jointly put by Sequoia and SONG Investment Advisors in an 80:20 ratio. Second round funding of Rs 25 crore was made in March 2011.With this, Sequoia-SONG hold 49 percent in K12 Techno Services while the rest is with the promoters.

K12 Techno Services managing director M Venkatnarayana said the funds would be used to open 25 new schools, upgrade infrastructure and invest in teacher training this year. It is in talks to open 30-40 schools in Orissa, Chhattisgarh, Maharashtra and Karnataka next year. It has tied up with Brilliant Tutorials for partnership in IIT-JEE preparatory courses, with CfBT Education Trust (UK) for teacher training and the Indian School of Business for training school principals in business management.

Sequoia has invested in two other education ventures, TutorVista and Brainvisa, apart from K12 Techno Services.

According to its managing director GV Ravishankar Sequoia Capital India Advisors Pvt Ltd. the education sector is worth $40 billion, but it was a tough-to-execute market.

Tirumala milk Acquisition by Lactalis

Lactalis World’s largest dairy player agreed to buy Indian dairy producer Tirumala Milk Products Pvt. from private equity firm Carlyle Group and its promoters, in its first acquisition in the South Asian nation.

Lactalis will take over 100 percent of the Indian company and retain the existing management. Carlyle, the world’s second-biggest buyout firm, invested $22 million in the Indian company in 2010.

Shankar Narayanan, Managing Director, Carlyle India, said that Carlyle’s investment in Tirumala exemplifies its ability to partner with entrepreneurs to create value for all stakeholders. During Carlyle’s investment, he added that the company’s revenues grew two-and-a-half times and profits more than quadrupled.

We are extremely happy to have partnered with Carlyle, who provided numerous value creation activities and acted as a catalyst in the growth of the company over the past few years.

The deal will help Lactalis reduce its reliance on Europe, where it gets 60 percent of its revenue.

Foreign companies announced $15.6 billion of acquisitions in India last year, up from $11 billion in 2012, according to data Bloomberg compiled.

“India is an important place of opportunity for the development of the group worldwide,” Nalet said. “With the size of Tirumala today we think we have a good opportunity for the development of the Indian dairy market.”

India was the No. 3 producer of liquid, or non-powdered, cow’s milk in the world in 2013, behind the European Union and U.S., according to the U.S. Department of Agriculture.

Hyderabad-based Tirumala’s sales for the year ended March 2013 was 14.24 billion rupees ($229 million), according to its website. It had net income of 700 million rupees in the year. The company has seven plants across south India, and Lactalis will help expand the company in both north and South India, said Danda Brahmanandam, Tirumala’s founder and managing director.

Tirumala is the second-largest private sector dairy producer in southern India, Brahmanandam said.

Carlyle had invested around $1.1 billion in India as of Sept. 30, according to a December statement. Carlyle will invest in strong owner driven companies in sectors including consumer, health-care, technology and engineering services, said Carlyle India Managing Director Shankar Narayanan said in a phone interview from Mumbai today.

SKS Micro finance/Bharat Financial Acquisition by Indus Ind Bank

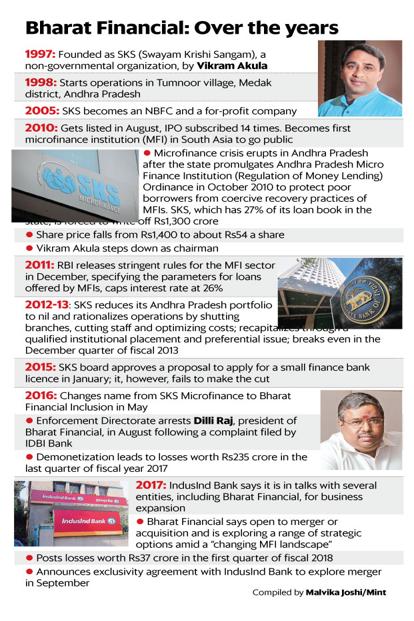

Sep 2017: The about 12-year-old journey of Bharat Financial Inclusion Ltd, formerly known as SKS Microfinance, has been tumultuous.

It suffered its biggest blow after the then undivided Andhra Pradesh promulgated a state law to severely restrict microfinance activity because of a spate of suicides by borrowers in late 2010, allegedly driven by coercive loan recovery practices. Subsequently, management differences saw the exit of its founder Vikram Akula and the central bank denied the microlender's claim to run a small finance bank (SFB).

Bharat Financial overcame the stress and has since improved its profitability. But it now faces a potential takeoverby the private sector lender IndusInd Bank, which some experts say is the only way for the survival of the microlender. The changing regulatory space has shrunk the microfinance industry to only three large companies, including Bharat Financial. Bharat Financial started its journey as a non-profit in 1998. Founded as Swayam Krishi Sangam by Vikram Akula, it later morphed into a non-banking financial company (NBFC) in 2005.

The microlender along with its peers saw unprecedented growth because of the reluctance of banks to serve the financial needs of poor customers who were not part of the formal banking system.

Five years later, it became the only microfinance lender to be listed on stock exchanges. In August 2010, Akula steered the initial public offering, which was subscribed almost 14 times. The success of SKS led to talks that other companies in the sector may also tap capital marketsThe party was, however, short-lived, not only for the company but also for the microfinance industry.

The suicides in Andhra Pradesh led to the state government putting severe restrictions on microlenders in a state that then accounted for a fourth of the industry's business.

Andhra Pradesh enacted a law greatly limiting the ability of microfinance companies to lend and recover their loans in the state. Operations of most MFIs came to a near halt. SKS was one of the worst hit due to the crisis.

In September 2010, just before the microfinance crisis unfolded, SKS's exposure to Andhra Pradesh was at over 27% of its total loan book, its highest in any state. In October that year, 30 poor women borrowers in Andhra Pradesh committed suicide within a period of 45 days. Among these 30 women, 17 were then reported to be borrowers of SKS Microfinance.In the years that followed, SKS Microfinance provided fully for the outstanding exposure in Andhra Pradesh, wrote off exposure of Rs1,360 crore in the state, and stopped fresh disbursals there.

"It (AP crisis) had a long-lasting adverse impact but BFIL (Bharat Financial) was an exception. We met all our commitments to lenders including to banks on time and never went into CDR (corporate debt restructuring) structure," said non-executive chairman P.H. Ravikumar.

Today, a chunk of SKS's assets are in Odisha, Bihar, West Bengal, Karnataka and Maharashtra.

While most believe that the industry has managed to survive the Andhra crisis, the recent loan waivers announced by the state governments of Maharashtra, Uttar Pradesh (UP) and Karnataka could trigger another round of defaults in repayments. "The market at large, particularly investment community, feels that for MFIs, Andhra Pradesh like event or UP or Maharashtra election like scenario which adversely affect their operations is going to be a periodic recurring feature. This increases the credit costs," Ravikumar said.

A year later in November 2011, Akula exited the company, allegedly owing to differences with the board.

This happened amid a changing regulatory framework.

As a fallout of the Andhra crisis, in December 2011, the Reserve Bank of India (RBI) put in place regulations based on the recommendation of a high-powered committee headed by Y.H. Malegam, a member of the central bank's board. The norms capped the margin between the cost of borrowing and the price at which loans were given, and interest rates and loans were regulated.

Despite this, the company maintained its growth momentum. Assets under management, consisting of non-Andhra exposure, grew at a compounded annual growth rate of 46% between fiscal 2013 and 2017. As of June-end, its non-Andhra Pradesh portfolio grew 14% year-on-year to over Rs9,630 crore.

Following the Andhra crisis, the company reported losses due to loan write-offs and a shrinking credit book. From the December 2011 quarter, when losses peaked to around Rs428 crore, the lender swung back to profit a year later. However, demonetization also impacted the collection of loans, which forced the lender to make higher provisions, resulting in losses.

With improving collection, its net loss narrowed to Rs37 crore in the June quarter from Rs235 crore a quarter ago.

Even as things look normal, Bharat Financial faced another hurdle with the central bank killing its banking aspiration. In September 2015, RBI handed out in-principle SFB licences to 10 applicants, eight of which were microfinance lenders. SKS Microfinance was left out.

According to Vikram Akula, the central bank's decision puzzled him because the lender seemed to meet all the criteria for an SFB. "Perhaps it was the RBIs discomfort with the current management team," he said on Monday.

Dilli Raj, the then president of the company, was under the scanner of the Enforcement Directorate in a complaint filed by IDBI Bank against First Leasing Company of India, where he worked previously.

The conversion of MFIs into SFBs and RBI regulations are also being seen as reasons for the fall of the MFI industry.

Regulations on loan spread and lending has been unfavourable for the micro lending industry. For instance, MFIs are not allowed to lend to a borrower who already has two loans but is not applicable to banks. SFBs have access to low-cost deposits, which gives them advantage of lower cost of funds. MFIs are not allowed to access deposits.

According to Bharat Financial's Ravikumar, the banks and SFBs today already have 70% share in the overall microfinance lending in the country and trends indicate that in another two or three years that share of MFIs would be less than 20-25% from 30% currently.

Monday's announcement by IndusInd Bank about the merger talks with Bharat Financial follows months of speculation. Several banks as well as non-banking financial companies were rumoured to be either picking-up a strategic stake or taking over the company.

According to analysts, most of the talks were based on the fact that a bank partnership would give the microlender a leverage to expand its horizon into other loan products such as gold credit, two-wheeler loan.

Akula, former head of Bharat Financial, said that it appears to him that the RBI has decided to focus on expanding financial inclusion through focusing on banks rather than through standalone MFIs.

"In light of the history of political backlash against standalone MFIs, I think this is a prudent tactical move. I just would like to see the RBI accelerate this process so that all standalone MFI-NBFCs move under the umbrella of a bank, either by becoming SFBs or merging with a bank," he said.

When asked if merger is natural choice for Bharat Financial given the challenging environment, Ravikumar did not offer any comments.

If the Bharat Financial-IndusInd Bank merger deal goes through, Grameen Koota Financial Services Pvt. Ltd, and Satin Creditcare Network, which are the other two large microlenders, will be the ones left in the space.

Jindal Haria, associate director, financial institutions, India Ratings and Research said, There are over 40 NBFC-MFIs in the country. It is a given that there will be further consolidation in the sector. "Given that private banks are looking for a way to reach the microfinance and missing middle customers and hence would gain from the distribution networks that MFIs have set up. It also could be an easy source of PSL. For MFIs, We are already seeing that the customer acquisition in urban areas is in single digits for most of them and in very few rural pockets it is over 20%." He further added, "They may have to evolve their loan products and may not be able to maintain high growth in group loan products without increasing borrower leverage. Hence there is clear synergy between banks and MFIs."

alekh.a@livemint.com

SEP 01, 2018,

Beverage giant

Coca-Cola’s global $5.1-billion buyout of Whitbread Plc owned UK café chain

Costa Coffee has set the world’s biggest soda maker in direct

competition with coffee giants such as Starbucks and Nestle, as it looks to

hedge its risks in a sluggish soft drinks market and broaden its portfolio

beyond sugary drinks.

“Costa gives Coca-Cola new capabilities and expertise in

coffee, and our system can create opportunities to grow the Costa brand

worldwide,” Coca-Cola president James Quincey said in a statement. “Hot

beverages is one of the few segments of the total beverage landscape where

Coca-Cola does not have a global brand. Costa gives us access to this market

with a strong coffee platform.”

Analysts said the deal will give Coca-Cola a scalable coffee

platform across parts of Europe, the Asia-Pacific, the Middle East and Africa,

with the opportunity for additional expansion, besides expertise in coffee

supply chain, sourcing, vending and distribution. CocaCola’s own coffee brand,

Georgia, remains small. Coca-Cola is urgently broadbasing its portfolio beyond

its core sugary drinks to retain consumers switching to healthier drinks. The

acquisition is to close in the first half of 2019 once all approvals are

received. Whitbread said Friday that it would focus on its hospitality

businesses under the Premier Inn franchise in the UK and Germany. It acquired

Costa Coffee for £19 million in 1995.

Success stories of Mergers and Acquisitions

2 stories to begin with

1. Nokia refused Android

2. Yahoo refused Google

Story Over

Lessons Learnt

1. Take risks

2. Embrace changes

3. If you refuse to change with time, you might perish

Ok 2 More stories

1. Facebook takes over whatsapp and instagram

2. Flipkart takes over Myntra and flipkart owned Myntra takes over jabong

Story Over

Lessons learnt

1. Become so powerful that your competitors become your allies

2. Reach the top position and then eliminate the competition

3. Keep innovating

2 More stories

1. Colonel sanders founded KFC at the age of 65

2. Jack Ma, who coudnt get job in KFC, founded Ali baba

Story over

Lessons learnt

1. Age is just a number

2. Only those who keep trying succeeds

Last but not the least

1. Lamborghini was founded as result of revenge of a tractor owner who was insulted by Enzy Ferrari, the founder of ferrari

Story Over

Lessons learnt

1. Never underestimate anyone, ever !!

2. Success is the best revenge

Just keep working hard !!

Invest your time wisely !!

Do what pleases you !!

Dont be afraid to fail !!!

Joint Ventures

Tata - Docomo

NTT Docomo and Tata Teleservices (TTSL) runs the Tata Docomo brand in India. After their joint venture, started posting continuous losses, TTSL was ordered to pay $1.17 (~Rs 7,538.89 crore) billion in damages to NTT by a London court in June last year. NTT paid Rs 12,924 crore in 2009 for an initial 26% stake in TTSL.

Tata Sons, the promoter of Tata Teleservices has received approval from the Competition Commission of India (CCI), to buy back 21.6% stake owned by Japan’s NTT Docomo.

SalesForce and

MuleSoft

$6.5 billion

acquisition that everyone hated a year ago was the only thing everyone loved

about Salesforce's latest quarter ROSALIE CHANMAR

6, 2019, 07.17 AM

Salesforce

acquired MuleSoft in 2018 for a whopping $6.5 billion, the

largest deal in the company's history. The big-ticket deal raised plenty

of skepticism at the time, especially since MuleSoft didn't fit neatly

into Salesforce's customer relationship management business. Salesforce's stock

sank about 5% in the immediate aftermath of the deal.

Mindtree acquisition by LT

Larsen and Toubro has bought the 20.32% stake at Rs 980 per share in Mindtree from early investor V G Siddhartha, after a lot of noise and the firing of a warning shot by promoters of the mid-tier IT services firm.

The Rs 3,269 crore deal was signed on Monday night and gives exit to investor VG Siddhartha

Engineering giant L&T is expected to spend as much as Rs 5,039 crore in an open offer to increase its stake to 51% and wrest majority control of the IT services firm, which would remain an independent listed entity. It is offering investors Rs 980 per share in the open offer, L&T and Mindtree disclosed separately on the BSE.

L&T has also advised its broker Axis Capital Ltd to buy as much as 15% shares from the open market to the tune of Rs 2,434 crore. With this, L&T is looking to increase its stake to 66.32% in Mindtree.

PVR

to acquire SPI Cinemas

PVR Ltd. will buy SPI

Cinemas, south India’s largest cinema chain and owner of the iconic Sathyam

Cinemas in Chennai in a transaction valued at 850

crore

The deal would help

PVR, which is listed on the stock exchanges, strengthen its base in Tamil Nadu,

a key movie market.

As per the terms of the

proposal, PVR would buy 71.7% stake in SPI Cinemas from existing shareholders

for a total consideration of 633 crore. Further, PVR would

issue 1.6 million shares or 3.3% shares in PVR as part of the transaction.

Based on PVR Ltd.’s closing share price of 1,317.20

on Friday, the 3.3% stake amounts to 210.75 crore. Overall, the cash and stock transaction is valued

at 843.75 crore. PVR currently operates a cinema circuit comprising

638 screens at 137 properties in 54 cities (19 States and UTs), serving 76

million patrons annually.

Post-transaction, PVR’s

total screen count will increase to 706 screens across 152 properties and 60

cities.

The acquisition will

also propel PVR as the seventh-largest cinema exhibitor in the world in terms

of annual admissions at its theatres, which will be in excess of 100 million,

according to a statement.

As on March 2018, SPI

had total assets of ₹319.63 crore and a

turnover of ₹309.60 crore. Ajay Bijli, chairman-cum-managing director, PVR

Ltd., said the transaction is a significant step in helping the firm achieve

its goal of 1,000 screens by 2020.

The statement added

there was also a provision for the customary call/put option for the firm to

buy the remaining 28.31% stake in SPI from SS Theatres LLP at an aggregate

price not exceeding 300 crore, if triggered

Business Today speaks

with Ajay Bijli, chairman and managing director of PVR, about how the multiplex

chain : March 13 2015

The Indian movie exhibition

industry was in the thick of action in 2014 with many acquisitions in the

multiplex business. All the big players - PVR, Carnival, INOX and Cinepolis -

are also betting big on small towns with malls. Ajay Bijli, chairman and

managing director of PVR, speaks with Arunima Mishra about how PVR Cinemas, the

largest chain of multiplexes in India with 462 screens, plans to maintain its

leadership position. Excerpts:

Q. How profitable has the Cinemax story been? Any takeaways? What's next

besides Sathyam?

Q. How is PVR looking at building its brand recall in the markets it's

entering? Also, does a movie-goer choose a cinema over another for the brand

value or it's the pricing and content?

Two people with direct knowledge of the company’s plans said Snapdeal now wants to position itself as a “true marketplace” without any inventory.

Redbus.com acquisition by IBibo

Tickets used to be booked through the traditional brick-and-mortar agents till 2005. That is when BITS Pilani alumni Phanindra Sama, Sudhakar Pasupunuri and Charan Padmaraju started Redbus, to sell bus tickets online.

Other investors in the company - SeedFund, Kanwal Rekhi's Inventus, and Helion Ventures also exited for what is said to be an enterprise value of Rs 600-700 crore, making it the biggest overseas strategic acquisition of an Indian internet asset. Estimated value of the deal was said to be Rs 800 crore

Carlyle had invested around $1.1 billion in India as of Sept. 30, according to a December statement. Carlyle will invest in strong owner driven companies in sectors including consumer, health-care, technology and engineering services, said Carlyle India Managing Director Shankar Narayanan said in a phone interview from Mumbai today.

SKS Micro finance/Bharat Financial Acquisition by Indus Ind Bank

SalesForce and MuleSoft

Q. How profitable has the Cinemax story been? Any takeaways? What's next besides Sathyam?

Q. How is PVR looking at building its brand recall in the markets it's entering? Also, does a movie-goer choose a cinema over another for the brand value or it's the pricing and content?

The PVR-INOX Merger

On March 27, 2022, PVR Limited ("PVR") announced that it proposes to merge with INOX Leisure Limited ("INOX"). Pursuant to the merger, the shareholders of INOX will receive shares of PVR at the approved share exchange (swap) ratio (the "PVR-INOX Transaction").

While existing screens of PVR and INOX are proposed to continue their present branding (i.e., 'PVR' or 'INOX', respectively), new cinemas opened following the merger will be branded as 'PVR-INOX'. The PVR-INOX Transaction is expected to bring together two of India's largest cinema brands with a combined network of more than 1,500 screens.1

Ordinarily, a deal of this magnitude would require the prior approval of the Competition Commission of India ("CCI"). In fact, PVR's acquisition of 39 screens from DT Cinemas (the "PVR-DT Transaction") in 2016 also required the approval of the CCI.

However, owing to the decreased revenues of the parties (and the cinema industry generally) caused by the pandemic, the PVR-INOX Transaction has been able to benefit from a revenue based statutory exemption to CCI approval requirements.

Market Positions of PVR and INOX

According to the press release issued by PVR, it currently operates 871 screens in 73 cities and INOX operates approximately 675 screens across 72 cities. The combined entity is headed to become the largest film exhibition company in India operating 1,546 screens across 109 cities.2

Based on publicly available information, the combined entity will have around 50 per cent multiplex screen market share and around 42 per cent box office collection market share.3

The creation of such an entity, particularly given that its market shares will cross 50% on a nation-wide basis, could potentially have effects on competition in the markets where the parties are present.

Review of Transactions by the CCI

The CCI was established under the Competition Act, 2002 ("Competition Act") to prevent practices that have an appreciable adverse effect on competition, to promote and sustain competition in markets, to protect the interests of consumers and to ensure freedom of trade carried on by other participants in markets in India.

Transactions involving enterprises which cross certain asset and turnover values (as prescribed under the Competition Act), are required to be notified to, and approved by the CCI prior to completion (unless any exemptions apply).

Pursuant to an exemption notified by the Ministry of Corporate Affairs, transactions are exempt from the approval requirements under the Competition Act where: (a) the value of assets being acquired, taken control of, merged or amalgamated is not more than INR 350 crore in India; or (b) the turnover of the target (i.e., the enterprise whose control, shares, voting rights or assets are being acquired) or the turnover attributable to the assets being acquired, taken control of, merged or amalgamated (as applicable), is not more than INR 1,000 crore in India (the "Target Based Exemption").4 Recently, the applicability of the Target Based Exemption was extended to March 2027.5

Based on the financial statements for the year ended 2020-21, the revenue for PVR was INR 280 crore6, and INOX was INR 106 crore7. These revenue numbers are below the thresholds provided in the Target Based Exemption, and allow the PVR-INOX Transaction to be exempt from notification and approval requirements under the Competition Act.

As stated above, in 2016, the CCI reviewed the PVR-DT Transaction and found that it was likely to have an appreciable adverse effect on competition in India due to a large increase in market shares in certain locations such as Noida, Gurgaon, and South Delhi. Therefore, the CCI directed divestiture of 7 screens belonging to DT, along with other commitments to be undertaken by PVR, prior to the completion of PVR-DT Transaction.8

Given that the Competition Act does not grant the CCI powers to examine transactions that are exempt from approval requirements, the PVR-INOX Transaction is unlikely to be reviewed by the CCI.

However, the subsequent conduct of the combined entity could be examined under the provisions relating to (i) the abuse of dominance under Section 4 of the Competition Act (for example, by way of imposing unfair prices or conditions) or (ii) anti-competitive agreements under Section 3(4) of the Competition Act (including, for example, with respect to tie-in arrangements, exclusive agreements, etc.)

Accordingly, it appears that due to revenue losses owing to the pandemic, the PVR-INOX Transaction will escape the CCI's scrutiny, and could result in an asset heavy company that would otherwise have been subject to the CCI's view on whether divestitures are needed based on competition concerns.

Adani Ports Strengthens presence on the Eastern Coast

Gautam Adani-led Adani Ports and Special Economic Zone Ltd (APSEZ) will buy a 75 per cent stake in Krishnapatnam Port Company Ltd, the entity that runs a private deep-water port at Krishnapatnam in Andhra Pradesh's Nellore district, for ₹13,500 crore.

Business Line was the first to report on the deal in its edition dated August 19, 2019.

The deal is APSEZ's biggest acquisition yet in India's port sector in terms of value and size and helps it build scale in an industry that is dominated by the 12 state-owned ports.

The acquisition, finalised today, fits well with the Group's strategy to take-over stressed assets, said a person briefed on the deal.

The acquisition will give APSEZ, India's biggest private port operator, access to the country's largest waterfront area (for a port) of 12.5 kms and a transit storage area of 6,800 acres. The port started operations in 2008.

Krishnapatnam, a port owned by the Andhra Pradesh government, was given to the Hyderabad-based CVR Group for development and operations on a 30-year contract beginning September 2004. The port contract can be extended up to 50 years (30+20 years).

Chinta Sasidhar, the managing director of Krishnapatnam Port Co Ltd and the youngest son of C Visweswara Rao, its chairman, will continue to hold the balance 25 per cent stake in the port operating company.

Currently, the port has a draft of 18.5 metres, a depth that can accommodate full-loaded Capesize vessels of 200,000-tonne capacity.

The port, located 180 kilo metres north of Chennai, currently has a capacity to handle 92 million tonnes (mt) of cargo from 10 berths, including 67 mt of bulk cargo and 2 million twenty-foot equivalent units (TEUs) of containers which is equivalent to 25 mt.

The port handled 54.37 mt in FY 19 including 506,168 TEUs.

The port has applied for environment and coastal regulation zone (CRZ) clearances to expand capacity further.

Krishnapatnam Port Company is 90.6 per cent owned by the CVR Group, which has interests in construction, ports, power, steel, information technology and exports.

London-based private equity firm 3i Group Plc invested $161 million in the port operating company in February 2009 through its India Infrastructure Fund for a 26% stake. 3i's stake has since dropped to 9.4 per cent due to change in valuations and rupee depreciation.

The deal will give 3i an exit route for its investment over which it has been wrangling with the CVR Group for some time.

This will be APSEZ's third acquisition on the eastern coast after the purchase of Dhamra port in 2014 and Kattupalli port in 2016.

The deal will also help APSEZ expedite the vision of handling 400 million tonnes (mt) of cargo by 2025 and expand its market share among India's ports.

The proceeds will be used by the CVR Group to settle lenders' dues, a person briefed on the deal said.

In FY19, APSEZ loaded a combined 207.7 mt of cargo, clocking a growth of 15 per cent over FY18. The standalone port business earned ₹8,897 crore in FY19 and a net profit of ₹4,006 crore.

APSEZ's 10 strategically located ports and terminals — Mundra, Dahej, Kandla and Hazira in Gujarat, Dhamra in Odisha, Mormugao in Goa, Visakhapatnam in Andhra Pradesh, Kattupalli and Ennore in Tamil Nadu — have the capacity to handle a combined 395 mt of cargo, accounting for 24 per cent of the country's total port capacity.

APSEZ is also developing a container transhipment port at Vizhinjam in Kerala and a container terminal at Yangon in Myanmar.

Krishnapatnam is Adani's second acquisition in the port logistics space in less than a week after the purchase of Snowman Logistics Ltd for ₹296 crore on December 27

WhiteHat Jr acquired by Byju

Think and Learn which owns and operates education technology platform Byju’s — The Learning App — has acquired Mumbai-based WhiteHat Jr in a $300 million all-cash transaction, according to an announcement late Wednesday evening.

WhiteHat Jr, founded in 2018 by Karan Bajaj, the former CEO of Discovery Networks India, operates in the K-12 segment, teaching students to code and helping them build commercial-ready games, animations and apps, using the fundamentals of coding.

The startup has developed a proprietary coding curriculum, focused on product creation, and imparts lessons through live, interactive online classes. It claims to be clocking a revenue run rate of $150 million. DC Advisors acted as the exclusive financial advisors to the transaction.

According to an official statement released by Byju’s, it will make significant investments in WhiteHat Jr’s technology platform, product innovation while expanding the teacher base to cater to demand from new markets. Bajaj will continue to lead and scale this business in India and the US.

WhiteHat Jr is the leader in the live online coding space. Karan has proven his mettle as an exceptional founder and the credit goes to him and his team for creating coding programs that are loved by kids. Under his leadership the company has achieved phenomenal growth in India and the US in a short span of time," said Byju Raveendran, founder and chief executive of Byju's.

The closure of the deal comes even as Byju's is reportedly in advanced stages of negotiations to acquire Doubtnut, a two-year-old learning app, for as much as $100-$150 million, in what is also expected to be an all-cash transaction.

The purchase of WhiteHat Jr is also the largest acquisition, till date, by Byju's . It had previously acquired Osmo, a US-based learning platform, for which it paid $120 million, in January 2019. At the time, the deal was said to be part of the Bengaluru-based firm's plan to aggressively expand internationally. Before that, Byju's had acquired Math Adventures, TutorVista and Vidyarth.

The Bengaluru-based unicorn, which is valued between $10-$10.5 billion, has also been on a fundraising spree over the course of the current calendar year. Earlier this week, Bloomberg reported that DST Global, the investment firm led by Israeli-Russian billionaire Yuri Milner, was in advanced stages of investing an estimated $400 million into the company.

CORPORATE FINANCE MINI COURSE

https://youtu.be/5eGRi66iUfU

https://courses.corporatefinanceinstitute.com/courses/introduction-to-corporate-finance

TR Foods owner Orkla to acquire Eastern Condiments

In a major development in

the food and beverages industry, Norwegian consumer conglomerate Orkla ASA that

also owns MTR Foods is set to acquire one of South India’s leading spice

makers, Eastern Condiments. Orkla will pick up 68 percent stake of Eastern Condiments,

and initiate a merger with MTR Foods.

In a major development in

the food and beverages industry, Norwegian consumer conglomerate Orkla ASA that

also owns MTR Foods is set to acquire one of South India’s leading spice

makers, Eastern Condiments. Orkla will pick up 68 percent stake of Eastern Condiments,

and initiate a merger with MTR Foods.

The transaction will see MTR acquire 41.8 percent stake from the Meeran Family,

who are the promoters of Eastern. The balance of 26 percent will be picked up

from McCormick Spices which holds the stake. After the first leg of acquisition, an application to merge

Eastern with MTR will be submitted and the merged company will be owned by

Orkla ASA and the two brothers — Firoz and Navas Meeran, with a split stake of

90.1 and 9.99 percent respectively.

Eastern Condiments was founded by Kothamangalam native

late ME Meeran in Adimali in 1983. The brand’s name can be traced back to the

Eastern Trading Company which Meeran founded in 1968. The company has grown

into one of India’s largest spice exporters.Apart

from spices, Eastern also sells Sambar podi, Adai Dosai mix, Upma mix, pickles

and other ready-to-eat food items. They have also diversified to other

unrelated fields like mattress manufacturing. They even dabbled in Education

and Wind Energy.The company also acquired

actor Mohanlal’s company — Mohanlal’s Taste Buds — in 2007. Three years later,

McCormick Spices acquired 26 percent stake in Eastern for Rs 162 crore from a

PE Fund and the Meeran Family. The same year, MTR had lost out in the race to

McCormick. According to a spokesperson from Avendus Capital, financial

advisors to Eastern and McCormick on the transaction, Eastern and MTR combined

have “significant synergy potential in terms of product portfolio and

geography.” The deal, according to the representative, “is a testament to the

strong interest in branded spices from large F and B players”. Orkla

ASA which is headquartered in Oslo is a major supplier of branded consumer

goods in the Nordics, Baltics and a few markets in Central Europe and India

M&M and SsangYong

In April 2010, the company

released a statement citing interest of three to four local and foreign

companies in acquiring SsangYong Motor Company.The companies were later

revealed to be Mahindra & Mahindra, Ruia Group, SM Aluminum, Seoul Investments and

French-owned Renault Samsung Motors of

South Korea.In August 2010, Mahindra & Mahindra Limited was chosen

as the preferred bidder for SsangYong

M&M intended to become

global SUV player with this acquisition. However a decade later M&M has

written off SsangYong Investment, in the results declared for the quarter ended

March 2020. In September 2020 it had informed that over 98% shareholders had

approved the company’s decision to transfer, dilution or cessation of

controlling stake in its Korean subsidiary after it failed to turn it around

even nearly a decade after acquisition. On 21Dec 2020 SsangYong

filed for Bankruptcy.

Vertical Integration :Nextbillion to buyout Indiabulls

Mutual Fund for 175 crore

In May 2021, Nextbillion Technology Private had

entered into a deal with the fund house to buy out the entire stake for 175

crore.

The proposed transaction will mark the entry of

Nextbillion Technology (Groww) in asset management space of managing mutual

fund schemes. Prior to this transaction, the acquirer did not own and manage

any asset management business.

Existing Domain: Registered distributor

Nextbillion Technology is a stockbroker and

depository participant. It is also registered with Association of Mutual Funds

in India as a mutual funds distributor. It is engaged in providing an online

platform named Groww that allows investors to invest in mutual funds and

stocks.Indiabulls AMC is a subsidiary of Indiabulls Housing Finance.

Reliance-Disney Deal may face antitrust review

A merger between Walt Disney's

India division and Mukesh Ambani's media enterprise could form a strong

entertainment giant in India. However, legal experts suggest the merger might

face intense antitrust scrutiny. The merger could require shedding assets.

Disney and Reliance, both with significant streaming services and a total of

120 TV channels, are reportedly considering a merger where Ambani's group would

probably hold the majority stake.

A merger of Walt Disney's

India unit and billionaire Mukesh Ambani's media business would create an

entertainment powerhouse in India, but lawyers say any deal would draw intense

antitrust scrutiny and assets would likely need to be shed.

Disney and India's Reliance, which each have a

major streaming service as well as 120 TV channels between them, are looking at

merging into an entity in which Ambani's group would likely have a majority

stake, sources said this week.

If a deal was struck, it would be the second to

seismically reshape India's TV and streaming landscape as Japan's Sony also

plans to merge its India business with India's Zee Entertainment.

One key area of regulatory scrutiny for a

Disney-Reliance merger would be their streaming businesses and their power over

advertising during cricket - a sport that commands fanatical devotion in India.

Disney Hotstar, India's biggest streaming app

with 38 million users, owns the rights for International Cricket Council's

matches in India until 2027, while Reliance's growing JioCinema app has the

rights for popular cricket league IPL.

The CCI would be worried that the "combined

entity, due to its strong market presence in streaming can command their own

rates and advertisers will be left without bargaining power," said Vaibhav

Choukse, head of competition law at Indian law firm JSA.

While divesting certain channels would be an

option to assuage CCI's concerns, the merged entity could also offer commitments to not raise ad rates for a certain period, according to Gautam

Shahi of Dua Associates.

The Zee-Sony plan cleared a

review by the Competition Commission of India (CCI) last year and could close

in the coming weeks. The two companies have said they will divest three of

Zee's Hindi TV channels as part of their agreement for regulatory acceptance.

This deal may get closer scrutiny because of the

increased concentration of market power post the Zee-Sony merger. That makes

their path to CCI approval more challenging," said Avimukt Dar, founding

partner at India's IndusLaw.

Disney declined to comment. Reliance, its

broadcast unit Viacom18 and the CCI did not respond to Reuters queries.

"If the market shares

of the parties exceed 40-50% in any market, CCI is likely to conduct a detailed

investigation," said Choukse.

Reuters Dec 16, 2023

Think and Learn which owns and operates education technology platform Byju’s — The Learning App — has acquired Mumbai-based WhiteHat Jr in a $300 million all-cash transaction, according to an announcement late Wednesday evening.

WhiteHat Jr, founded in 2018 by Karan Bajaj, the former CEO of Discovery Networks India, operates in the K-12 segment, teaching students to code and helping them build commercial-ready games, animations and apps, using the fundamentals of coding.

According to an official statement released by Byju’s, it will make significant investments in WhiteHat Jr’s technology platform, product innovation while expanding the teacher base to cater to demand from new markets. Bajaj will continue to lead and scale this business in India and the US.

The purchase of WhiteHat Jr is also the largest acquisition, till date, by Byju's . It had previously acquired Osmo, a US-based learning platform, for which it paid $120 million, in January 2019. At the time, the deal was said to be part of the Bengaluru-based firm's plan to aggressively expand internationally. Before that, Byju's had acquired Math Adventures, TutorVista and Vidyarth.

The Bengaluru-based unicorn, which is valued between $10-$10.5 billion, has also been on a fundraising spree over the course of the current calendar year. Earlier this week, Bloomberg reported that DST Global, the investment firm led by Israeli-Russian billionaire Yuri Milner, was in advanced stages of investing an estimated $400 million into the company.

https://courses.corporatefinanceinstitute.com/courses/introduction-to-corporate-finance

M&M and SsangYong

In April 2010, the company

released a statement citing interest of three to four local and foreign

companies in acquiring SsangYong Motor Company.The companies were later

revealed to be Mahindra & Mahindra, Ruia Group, SM Aluminum, Seoul Investments and

French-owned Renault Samsung Motors of

South Korea.In August 2010, Mahindra & Mahindra Limited was chosen

as the preferred bidder for SsangYong

M&M intended to become global SUV player with this acquisition. However a decade later M&M has written off SsangYong Investment, in the results declared for the quarter ended March 2020. In September 2020 it had informed that over 98% shareholders had approved the company’s decision to transfer, dilution or cessation of controlling stake in its Korean subsidiary after it failed to turn it around even nearly a decade after acquisition. On 21Dec 2020 SsangYong filed for Bankruptcy.

Vertical Integration :Nextbillion to buyout Indiabulls Mutual Fund for 175 crore

The proposed transaction will mark the entry of

Nextbillion Technology (Groww) in asset management space of managing mutual

fund schemes. Prior to this transaction, the acquirer did not own and manage

any asset management business.

Existing Domain: Registered distributor

Reliance-Disney Deal may face antitrust review

A merger between Walt Disney's

India division and Mukesh Ambani's media enterprise could form a strong

entertainment giant in India. However, legal experts suggest the merger might

face intense antitrust scrutiny. The merger could require shedding assets.

Disney and Reliance, both with significant streaming services and a total of

120 TV channels, are reportedly considering a merger where Ambani's group would

probably hold the majority stake.

A merger of Walt Disney's India unit and billionaire Mukesh Ambani's media business would create an entertainment powerhouse in India, but lawyers say any deal would draw intense antitrust scrutiny and assets would likely need to be shed.

Disney and India's Reliance, which each have a

major streaming service as well as 120 TV channels between them, are looking at

merging into an entity in which Ambani's group would likely have a majority

stake, sources said this week.

If a deal was struck, it would be the second to seismically reshape India's TV and streaming landscape as Japan's Sony also plans to merge its India business with India's Zee Entertainment.

One key area of regulatory scrutiny for a

Disney-Reliance merger would be their streaming businesses and their power over

advertising during cricket - a sport that commands fanatical devotion in India.

Disney Hotstar, India's biggest streaming app

with 38 million users, owns the rights for International Cricket Council's