Preparation of Financial Statements as per Reporting Standards

Schedule III to the Companies Act, 2013 was amended on March 24, 2021, to improve the quality and reliability of financial statements. Some new disclosures were also added to Schedule III. The amendments to Schedule III are applicable from 1st April 2021.On analyzing the amendments in Schedule III and CARO 2020, it can be stated that the majority of the modifications made in Schedule III and CARO 2020 are to match the two reporting frameworks and improve transparency between the company and the users of financial statements. It further enabled to reduce the risk of fraud and other unethical behavior on part of the companies.

Highlights of the amendments in Schedule III

1.Shareholding of Promoters: As compared to earlier version, the entities shall now disclose the shares held by the promoters at the end of the financial year and % change during the year in notes to accounts in tabular format as mentioned in the Schedule.

2.Rounding Off: It is mandatory for the companies to round off the figures appearing in the financial statements on the basis of ‘Total Income’. Earlier this provision was optional and round off was done on the basis of ‘Turnover’.

3.Short Term Borrowings: From 1 April 2021 onwards, the current maturities from long term borrowings is required to be separately disclosed in the financial statements.

4.Trade Payables Due For Payments: Gone are those days where ageing schedule for only receivables were made. From now onwards, it shall be prepared for trade payables also which are due for payment, in a tabular form, whether or not, due date of payment is specified on bill. However, unbilled dues shall be separately disclosed.

5.Disclosure for Tangible and Intangible Asset: At the beginning and end of the reporting period, a reconciliation of the gross and net carrying amounts of each class of assets showing additions, disposals, acquisitions through business combinations, amount of change due to revaluation and other adjustments and the related depreciation and impairment losses or reversals shall be disclosed separately, if the changes is 10% or more in each class of asset.

6.Trade Receivables outstanding: Ageing schedule shall be prepared for trade receivables in a tabular form in a manner as notified by MCA, whether or not, due date of payment is specified on bill. However, unbilled dues shall be separately disclosed.

7.Borrowing from Banks and Financial Institutions: At balance sheet date, the companies shall disclose the details of those funds which were borrowed from banks and financial institutions for a specific purpose.

8.Title deeds of Immovable Property: The companies have to give the details of all those immovable properties whose title deeds are not in the name of the company, except those immovable properties in which the company is lessee and lease agreement are executed.

9.Loan Granted to Promoters, Directors, KMPs and the Related Parties: The company shall disclose all the loans and advances in the nature of loan granted to promoter director and KMPs and related parties, severally or jointly with any other person either repayable on demand, without specifying any terms or period of repayment.

10.Benami Property: Company shall disclose all the benami property in which proceedings have been initiated or pending against the company for holding any benami property under the Benami Transactions (Prohibition) Act, 1988 and rule made thereunder, disclosures shall be made in the manner prescribed.

11.Willful Defaulter: If any company is declared as wilful defaulter by the bank or financial institution or any other lender then disclosures shall be made by the company in the manner prescribed.

12.Ratios: Companies shall disclose the all those ratios which are prescribed and shall explain the items included in numerator and denominator for computing the above ratios. Moreover, if any change in the ratio is more than 25% as compared to the preceding year then explanation for the same shall be provided.

13.Undisclosed income: Where a company has surrendered or disclosed any income under the relevant provisions of the Income Tax Act and which are not disclosed earlier shall be disclosed in the books of accounts, unless there is immune impact.

14.Corporate Social Responsibility: Where a company under section 135 of the Companies Act, 2013, then disclosure shall be made in the manner prescribed in the Schedule III to the Companies Act, 2013.

·Crypto Currency or Virtual Currency: If any company has traded or invested in Crypto Currency or Virtual Currency then disclosures shall be made in the financial statements relating to Profit and loss made from crypto currencies, Amount of currency held at reporting date, Deposit or advance taken from any person for trading or investment in crypto.

IND AS

IND-AS 115 Revenue Recogntion

FINANCIAL INSTRUMENTS - INDAS 32,109 and 107

Computation of Lease Asset, Liability and Expenses IND AS 116

IND- AS 110 Consolidation

Joint Arrangements

IndAS 111 that is IFRS 11 charts

Ind-AS 112 Disclosures

Segmental Reporting under Ind-AS 108

Interaction between various standards on consolidation

IND-AS 113 Fair Value

Inter Corporate Investments- Business Combinations

Accounting treatment of Goodwill

Goodwill and intangibles acquired in merger-and-acquisition transactions represent synergies and benefits accruing to the acquiring enterprise.

Under old AS, the transaction structure determines the accounting; an asset acquisition is covered by AS-10, a court merger by AS-14, but everything else is practically left out.However, most acquisitions today are through acquisition of a company, which is only covered by AS-21 through its guidance on consolidation procedures of historical values.Intangibles that are self-created are often not recorded in the books of the selling company. and hence the value attributed to these elements is accounted as goodwill.

On subsequent measurement of goodwill : for transactions accounted as per AS-10, the standards state it is prudent to amortise, but not required. On the other hand, for goodwill arising on consolidation as per AS-21, there is no specific guidance, hence only tested for impairment if indicators exist. Further, goodwill arising out of a merger as per AS-14 is required to be amortised over five years. So, depending on the transaction structure used to acquire the business, the subsequent accounting is determined and impacts the recognised values on the balance sheet as well as the reported income in subsequent periods. The fact that the amount recorded as goodwill might actually represent some finite life assets is often not considered.

Business combination as per new Ind-AS

According to IFRS and Ind-AS, a business combination is a transaction where an acquirer obtains control over one or more businesses, and such transactions may be structured as mergers, outright acquisitions or the creation of a new entity. The meaning of the term is, thus, quite wide and designed to cover typical types of M&A activity.

Accounting for business combinations follows the acquisition method, where a key element is the recognition and measurement of all identifiable assets acquired and liabilities assumed. Thus, intangibles that were not previously recognised — such as customer contracts, relationships, favourable lease arrangements and so on — are also separately identified and valued. Goodwill is the residual amount after allocation of the purchase consideration to the assets and liabilities taken over, including intangibles. The goodwill itself is not amortised but only tested for impairment on an annual basis.

Accounting using this guidance, therefore, helps enterprises communicate to key stakeholders in a much more transparent and measurable manner the business rationale and expected value addition. Ashish Gupta is Partner and Saurabh Mathur is Manager, Walker Chandiok & Co

Goodwill Impairment

Income Taxes - Ind-AS 12

Account for Tax Expense in traditional method vs AS/IND-AS

Method

Tax Expense in P&L

Old Practice before AS came into effect

Tax Payable method

Current Tax

New Practice after AS/IND-AS is applied

Tax effect accounting method

Current Tax

+/- Deferred Tax

+/- DeferredTax adjustment

of opening balance

What is sought to be acheived is Effective Tax Rate over a period of Time

Effective Tax Rate is not tax rate multiplied by book profit. It is a tax rate after taking away the permanent differences and then multiply with book profit.

What appears in P&L is - book profit multiplied by Effective Tax Rate over a period of Time (plus adjustment for opening balance of Deferred Tax Asset / Liability created out of previous understanding of timing differences which got changed now.)

This is one of the few standards which serve two purposes. - serve shareholder interest by not distributing away PAT based on current tax incidence if the entity is currently enjoying some benefits - Serves analysts by providing valuable insight into the effective tax rate for that entity which was earlier disclosed only in prospectus.

Employee Benefits

IndAS 19 Employee benefits

IND AS 19 vs IFRS 19

IND-AS Property Plant and Equipment

PPE

OTHER COMPREHENSIVE INCOME

IND AS CARVE OUTS

IFRS Covergence in New companies Act 2013

Companies Bill contains numerous provisions aligned to International Financial Reporting Standards. Under the Bill, utilisation of securities premium will be restricted to a prescribed class of companies whose financial statement complies with specified accounting standards. In meeting IFRS requirements, such companies cannot utilise the securities premium to write off preliminary expenses of the company, write off preference share or debenture issue expenses, and provide for premium payable on redemption of preference shares/ debentures. However, if the prescribed class of companies is notified immediately, the impact will be felt straightaway in Indian GAAP financial statements. As this is not the intention, the Ministry of Corporate Affairs should notify the prescribed class at a date aligned to IFRS implementation; otherwise there may be unintended consequences.

For changes in accounting policies and correction of past errors, IFRS requires restatement of comparative numbers. Currently, according to the Ministry's circular, a company can reopen and revise its accounts after they have been adopted during the annual general meeting and filed with the registrar to comply with any other law for a true and fair view. Thus, the current Companies Act is not suitable for IFRS implementation. Under the Bill, voluntary revision of financial statements is permitted and, hence, aligned to IFRS implementation. However, the revision process is cumbersome, including prior approval from the Income Tax Appellate Tribunal. In other words, under IFRS, every company should take adequate precaution in the selection of accounting policies and ensuring that errors are rare occurrences.

Currently, the Securities and Exchange Board of India requires all listed companies seeking approval for a draft merger, amalgamation or restructuring scheme to file an auditors' certificate to show that the accounting complies with standards. There is no such requirement for unlisted companies, including their subsidiaries. Under Companies Bill, the Tribunal will not sanction capital reduction, merger, acquisition or other arrangements unless the accounting treatment complies with standards and an auditor's certificate is filed. This is aligned with IFRS.

Schedule II of the Companies Bill sets out the useful lives of assets. Companies other than the prescribed class (essentially IFRS companies) should mandatorily adhere to these useful lives as minimum rates. The prescribed class of companies are allowed to depart from Schedule II useful lives to comply with IFRS. It is not clear whether these companies will be notified immediately or after IFRS is in force. If notified later, then all companies have to comply with Schedule II useful lives as minimum rates as soon as the bill becomes law. As the useful lives in many cases have been drastically reduced, the overall impact of depreciation on the profit-and-loss account can be negative.

Companies Bill requires component accounting, where components are depreciated based on their useful lives rather than the life of the principal asset. This is aligned to IFRS. However, until Indian GAAP applies (and the prescribed companies are not notified), companies should mandatorily follow useful lives under Schedule II. It is unclear how component accounting can be applied here, as that inherently involves departure from useful lives prescribed for the principal asset.

Under the Bill, for revaluation, depreciation will be based on the re-valued amount rather than historical cost. This is aligned to IFRS and will have a negative impact due to higher depreciation in the profit-and-loss account.

The Companies Act does not prohibit companies from creating treasury shares under a High Court scheme. The Companies Bill prohibits this, and a transferee company cannot hold any shares in its name or in the name of a trust either on its behalf or that of its subsidiary/ associate companies. Such shares should be cancelled or extinguished. The accounting of treasury shares is often misused. Currently, companies recognise dividend income on treasury shares and gain/ loss arising on sale of treasury shares in the profit-and-loss statement. This is inappropriate because any income cannot be derived by transacting with oneself. Such practices will not be possible if the Bill becomes an Act and is also aligned to IFRS.

The Institute of Chartered Accountants of India recently proposed a revised IFRS roadmap, which is also endorsed by the National Advisory Committee on Accounting Standards. According to this roadmap, IFRS implementation will be staggered, beginning from April 1, 2015. Of the two main hurdles to smooth implementation of IFRS, the one with respect to Companies Bill has been removed, while the other related to tax accounting standards needs to be resolved in the coming months.

Article by Dolphy D'Souza is Partner and National Leader – IFRS Services in a member firm of Ernst & Young Global

Depreciation under new companies Act with effect from 1.4.2014 Schedule XIV of the old companies Act 1956 specified minimum rates of depreciation to be provided by a company. Unlike that, Schedule II to the 2013 Act requires systematic allocation of the depreciable amount of an asset over its useful life. The Ministry of Corporate Affairs (MCA) vide its Notification dated 26-03-2014 has appointed 1.04.2014 as the date from which Schedule II comes into force.

Useful Life

Unlike the Companies Act, 1956, Useful lives of the assets have been prescribed instead of rates of depreciation in Part C of Schedule II of the Companies Act, 2013, as a base for computing depreciation. All companies shall be classified into three categories to determine the application of useful lives.

1. In prescribed class of Companies who comply with Accounting Standards prescribed for them, such companies can opt either to use useful lives and residual values prescribed in Schedule II or different useful lives or residual value for their assets, provided they disclose justification for the same. This class of companies is yet to be notified.

2.Class of Companies or Class of assets, whose useful lives or residual values are prescribed by any statutory authority or legislation (Electricity companies, Insurance companies etc.,): These companies will use depreciation rates or useful lives and residual values prescribed by relevant authority or legislation for depreciation purposes.

3.Other companies: The useful life of an asset will not be longer than the useful life and residual value will not be higher than that prescribed in the schedule.

The crux to the above discussion says that, whether as per the schedule or not, depreciation will be based on the useful life of assets.

Component Approach

The useful lives prescribed in Part C of Schedule II pertain to whole of the assets. Where cost of a component of the asset is significant to the total cost of the asset and useful life of that component differs from that of the asset, then the useful life of that component shall be determined separately and depreciation is calculated accordingly. This is called Component Approach. This concept of accounting which was hitherto not there has been introduced with the Companies Act, 2013. This approach is in consonance with the depreciation computation prescribed in Indian Accounting standards (Ind AS16).

Depreciation on Revalued Assets

As of now, in case of Revaluation of Assets the following accounting treatment was in vogue; depreciation arising on account of upward revaluation of Fixed Assets is to be transferred from Revaluation Reserve to Profit & Loss account. The aforesaid accounting treatment is prescribed as per Guidance note given by our Institute (ICAI) on "Treatment of Reserve created on Revaluation of Fixed assets", which specifies that only depreciation pertaining to historical cost needs to be provided out of current profits of the company.

But now the concept is altogether different.

The depreciable amount of an asset is the cost of an asset or other amount substituted for cost, less its residual value.

Therefore, in case of revaluation, depreciation will be based on the Revalued amount. Consequently, the ICAI Guidance Note may not apply and full depreciation on revalued amount is expected to be provided.

Transitional Provisions

The carrying amount of the asset as on 01.04.2014 will be depreciated over the remaining useful life of the asset according to the Companies Act, 2013 and if the remaining useful life is nil, then any carrying cost remained apart from Residual Value will be recognized in the opening retained earnings.

Depreciaiton Methods

Apart from Straight Line and Written Down Value Methods of Depreciation, Unit of Production Method is also an acceptable method of depreciation under the new Act.

Other provisions

In case, any addition has been made to any asset, or where any asset has been sold, discarded, demolished or destroyed during any financial year, the depreciation on such assets shall be calculated on a pro rata basis from the date of such addition or, as the case may be, up to the date on which such asset has been sold, discarded, demolished or destroyed.

This provision is same as contained in the old act.

Under the old Act assets whose actual value does not exceed ₹ 5000 shall be provided depreciation at 100%. But there is no such specific provision under the Companies Act, 2013.

IFRS: IMPACT IN THE ASSET ACCOUNTING CYCLE

An asset accounting cycle is akin to our Working capital cycle. It comprises of a purchase or in house production, consumption for business or capital appreciation and final disposal. This article envisages the application of various IFRS in the asset accounting with some significant changes brought out in the new standards.

To start with a depiction to capture the important Accounting standards during the asset accounting cycle,

Purchase/In House creation

IAS-16 / IAS – 40, IAS-17, IAS-38 and IFRS-3

Consumption and Maintenance

IAS-16, IAS-20, IAS-21, IAS-36, IAS-38, IAS- 40

Holding until Disposal

IFRS-5

Disposal

IAS-16 /IAS – 40

On Acquisition:

When asset is acquired, the accounting has to be done based on the mandates in IAS-16 or IAS-40 depending on the holding intentions of the management. IAS-40 can be called a sub sect of IAS-16 in so far as the definition of the Property, plant and Equipment (PPE) is concerned due to inclusion of the words 'for Rental or administrative purpose' within the definition of PPE. As per both these standards, the initial recognition has to be done on 'Cost' Basis. The word 'Cost' is fine tuned to make it cash equivalent or in other words, the finance charge implicit due to deferred credit terms is not included in the asset cost. This falls in line with the revised definition for 'Revenue' in IAS-18. The major inclusions for arriving at cost as prescribed in the new standard is as below,

· Inclusion of an initial estimate of future dismantling cost if there already exists an obligation at the inception. We already know that cost to bring to the current location and condition is an inevitable portion of cost whether it is inventory or fixed asset. Care is needed to include the dismantling cost only once and not again for cost of the next replaced asset under the caption' Costs to bring to the current location and condition'. This also requires a change of mindset.

· Major Inspection cost is sought to be included if it is necessary to start operation of the asset. Record Maintenance upsurges with this.

· Cost of Major spare parts is proposed to be capitalized. All along there was no clear guidance except for those spares which are used only for specific machinery and could be capitalized.

Don't these changes impact the P&L favorably? All other governances by IAS-38 on Intangible assets, IAS-17 for leased assets or IFRS-3 for takeover in Business combination remain status quo in more than one ways, except that the IFRS-3 narrows down the initial recording of assets and liabilities at 'Fair Value' basis ONLY and also mandates inclusion of any contingent consideration at Fair value basis.

Consumption and Maintenance:

Asset consumption is nothing but depreciation. In IAS-16 Depreciation is defined with a wider corridor by suitably including the words' number of production or other similar units' in the meaning of the term 'Useful life'. This implies allowing the usage of Production unit method to calculate Depreciation. In fact production unit method is more suitable for manufacturing companies since the depreciation so computed can be a best representative of 'Asset turnover Ratio'.

The other significant path breaker is allowance of depreciation till the time of actual de recognition of the asset from the books. Earlier depreciation was made to stop once the asset is retired from active use and account at Net Realizable value. In effect the entity has a choice to either classify the asset as 'Noncurrent asset held for sale' as per IFRS-5 and adopt 'fair value' basis or carry on with depreciation until realization.

One more thought provoker is the treatment prescribed for subsequent component replacements. Whenever a component is to be replaced, the replacement cost of the new component has to be added and the unamortized cost of the replaced old component has to be reduced. But tough times are ahead for the corporate world since the cost of each integral component of an asset and Inspection costs has to be maintained separately. This can be facilitated if it is an in house production. But can/will suppliers issue an Invoice setting out the price component wise? This may be a little harsh as it implies the supplier has to literally share his cost sheet with the buyer!

Subsequent Measurement of a PPE can be using 'Revaluation Model' whereas for an Investment Property what is permitted is 'Fair Value' Model. There are two differences between these two models,

1. Depreciation is permitted after revaluation, whereas not permissible under Fair value Model. Inherently a Fair value measurement is more frequent than 'Revaluation', since the latter once adopted will need revaluation only at an interval of 3-5 years (as per standard) unless there is more fluctuation in market values.

2. Any Revaluation surplus is stashed in the 'Other Comprehensive Income' whereas changes to Fair value are routed through P&L. The logic exhibited is, once fair value is adopted there is an association with the market which is a synonym of 'short term' where the related changes will impact the current period and hence debited/credited to P&L.

Other incidences such as Impairment testing, accounting for Government grants, foreign currency fluctuations and amortization of intangibles are governed in the same manner except for few minor changes.

Holding till Disposal stage:

Subject to the conditions specified in the IFRS-5 being satisfied, the management can account a Noncurrent asset held for sale on 'Fair value' basis. On Common sense basis there is no possibility/need for depreciation during this stage. The essence of our current AS-24(Discontinuing operations) is visible in this new standard. All changes to Fair value are effected through P&L.

On Disposal:

There are no major changes in this area. All gain/loss are debited/credited to Income statement.

On the whole there has been an attempt to bring in more discipline and accuracy in Asset accounting. Though there are bound to be practical difficulties in initial stages, with the advent of new technology and sophisticated ERP software anything can be made easier.

Convergence of AS 9 with IAS 18

The new AS 9 or the offspring of IAS-18 comes with a tinge of maturity to the most fundamental concept of Revenue. A comparative analysis between the existing definition as per AS-9 (old) and the new definition proposed to be introduced as per AS-9 ( new) is presented below.

The existing definition reads as in these italics,

Revenue is the gross inflow of cash, receivables or other consideration arising in the course of the ordinary activities of an enterprise from the sale of goods, from the rendering of services, and from the use by others of enterprise resources yielding interest, royalties and dividends

The new definition available for Revenue in the converged AS-9 (IAS 18)is,

The gross inflow of economic benefits during a period arising in the course of ordinary activities when those inflows result in increases in equity, other than increases relating to contributions from equity participants.

The term Economic Benefits gives or would impart a wider connotation for inclusion of certain other elements in the term Revenue. For e.g. the recognition of Fair value relating to Customer Loyalty credits.In international GAAP under "IFRIC 13, Customer Loyalty Programs" it is allowed to recognise such revenue.

2. Fair Value: is the amount for which inventory could be exchanged between knowledgeable buyers and sellers in the market place.

Measurement:

At lower of cost and net realisable value

Differences:

S. No

AS 2

IAS 2

1.

Excludes work-in-progress of service providers

Includes work-in-progress of service providers

2.

Deferred payments are not dealt with separately

Element of interest if any inthe purchase of inventories to be recognized separately

3.

Excludes selling & distribution costs as elements of cost

Excludes only selling costs

4.

Does not deal with reversal of write-down of inventories

Includes details of reversal of write-down

5.

Limited disclosures

Extensive disclosures

IND AS Carve outs in IFRS 2016

What is complete set of Financial statements

Schedule 3 ( III ) of Companies Act 2013 - format for financial statements (IGAAP Schedule III and IND-AS Schedule III), clause 33 format for stock exchanges and format for newspaper publication of results Schedule III of the Companies Act, 2013 contains a format for preparation and presentation of financial statements. . Except for addition of general instructions for preparation of Consolidated Financial Statements (CFS), the format of financial statements given in the Companies Act, 2013 is the same as the revised Schedule VI notified under the Companies Act, 1956.

It maybe noted the required changes as per IFRS and other improvements were already made in the revised Schedule VI and hence no further changes are required to be made while moving from Revised Schedule VI to new Schedule III

CASHFLOW STATEMENT

NOTES TO ACCOUNTS

Companies Act, 2013 : All provisions relating to Financial Statements

Financial Year

Financial Year was not defined in the Companies Act, 1956 (hereinafter “1956 Act”).

Financial Year as defined in Clause 2(41) of the Companies Act, 2013 (hereinafter “2013 Act”) says

·Company or body corporate required to adopt uniform financial year of 1st April to 31st March every year,

·Companies incorporated on or after first day of January of a year, the period ending on 31st day of March of following year will be considered as financial year,

A company or body corporate existing on the commencement of the 2013 Actshall, within a period of two years from such commencement,align its financial year as per the above mentioned provision.

Exception

A company which is a holding or subsidiary of a company incorporated outside India and is required to follow the different financial year for consolidation outside Indiacan make an application to the Tribunal. The Tribunal can allow any period as its financial year after being satisfied.

Financial Statements

As per Sec 2(40) of the 2013 Act, financial statements of a company includes:-

·Balance Sheet as at the end of financial year.

·Statement of Profit & Lossor Income & Expenditure Account for the financial year.

·Cash Flow Statement for the financial year

·Statement of Changes in Equity, if applicable

·Any explanatory note annexed to, forming part of the documents mentioned above.

Exceptions

One Man Company, Dormant Company, Small Company are not required to prepare Cash Flow Statement.

Consolidation of Financial Statements

Section 212 of the 1956 Act providedfor attachment ofaccounts ofsubsidiaries alongwith the holding company accounts.No provision forconsolidation.

Section 129 of the 2013 Act provides that where a company has one or more subsidiaries, it shall prepare a consolidated financial statement of thecompany and of all the subsidiaries in the same form and manner as that of its own whichshall also be laid before the annual general meeting of the company.

A separate statement containing the salient features of the financial statement of its subsidiary orsubsidiaries is to be attached with the holding company’s financial statements.

Signing of Financial Statements

Financial Statements to be signed at least by:-

·Chairperson of the company, if authorised

·2 directors including MD

·CEO, if he is a director

·CFO and CS wherever they are appointed

Exceptions

In case of OPC, Balance Sheet and Statement of Profit & Loss are to be signed by one director only.

Voluntary Revision of Books of Accounts

Board of Directors may prepare revised financial statement and board report in respect of any of the 3 preceding financial years after obtaining the approval from NCLT, if they believe that financial statements or report does not comply with the relevant provisions.

Mandatory Reopening / Recasting of books of accounts

A company can reopen its books of accounts or recast its financial statements on an application made by CG, IT authorities, SEBI or any other statutory regulatory authority and on an order being made by a Court or NCLT, on the below grounds:

·relevant earlier accounts were prepared in a fraudulent manner, or

·affairs of the company are mismanaged during the relevant year giving a doubt on the reliability of the financial statements.

Audited Accounts

Audited Accounts of all the subsidiaries are required to be provided to the shareholders on request.

Maintenance of Books of Accounts

·According to Section 128 of 2013 Act, books of accounts are required to be maintained in electronic mode as prescribed.

·Books of Accounts are required to be kept for 8 years.

Exception

CG may direct to keep the books of accounts for the longer period, where any investigation has been ordered.

Major differences between U.S. GAAP and IFRS

1. Error correction. According to IFRS rule IAS 8, it's not always necessary to retrospectively restate financial results when a company corrects errors, especially if the adjustment is impractical or too costly. U.S. GAAP, on the other hand, requires restatements in many error-correction cases.

2. Death of LIFO. Last-in, first-out inventory accounting is prohibited under IAS 2, so any American company using the method will have to abandon it (and the tax benefits) and move to another methodology. Although LIFO is permitted under U.S. GAAP, the repeal of LIFO for tax purposes is an ongoing debate.

3. Reversal of impairments. IAS 36 permits companies to reverse impairment losses up to the amount of the original impairment when the reason for the charge decreases or no longer exists. However, U.S. GAAP bans reversal.

4. PP&E valuation. IAS 16 allows for the revaluation of property, plant, and equipment, but the entire asset class must be revalued. A company can choose to use the revaluation model if its fair value can be measured reliably.U.S. GAAP does not allow revaluation.

5. Component depreciation. Also under IAS 16, companies must recognize and depreciate equipment components separately if the components can be physically separated from the asset and have different useful life spans. In practical terms, that means controllers will have to rely on the operations side of the business to help assess equipment components. U.S. GAAP allows component depreciation, but it is not required.

6. Development costs. Based on IAS 38, companies are permitted to capitalize development costs as long as they meet six criteria. However, research costs are still expensed. U.S. GAAP requires that all R&D costs be charged to expense when incurred.

AS applicable for small entities in India for whom IND-AS is not mandatory

AS 21, AS 23 and AS 27

Consolidation of Jointly Controlled Entity as per AS 27 What is a Joint Venture:

A joint venture is a contractual arrangement whereby two or more parties undertake an economic activity, which is subject to joint control.

Two Important Words:

1. Joint control is the contractually agreed sharing of control over an economic activity. 2. There is no definition for the contractual arrangement. It may be evidenced in a number of ways, for example by a contract between the venturers or minutes of discussions between the venturers. In some cases, the arrangement is incorporated in the articles or other by-laws of the joint venture. Whatever its form, the contractual arrangement is normally in writing and deals with such matters as:

(a) the activity, duration and reporting obligations of the joint venture;

(b) the appointment of the board of directors or equivalent governing body of the joint venture and the voting rights of the venturers;

(c) capital contributions by the venturers; and

(d) the sharing by the venturers of the output, income, expenses or results of the joint venture.

The existence of a contractual arrangement distinguishes interests which involve joint control from investments in associates in which the investor has significant influence (see Accounting Standard (AS) 23, Accounting for Investments in Associates in Consolidated Financial Statements). Activities which have no contractual arrangement to establish joint control are not joint ventures for the purposes of this Statement (AS 27).

Jointly Controlled Entity:

A jointly controlled entity is a joint venture which involves the establishment of a corporation, partnership or other entity in which each venturer has an interest. The entity operates in the same way as other enterprises, except that a contractual arrangement between the venturers establishes joint control over the economic activity of the entity.

Consolidation of JCE:

JCE should be consolidated as per Proportionate Consolidation method. Under this method the consolidated balance sheet of the venturer includes its share of assets and liabilities. The profit and Loss account includes its share of expenses and incomes.

Note:

As per AS 23, an associate is an enterprise in which the investor has significant influence and which is neither a subsidiary nor a joint venture of the investor.So applicability of AS 27 (and AS 21) supersedes the applicability of AS 23.

IND-AS 115 - Revenue from Contracts with Customers.

From April 1, 2018 AS 115 replaced the earlier revenue standards — Ind AS 18 - Revenue, and Ind AS 11 - Construction Contracts.

Revenue — which reflects an entity's growth and financial performance — is one of the most important components in a financial statement. Ind AS 115 directs companies to follow the most conservativeapproach while recognising revenue. It also prescribes more extensive qualitative and quantitative disclosures than the earlier revenue standards.

Though the financials of almost all companies have been impacted by the new accounting standard, there is a more notable change in the reporting done by entities in real estate, IT and hospitality.

The transition

Before taking a look at how this new standard has affected key sectors, it is important to understand the options available and the provisions applicable in the move from Ind AS 18/11 to Ind AS 115.

Once a company begins applying Ind AS 115, it can either restate the financial statements of the prior accounting year (2017-18) as per the new standard, or adjust the opening reserves — as of April 1, 2018 — as regards incomplete projects for which revenue was partially recognised in the previous period (as per Ind AS 18/11). Most of the companies have chosen the latter option by adjusting the retained earnings at the beginning of the year without restating the previous financial statements. This makes the reporting in this financial year uncomparable with the corresponding figures in the previous year.

Impact on real estate

Ind AS 115 has had a striking impact on the real estate sector. The new accounting standard directs companies to recognise the revenue in a more conservative manner — only when the collections from customers become 'probable'.

Ind AS 115 allows using the percentage of completion method (POCM) to recognise revenue, albeit with explicit and specific requirements. POCM implies that until certainty is achieved, at every stage of a project, revenue is to be recognised only to the extent of cost, and the margins gets deferred to the period in which the project phase attains certainty.

Certainty essentially implies the ability of the company to gauge the progress of each stage in a project.

Under the earlier Ind AS 11, as long as there was certainty attached to the entire project — not necessarily to each stage — companies could recognise revenue as cost plus margin.

Aside from POCM, companies can also report revenues under the project completion method. Here, the revenue is completely deferred, and recognised only in the quarter in which the project is completed. Till then, even payments received from customers have to be shown under loans or advances from customers.

Here's a closer look at how various real-estate companies reported their revenues during the quarter ended June 30, 2018.

Retaining POCM

With the transition to Ind AS 115, most of the companies that earlier used POCM continue to follow the same method to recognise revenues. The rest of the real-estate players have shifted to the project completion method. For example, Oberoi Realty's earnings call shows that the firm still follows the POCM. But given that it reported revenues, including margins, for two of its projects as per the earlier regime, there has been an adjustment in its opening reserves as of April 1. The two projects were Sky City, and Eternia and Enigma. In the June quarter, revenue (including profit) was recognised for Sky City as it had crossed certainty. But for the other project — progress on which was not certain then — revenue was reported only to the extent of cost.

Application of Ind AS 115 reduced Brigade Enterprises'consolidated retained earnings as of April 1, 2018 by ₹406 crore. However, Ind AS 115 helped raise its revenue and net profit for the quarter ended June 30 by ₹123 crore and ₹36 crore, respectively. A significant impact is also evident in the firm's EPS — ₹4.63 (as per Ind AS 115), compared with ₹1.96, had it followed Ind AS 11.

Deferring revenue

Sobha Developers shifted to the project completion method beginning this financial year. The transition brought about considerable changes in how the company recognised revenue. The company's retained earnings as of April 1, 2018 were reduced by a whopping 757 crore due to postponing of revenue from unfinished projects.

As the firm adjusted the opening reserves and did not restate the financial statements, revenue for the first quarter of FY 2019 cannot be compared with the figures for the corresponding period in the previous financial year. Therefore, revenue for the June quarter was down ₹203 crore compared with the same quarter last year. Had it followed the earlier accounting method, the revenue would have increased 18 per cent y-o-y.

Takeaway

As the new standard lacks clarity, realty firms have come up with their own interpretations. Under Ind AS 115, the profits may not reflect the actual performance of the company in that particular period. Therefore, if you track real-estate companies, bear in mind that, given the changes in accounting methods, you should not consider merely the quarterly profits. Instead, take a close look at projects in pipeline to get a better picture of the likely revenue over the coming quarters.

Impact on other sectors

IT Servcies

'Remaining performance obligations' and 'disaggregated revenue' — two new disclosures under Ind AS 115 — provide more transparency. These disclosures are applicable to all companies across sectors. However, disclosures made by services companies in the information technology and construction sectors are more meaningful due the continuing nature of their contracts.

The 'remaining performance obligation' disclosure reveals the aggregate amount of revenue yet to be recognised as of the end of the reporting period. It also discloses when the company expects to recognise these revenues. For example, Infosys, in its June quarter report, stated that "the aggregate value of performance obligations that are completely or partially unsatisfied as of June 30, 2018 is ₹40,936 crore (with some exclusions). Of this, the firm expects to recognise revenue of around 50 per cent within the next year and the remaining thereafter." Such disclosures help investors assess the near-future revenue inflow from existing projects.

Auto

The payment that auto companies receive when transferring vehicles to dealers for sale was earlier recognised as revenue. The costs associated with that process were presented under 'other expenses' in the statement of profit and loss. Under Ind AS 115, such revenue is to be presented net of cost. This change significantly contributed to the dip in Tata Motors' revenue and expenses — down 929 crore — in the quarter ended June 30. So, even though the company's profitability wasn't affected, revenue has become uncomparable.

Hospitality

The non-refundable admission fee collected for vacation ownership contracts is one of the key revenue segments in the hospitality sector.

A significant portion of this revenue was earlier recognised in the year of sale. According to the new standard, income from such contracts has to be recognised over the tenure of the membership; and the associated costs (except incremental) are to be charged to the profit-and-loss account for the period. Due to this change, the profit of Mahindra Holidays and Resorts was down by ₹23 crore, compared with the profits computed using Ind AS 18.

Telecommunication

Under Ind AS 115, revenue from certain items has to be recognised over the life of a contract, unlike earlier, when it was recognised — fully or substantially — in the year of sale. Tata Communication has had to bear the brunt of this alteration. Ind AS 115 is also one of the prime reasons for the decline in the company's Q1 FY19 revenue by 12.6 per cent y-o-y and 6.2 per cent q-o-q.

In the upcoming quarters of FY 2019, investors would do well to be a bit more cautious while analysing the results of these sectors. However, keep in mind that Ind AS 115 has not caused a ripple in the revenue recognition process of all companies in these segments.

Indian GAAP to Ind AS

Some revenue recognition rules were altered when the transition from Indian GAAP to Ind AS revenue standards (Ind AS 18/11) happened in April 2016. These changes continue to be effective under the Ind AS 115 as well.

Under Indian GAAP, the gross revenue and the tax paid (on sales) were shown separately in the financial statement. Ind AS requires companies to show just the post-tax revenue in the statement of profit and loss.

The Ind AS revenue standards focus on recognising the revenue on a fair-value basis, that is, after considering the time value of money.

Fair value comes into the picture when there is an in-built financing element (explicit or implicit) in the price consideration. For example, fair value is considered when the time provided for payment to a particular customer is beyond the normal credit period.

In such cases, the revenue is to be recognised at the discounted value of future cash flows, while the difference is to be recognised as interest over the tenure of the contract. As per Ind AS, a company has to recognise its interest income from investments — other than operational investments — according to the effective interest rate method, while Indian GAAP suggested the proportionate basis method.

The effective interest method takes into consideration the time value of money while calculating the interest income. Ind AS mandates considering the fair value while reporting income, in line with global reporting standards.

IND-AS 116 LEASES

IND-AS 116 Leases Impact

Note Earlier above treatment applicable only to financial lease.. Now apply to operational lease also..

Improved true and fair view of balance sheet.. Acts as disincentive to plan balance sheet. Still tax benefits on lease will keep lease option attractive

In P&L ebidta will increase ironically ..since rent is moved to Interest and depreciation

STOCK EXCHANGE Format for results

These are standard formats as prescribed

Release of Quarterly Results by listed companies As per Reg 33 of the LODR, every company shall submit quarterly, year to date and annual financial results to the stock exchange (SE) in the manner as prescribed under the clause. Further, the company has an option to submit either audited financial results with audit report or un-audited financial results subject to limited review by statutory auditors quarterly and year to date financial results to the SE within 45 days of end of each quarter (Other than last quarter). For the last quarter alone the company has an option to submit its audited financial results (both standalone and consolidated) for the entire financial year within 60 days from the end of the financial year.

Sample Consol Results

Sample Standalone Results

News Paper Publication format of Summary Results for listed companies

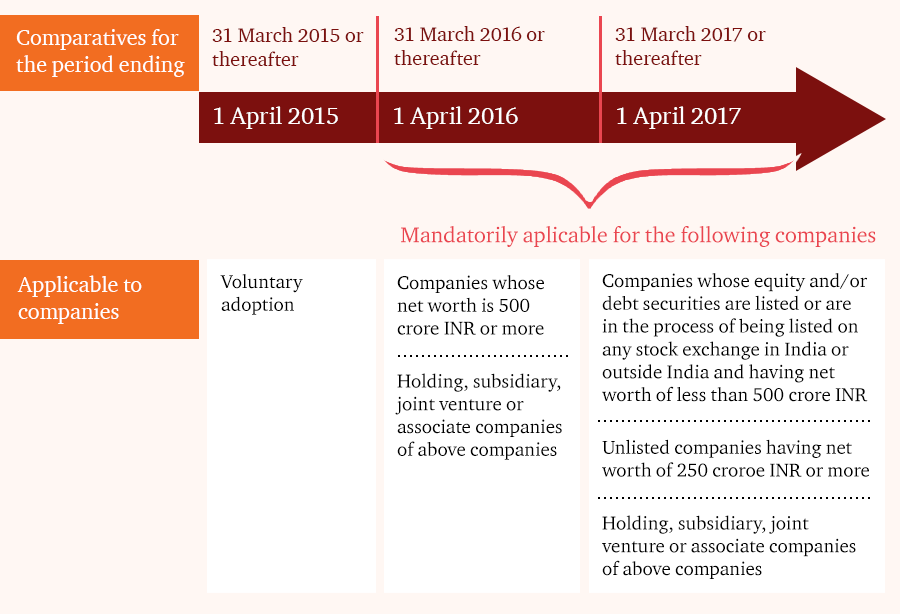

IFRS Convergence in India - Ind-AS mandatory from 2016 / 2017

Indian Accounting Standards (Ind AS) : Roadmap for IFRS Convergent Standards

Net worth

It has been clarified that net worth will be determined based on the standalone accounts of the company as on 31 March 2014 or the first audited period ending after that date.

Net worth has been defined to have the same meaning as per section 2(57) of the Companies Act, 2013. It is the aggregate value of the paid-up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not include reserves created out of revaluation of assets, write-back of depreciation and amalgamation.

Accounting standards for companies - unlisted and less than 250 crores

Segmental Reporting under AS (Old)

Scope :

For standalone Financial Statements or Consolidated Financial Statements.

If financial report contains both, then on the basis of CFS.

How many categories

1. Business Segment

Distinguishable component of an enterprise, engaged in providing an individual product or service or a group of related product or services and subject to risks and returns exclusive of other segments.

2. Geographical Segment

Distinguishable component of an enterprise, engaged in providing an individual product or service or a group of related product or services within a specific environment and subject to risks and returns exclusive of other segments.

What is to be reported under the head Segmental Revenue

Segment Revenue

Segment Expense

Segment Result

Segment Revenue ( minus ) Segment Expense

Segment Assets

Segment Liabilities

Capital Expenditure

Depreciation and other Non cash Expenditure

How to ascertain if a segment is reportable ?

Based on-

a) Revenue

Revenue of segment (external customers + internal transfers) is atleast 10% of all segments.

b) Profit or Loss

Segment result ( higher of (combined result of all segments in profits or loss)) is atleast 10% of all segments.

c) Segment assets

Segment assets are atleast 10 % of all segments. If the segment becomes reportable in any one of the above tests then it becomes a reportable segment.

d) Preceeding data

If segment reportable in previous period, then reportable in current period also.

e) Total External revenue

If external revenue of reportable segments less than 75% of total enterprise revenue additional segments to be identified as reportable until 75% of external revenue is included.

f) Management Choice

How to determine primary and secondary reporting formats?

The dominant source and nature of risks and returns of an enterprise should govern whether its primary segment reporting format will be business segments or geographical segments.

Vedanta Limited(earlier Sesa Goa) is a metals and mining gaint in India. It has following buisness segments :

Zinc-Lead-Silver: Zinc India business is owned and operated byHindustan Zinc Limited(HZL). HZL owns and operates a fully integrated zinc-lead business. HZL is one of the world's largest integrated zinc-lead producers by volume. Sesa Sterlite owns 64.9% of the share capital of HZL, while the Government of India remains an equity partner and holds a 29.5% stake. HZL is listed on Indian stock exchanges (NSE and BSE).

Oil & Gas: Sesa Sterlite's Oil & Gas operations comprise the assets ofCairn Indiain India,Sri Lankaand South Africa. Cairn India is India's largest private-sector crude oil producer, contributing to over 25% of India's crude oil production. Sesa Sterlite owns 58.9% of Cairn India, which is also the fastest-growing Asian E&P company (Platts 2011) and one of the top 20 independent E&P companies worldwide.

Iron Ore:Sesa Sterlite is largest private sector exporter of iron ore in India and is developing large iron ore deposits inLiberia. Iron ore mining operations are carried out in the Indian States of Goa and Karnataka. We also manufacture pig iron and metallurgical coke. During FY 2013, our Indian iron ore operations were affected by a suspension of iron ore mining activities across the states ofGoaandKarnataka.

Copper: they says "We aim to provide high-quality refined copper by improving our operational efficiency and reducing our unit costs" Their copper business is principally a custom smelting operation located in India and Australia.

Aluminium:BALCOhas a smelter capacity of 345 ktpa with capabilities to produce ingots, wire-rods, billets, busbars and rolled products. BALCO's operations include mines, refineries, smelters and captive power plants in the state of Chhattisgarh in India. Sesa Sterlite holds a controlling 51% stake in BALCO, while the Government of India remains an equity partner and holds the remaining 49% stake.

Power: Sesa Sterlite is one of India's leading power producers with a capacity of 3,900 MW in commercial power.

Metallurgical Coke: Approximately 65% of total production is consumed by Sesa group, for its pig iron production. The remainder is sold to customers located in India.

Pig Iron: This business is skewed towards catering to the steel mills and foundries of the Indian market, in particular the Western and Southern India. The division manufactures basic, foundry and nodular grade pig iron and also sellsslag. The annual production capacity is 250,000 tons per annum.

Tax opinion on a possible outcome - whether amounts provision or contingent liability

There are some common definitions used in tax opinion which

• Not frivolous: There is a 10 to 20 percent chance your tax argument will prevail;

• Reasonable basis: There is approximately a 1 in 3 chance that you will prevail;

• Substantial authority: There may be cases both ways, but there is approximately a 40

percent chance you will win;

• More likely than not: The odds are better than 50 percent that you will win;

• Should: There is approximately a 60 percent or higher probability that you will prevail;

and

• Will: Your desired tax treatment is virtually assured — 90 percent or better.

Probable possible remote

Paragraph 10 of IAS 37 defines a provision as "a liability of uncertain timing or amount."

Paragraph 10 of IAS 37 defines a contingent liability as "a possible obligation that arises

from past events and whose existence will be confirmed only by the occurrence or non-

occurrence of one or more uncertain future events not wholly within the control of the

entity."

Paragraph 10 of IAS 37 also includes in the definition of a contingent liability "a present

obligation that arises from past events, but is not recognised because:

(i) it is not probable that an outflow of resources embodying economic benefits

will be required to settle the obligation; or

(ii) the amount of the obligation cannot be measured with sufficient reliability."

A provision must be probable to be recognized. Probable is interpreted as more likely than

not (i.e., a probability of greater than 50 percent).