Price decreases + volume decreases = Bears don't have strength.

Hero MotoCorp Vs Bajaj Auto: Goldman Sachs’ Pick

: Differences in Firms with in a Industry March 2022

Goldman Sachs initiated coverage on Hero MotoCorp

Ltd. with a ‘sell’, but suggested a ‘buy’ for peer Bajaj Auto Ltd. “We

see the risk reward on Hero as unfavourable given high dependency (94% of

volumes) on domestic two-wheeler market where demand remains subdued,

concentrated portfolio in entry-level sub-110 cc segments where customers are

more vulnerable to the present wave of raw material-led price hikes, and higher

loan losses than peer at captive financing subsidiary,” the financial services

provider said in a March 3 report.

These factors, it said,

drive its 3.1% FY19 to FY25E top line CAGR at Hero MotoCorp versus 8% median

growth for India two-wheeler coverage. “Our FY24E EPS is 20% below consensus.”

“Diversification away from the entry-level segment, an increase in exports

penetration and the nature of response to Hero’s upcoming fixed and swappable

battery electric scooter launches are the key events that we would watch

to see success on in order to turn more optimistic.” On the other hand, Bajaj

Auto’s “meaningful export market exposure in two-wheelers, offsetting ongoing

domestic demand weakness, upcoming cyclical recovery in higher margin

three-wheeler demand, its industry leading dividend yield of 5.4%” prompts

Goldman Sachs to bet on the Pune-based company. “These factors underline

our FY22E-FY25E EPS CAGR of 21%, with FY24E EPS 6% above consensus.” Goldman

Sachs, however, cautioned that the ongoing geopolitical uncertainties,

associated volatility in raw material costs and transition toward electric

two-wheelers could impact margin of the industry.

Hero MotoCorp

Initiates coverage with a ‘sell’ rating and a

price target of Rs 2,080 apiece, indicating a downside of 13.8%. Hero

MotoCorp’s high domestic business mix is sensitive to recent price hikes and

could take longer to start showing revenue growth compared to peers. Witnessed

lowest Ebitda growth and the highest margin compression among its listed mass

market two-wheeler peers (Bajaj Auto and TVS Motor Co. Ltd.) Missed out

on the two key market shifts in the motorcycles segment—exports market

development and premium motorcycles growth. Lost market share in 11 of the past

12 years since split with Honda. Non-performing assets at Hero FinCorp could

weigh on capital allocation flexibility. Slower to market in the

electric scooter space versus Bajaj and TVS, both of which have already

launched their electric scooters and have been competing for more than 12

months.

Bajaj Auto

Initiates coverage with a

‘buy’ and a price target of Rs 4,270 apiece, indicating an upside of 27%.

Benefit of exports market exposure where emission-related price hikes have been

less of a challenge. CNG network expansion by the Indian government to further

support Bajaj’s three-wheeler volumes. Upside optionality from plans to set up

captive financing arm. Expected recovery in domestic three-wheeler

market to benefit Bajaj more than peers. Low exposure to scooters and mopeds

which are more at risk from EV-led disruption.

share turnover velocity(ratio of traded turnover to market capitalisation) If share turnover velocity is an indicator of the breadth of activity and liquidity in the market. Share turnover velocity is the ratio of traded turnover to market capitalisation. Higher the ratio, better the liquidity and more widespread the activity in the market. Globally, investors are attracted to markets with high share turnover velocity as it means lower impact costs (the cost of entering and exiting a stock). In stock markets across the globe, share turnover velocity has been on the rise over the past, one-and-a-half years. In India, the trend has been the opposite, with share turnover velocity declining steadily. Experts attribute factors like concentration of trading in few stocks and high-promoter holding in companies to this trend.

As per World Federation of Exchanges’ data. Share turnover velocity in some of the developed world stock exchanges like Nasdaq, NYSE, Shenzhen Stock Exchange, Taiwan Stock Exchange, BME Spanish, Borsa Italiana, Tokyo Stock Exchange and Deutchse Borse is very high and in many cases runs to over 100%. If there is very low market participation, trading is concentrated to a few players.

5/12/2007 Mutual funds exposure to equity compared to debt is a good indicator of perceived riskiness of market.(But there could be other reasons for changes in ratios)

The equity exposure of Indian mutual funds (MFs) in the secondary market has come down by 37% in FY07 as compared to FY06. The MFs invested Rs 9,062 crore in FY07 as compared to Rs 14,302.20 crore a year earlier. The trend has continued even in the first month of the new financial year. In April 2007, MFs exposure to equity was at Rs 1,022 crore while in April 2006 it stood at Rs 2,850 crore.

MFs' net exposure to debt segment grew 43% in FY07 to Rs 52,543.46 crore from the previous year's Rs 36,801.24 crore.

This sharp rise in MFs' exposure to debt segment in FY07 can be mostly attributed to the fact that fixed maturity plans (FMPs) have gained popularity among the investors during the period. The MFs' exposure to equity in FY06 was higher as during the year, there were large number of equity new fund offerings (NFOs) mobilising resources from the retail investors.

An indicator is anything that can be used to predict future financial or economic trends. For example, the social and economic statistics published by accredited sources such as U.S. government departments are indicators. Popular indicators include unemployment rates, housing starts, inflationary indexes and consumer confidence. Official indicators must meet certain set criteria; there are three categories of indicators, classified according to the types of predictions they make.

New Fund launches data by AMFI

SIZE OF INDIAN STOCK MARKET

Economic Indicators followed by stock market analysts

Lead Indicators - These types of indicators signal future events. Think of how the amber traffic light indicates the coming of the red light. In the world of finance, leading indicators work the same way but are less accurate than the street light. Bond yeilds are thought to be a good leading indicator of the stock market because bond traders anticipate and speculate trends in the economy (even though they aren't always right).

Lag Indicators :A lagging indicator is one that follows an event. Back to our traffic light example: the amber light is a lagging indicator for the green light because amber trails green. The importance of a lagging indicator is its ability to confirm that a pattern is occurring or about to occur. Unemployment is one of the most popular lagging indicators. If the unemployment rate is rising, it indicates that the economy has been doing poorly. Major Indicators followed by stock markets in India are Index of industrial production (IIP) Industrial output figures are released by the Ministry of Statistics and Programme Implementation every month within 40 days from end of month.They are one the important lag indicator

Advance tax numbers

Advance tax numbers 15th June, 15th Sep 15th Dec and 15th march give indication of the upcoming Quarterly results

Auto Sales Numbers

Auto companies release their sales data every month. That allows volatility in auto stocks every month even before quarterly results

US Payroll numbers :

Payroll data impact can be both ways as below :

Stocks climb on Weak Jobs Data

Surprisingly weak jobs data eased fears about higher inflation and a stimulus cutback. The dollar slumped toward the lowest since February and stocks climbed.

Moving Averages

Moving averages allow traders the ability to quantify trends and act as signals for entries, exits, and trailing stops. They can become support and resistance, and give the trader levels to trade around. Below are examples of the specific moving averages with time frames.

5 Day EMA: Measures the short term time frame. This is support in the strongest up trends. This line can only be used in low volatility trends.

10 day EMA: “The 10 day exponential moving average (EMA) is my favorite indicator to determine the major trend. I call this ‘red light, green light’ because it is imperative in trading to remain on the correct side of a moving average to give yourself the best probability of success. When you are trading above the 10 day, you have the green light, and you should be thinking buy. Conversely, trading below the average is a red light. The market is in a negative mode, and you should be thinking sell.” – Marty Schwartz

21 day EMA: This is the intermediate term moving average. It is generally the last line of support in a volatile up trend.

50 day SMA: This is the line that strong leading stocks typically pull back to. This is usually the support level for strong up trends. Use 50 Day Average For Trading Signals

100 day SMA: This is the line that provides the support between the 50 day and the 200 day. If it does not hold as support, the 200 day generally is the next stop.

200 day SMA: Bulls like to buy dips above the 200-day moving average, while bears sell rallies short below it. Bears usually win and sell into rallies below this line as the 200 day becomes resistance, and bulls buy into deep pullbacks to the 200 day when the price is above it. This line is one of the biggest signals in the market telling you which side to be on. Bull above, Bear below. Bad things happen to stocks and markets when this line is lost.

Rollovers in F&O market- As an indicator

WHAT IS A ROLLOVER?

Rollover involves carrying forward of futures positions from one series, which is nearing expiry date, to the next one. On expiry, traders can either let a position lapse or enter into a similar contract expiring at a future date. Rollovers happen only in futures and not in options.

HOW ARE CONTRACTS ROLLED OVER IN INDIA? HOW DOES IT WORK?

Equity derivatives contracts in India are settled on the last Thursday of every month (if Thursday is a holiday, the settlement happens on a Wednes day). While rollovers are done till the close of trading hours on that day, a chunk of the rollovers begin a week before expiry. Positions are rolled over to the next month through a spread window on the trading terminal. For instance, if a trader holds one futures contract of Nifty expiring in June, he would enter the `carry-forward this position to June' by keying in the spread at which he desires to rollover the positions to July. The spread window has made it easier for traders to rollover, which was a two-step process earlier.

HOW TO INTERPRET ROLLOVERS?

Rollover is expressed as a percentage of total positions. There are no benchmarks for rollovers but they are compared on the basis of historical data, especially the trailing three-month average.

Rollover is an indicator of traders' willingness to carry forward the bets on the market. But, the figures will not tell you in which direction traders have bet. On most occasions, lower-thanaverage rollovers signal uncertainty while higher rollovers show that sentiment is strong. Hypothetically, if rollover in Nifty futures from May series to June is at 70% and three-month av erage is 65%, it means traders are more con vinced about their views on the market and are willing to build more positions.

However, at times, rollover trends can be misleading. For instance, 70% roll over may have taken place at a lower base of open interest -number of outstanding positions -while the average of 65% rolls would have happened at a relatively higher open interest base. Savvy traders also analyse rollover trends on the basis of rollover cost. “Usually, high rollover costs signal that the mood is upbeat in the market,“ said K Anant Rao, an independent derivatives analyst.

Nishanth Vasudevan

ECONOMICTIMES.COM 27.6.14

Technical Analysis on Stock Market : Reading the charts

Technical analysis on stock market

Technical analysisis a method of evaluating securities by analyzing the statistics generated by market activity. It is based on three assumptions: 1) the market discounts everything, 2) price moves in trends and 3) history tends to repeat itself.

Technicians believe that all the information they need about a stock can be found in its charts.

Technical traders take a short-term approach to analyzing the market.

Criticism of technical analysis stems from theefficient market hypothesis, which states that the market price is always the correct one, making any historical analysis useless.

One of the most important concepts in technical analysis is that of atrend, which is the general direction that a security is headed. There are three types of trends:uptrends,downtrendsandsideways/horizontal trends.

Atrendlineis a simple charting technique that adds a line to a chart to represent the trend in the market or a stock.

Achannel, or channel lines, is the addition of two parallel trendlines that act as strong areas of support and resistance.

Supportis the price level through which a stock or market seldom falls.Resistanceis the price level that a stock or market seldom surpasses.

Volumeis the number of shares or contracts that trade over a given period of time, usually a day. The higher the volume, the more active the security.

A chart is a graphical representation of a series of prices over a set time frame.

The time scale refers to the range of dates at the bottom of the chart, which can vary from decades to seconds. The most frequently used time scales areintraday, daily, weekly, monthly,quarterlyand annually.

The price scale is on the right-hand side of the chart. It shows a stock's current price and compares it to past data points. It can be eitherlinearorlogarithmic.

There are four main types of charts used by investors and traders:line charts,bar charts,candlestick chartsandpoint and figure charts.

A chart pattern is a distinct formation on a stock chart that creates a trading signal, or a sign of future price movements. There are two types:reversalandcontinuation.

Ahead and shoulders patternis reversal pattern that signals a security is likely to move against its previous trend.

Acup and handle patternis a bullish continuation pattern in which the upward trend has paused but will continue in an upward direction once the pattern is confirmed.

Double topsanddouble bottomsare formed after a sustained trend and signal to chartists that the trend is about to reverse. The pattern is created when a price movement tests support or resistance levels twice and is unable to break through.

Atriangleis a technical analysis pattern created by drawing trendlines along a price range that gets narrower over time because of lower tops and higher bottoms. Variations of a triangle includeascendinganddescendingtriangles.

Flagsandpennantsare short-term continuation patterns that are formed when there is a sharp price movement followed by a sideways price movement.

Thewedgechart pattern can be either a continuation or reversal pattern. It is similar to a symmetrical triangle except that the wedge pattern slants in an upward or downward direction.

Agapin a chart is an empty space between a trading period and the following trading period. This occurs when there is a large difference in prices between two sequential trading periods.

Triple topsandtriple bottomsare reversal patterns that are formed when the price movement tests a level of support or resistance three times and is unable to break through, signaling a trend reversal.

Arounding bottom(or saucer bottom) is a long-term reversal pattern that signals a shift from a downward trend to an upward trend.

Amoving averageis the average price of a security over a set amount of time. There are three types:simple, linear andexponential.

Moving averages help technical traders smooth out some of thenoisethat is found in day-to-day price movements, giving traders a clearer view of the price trend.

Indicatorsare calculations based on the price and the volume of a security that measure such things as money flow, trends, volatility and momentum. There are two types:leadingandlagging.

Theaccumulation/distributionline is a volume indicator that attempts to measure the ratio of buying to selling of a security.

Theaverage directional index(ADX) is a trend indicator that is used to measure the strength of a current trend.

TheAroon indicatoris a trending indicator used to measure whether a security is in an uptrend or downtrend and the magnitude of that trend.

The Aroon oscillator plots the difference between the Aroon up and down lines by subtracting the two lines.

Themoving average convergence divergence(MACD) is comprised of two exponential moving averages, which help to measure a security'smomentum.

Therelative strength index(RSI) helps to signal overbought and oversold conditions in a security.

Theon-balance volume(OBV) indicator is one of the most well-known technical indicators that reflects movements in volume.

Thestochastic oscillatorcompares a security's closing price to its price range over a given time period.

Retracement Or Reversal: Know The Difference

Most of us have wondered, at some point, whether a decline in the price of a stock we're holding is long term or a mere market hiccup. Some of us have sold our stock in such a situation, only to see it rise to new highs just days later. This is a frustrating and all too common scenario, but it can be avoided if you know how to identify and trade retracements properly.

What Are Retracements?Retracements are temporary price reversals that take place within a larger trend. The key here is that these price reversals are temporary, and do not indicate a change in the larger trend.

The Importance of Recognizing RetracementsIt is important to know how to distinguish a retracement from a reversal.

Factor

Retracement

Reversal

Volume

Profit taking by retail traders (small block trades)

Institutional selling (large block trades

Short Interest

*No change in short interest

Increasing short interest

Time Frame

Short-term reversal, lasting no longer than one to two weeks

Long-term reversal, lasting longer than a couple of weeks

Fundamentals

No change in fundamentals

Change or speculation of change in fundamentals

Recent Activity

Usually occurs right after large gains

Can happen at any time, even during otherwise regular trading

Psychology in Stock Markets

Positive and negative feedback loop

When stocks are rising (a bull market), the belief that further rises are probable gives investors an incentive to buy (positive feedback—reinforcing the rise, see also stock market bubble and momentum investing); but the increased price of the shares, and the knowledge that there must be a peak after which the market falls, ends up deterring buyers (negative feedback—stabilizing the rise).

Industry Weightages In Nifty

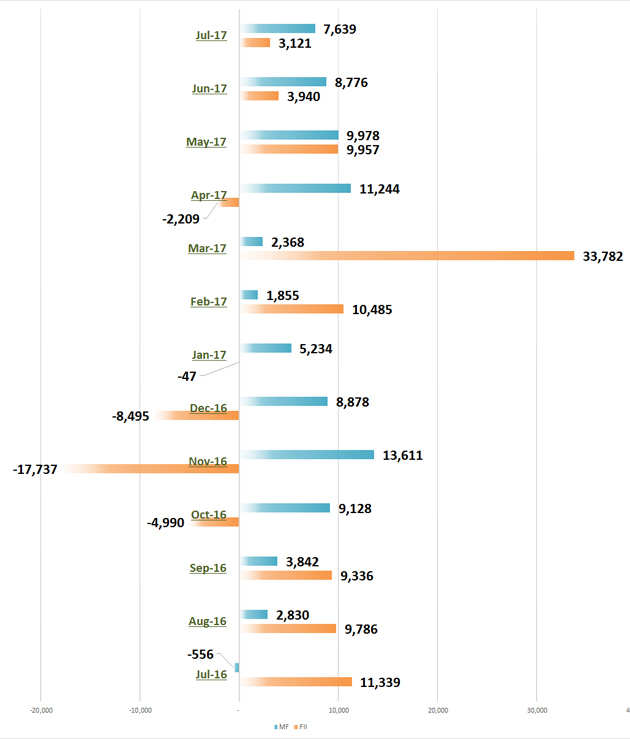

Domestic Investors (DII) buying more than FII in India in 2017

To clear the situation, we delve deeper and find out how analysts are placed on each of these stocks where the big investors have taken a contrasting stand.

The stock market is soaring high with abundant liquidity keeping the market buoyant even as companies have struggled to put on a good show. Both foreign and domestic investors have pumped in truck-loads of money over the past one year. However, contrary to the past trends, this time, domestic investors have taken the lead in boosting the market. While foreign institutional investors (FIIs) have bought equities worth Rs 58,268 since July last year,domestic institutional investors (DIIs) have made a bigger splash in the market with net inflows of Rs 84,825 crore. In fact, DIIs have emerged net buyers in the equity market for each month since August last year.

For 196 of the 200 firms in the BSE200 Index, non-promoter foreign institutional ownership increased marginally from 19.18% in June last year to 19.56% at the end of June 2017. Meanwhile, DII holding in the same basket rose from 10.71% to 11.48% during this period.

More interestingly, both sets of investors have taken different paths while buying and sellingstocks. Our study of the shareholding pattern of the BSE200 basket of companies shows that there is not a single company in which both DIIs and FIIs have simultaneously shored up holdings or cut their stake over the past four quarters.

Meanwhile, there are eight companies where the two have taken a sharply divergent view—where one set has increased stake consistently, the other has simultaneously pared down ownership. To clear the situation, we delve deeper and find out how analysts are placed on each of these stocks where the big investors have taken a contrasting stand.

Known - Unknown Framework

SECTOR SPECIFIC VS STOCK SPECIFIC

Buy pharma as a bucket, be stock-specific

in auto: Sudip Bandyopadhyay, Inditrade Capital

ET Now|Updated: Sep 09, 2018, 10.28

What is your assessment of the pharma pack as a whole? Could factors

like the currency and improvement in US business prove to be tailwinds for the

sector as a whole?

Absolutely. We have been positive for some time on the pharma sector

and this is one sector where investors should start moving money definitely.

There are always some uncertainties with pharma companies because of the

regulatory action and the consequences thereof, like we have seen in Sun Pharma

today. But our strategy has been very clearly to buy a basket of pharma

companies so that you avoid the vagaries of individual company related

regulatory action. We have been recommending a basket buy in pharma which

includes Sun, Aurobindo, Natco Pharma, Cadila and Torrent Pharma. For an

investor in a volatile market with depreciating currency, pharma definitely is

a good bet. It has not performed as a sector for quite some time. The valuation

looks attractive. As you rightly pointed out US business is improving and to a

great extent the regulatory action is also behind the industry. Most of the

companies have tried to get their act together. Yes, there may be sporadic

action here and there from US FDA but by and large things have improved

significantly from what it was couple of years back.

How are you looking at the auto space? We have been bullish on auto.

We have been particularly bullish on the commercial vehicle segment and

Ashok Leyland is one company on which we

have been recommending a buy. The commercial vehicle cycle has clearly turned

and that ensures that companies like Ashok Leyland continues to outperform the

expectations. It happened in the first quarter of the current fiscal. They came

up with excellent results. Post that. there was a bit of a correction in prices

due to that government changing the axle load factor but that was a temporary

blip. The larger issue is the vehicle scrappage policy which is being

circulated and which is being talked about. It is a matter of time before the

vehicle scrappage policy comes and that policy is going to help companies like

Ashok Leyland in a big way. We have to keep that in mind. You talked about

environment-friendly vehicles and electric vehicles. Ashok Leyland in the

commercial vehicle space is working on that and they have the capacity to

deliver electronic vehicles as well and that is excellent. Also, they have

started getting a lot of export orders including in double-decker buses where

they have the skill sets. The valuation after correction looks attractive and

we definitely recommend a buy there. In the two-wheeler space, Hero MotoCorp is

definitely a stand out with the rural market getting a lot of attention as this

is an election year. Farm income is expected to increase significantly with

good monsoon. Hero with its outstanding reach in the rural market should

benefit and they should be the outperformers amongst the two-wheeler companies.

There has been some announcements in Bajaj regarding their capacity to deliver

electrical three-wheelers and for that they will not require any licenses. They

are expecting large sales and they have got the export market working for them.

It is a good company to buy into but between the two-wheeler companies, we will

go for Hero MotoCorp.

Nifty & Sensex VS Mid-cap and Small-cap Index - Both to be considered for making any analysis

Sensex not the real picture, India's growth story scripted by small entrepreneurs - to be gauged from mid-cap and small-cap index

As this paper recently argued, the mid-cap- and small-cap indices — the barometer of the real economy — have dived in the past six months, signalling that all's not well with India Inc.

After ET front-paged the article (Is This An Uneasy Lull Before The Crash, Aug 6) that showed theSensexholding at fairly high levels despite the crash in mid- and small-caps, the markets have lost some of their steam. After all, this had to happen because the Sensex — comprising of only 30stocks— is in many ways not a clear indicator of the India Story.

REAL INDIA STORY

The real India Story is being scripted by small entrepreneurs, not the big boys. The big boys anyway have the wherewithal to ride out economic turbulence. It's the small entrepreneurs who are being squeezed dry by the rising cost of funds and plunging order books.

It's the small companies which are becoming uncompetitive because of erratic power supply, dismal infrastructure and rampant corruption. The big boys can take it on the chin and move on, but it's the small companies that are getting hit badly by these bouncers the dismal economy is throwing at a ferocious pace."The environment is not conducive for startups. The odds against a small manufacturer are very high," said Anil Bhardwaj, the secretary-general of the Federation of Indian Micro & Medium Enterprises (FISME). The contrasting fortunes of India's big and small companies are best reflected in stock market data. Policymakers in Delhi gloat over the fact that the market hasn't tanked despite GDP growth slowing down from 9% to 6.5%, and almost 5% now.

The firmness in the market is being seen, perhaps wrongly, as a proof of investor confidence in the India Story, and a steady Dalal Street is being flogged as a sign that global funds think India's troubles are temporary.

This faulty theory has lost some sheen in recent times since it solely focuses on the share-price performance of the 30 big companies that comprise the BSE Sensex, and conveniently ignores the larger market . The same largely can be said of the Nifty 50, where top blue chips determine the perception of the broader economy.

In the past 12 months, the Sensex companies generated a 7.45% return while the BSE mid-cap- and small-cap indices lost more than 10% and 19%, respectively. And from January 1 this year, the Sensex has fallen by just 2.5%, but the mid-cap- and small-cap indices have taken a battering of 23% and 28%, respectively. Contrary to the perception that the markets have held firm, there has actually been mayhem in the markets.

Rajesh Mascarenhas & Javed Sayed, ET Bureau | 13 Aug, 2013

Industry

Company Name

AUTOMOBILE

Bajaj Auto Ltd.

Bosch Ltd.

Hero MotoCorp Ltd.

Mahindra & Mahindra Ltd.

Maruti Suzuki India Ltd.

Tata Motors Ltd.

CEMENT & CEMENT PRODUCTS

ACC Ltd.

Ambuja Cements Ltd.

Grasim Industries Ltd.

UltraTech Cement Ltd.

CONSTRUCTION

Larsen & Toubro Ltd.

CONSUMER GOODS

Asian Paints Ltd.

Hindustan Unilever Ltd.

I T C Ltd.

ENERGY

Bharat Petroleum Corporation Ltd.

Cairn India Ltd.

GAIL (India) Ltd.

NTPC Ltd.

Oil & Natural Gas Corporation Ltd.

Power Grid Corporation of India Ltd.

Reliance Industries Ltd.

Tata Power Co. Ltd.

FINANCIAL SERVICES

Axis Bank Ltd.

Bank of Baroda

HDFC Bank Ltd.

Housing Development Finance Corporation

ICICI Bank Ltd.

IndusInd Bank Ltd.

Kotak Mahindra Bank Ltd.

Punjab National Bank

State Bank of India

Yes Bank Ltd.

INDUSTRIAL MANUFACTURING

Bharat Heavy Electricals Ltd.

IT

HCL Technologies Ltd.

Infosys Ltd.

Tata Consultancy Services Ltd.

Tech Mahindra Ltd.

Wipro Ltd.

MEDIA & ENTERTAINMENT

Zee Entertainment Enterprises Ltd.

METALS

Coal India Ltd.

Hindalco Industries Ltd.

Tata Steel Ltd.

Vedanta Ltd.

PHARMA

Cipla Ltd.

Dr. Reddy's Laboratories Ltd.

Lupin Ltd.

Sun Pharmaceutical Industries Ltd.

SERVICES

Adani Ports and Special Economic Zone Ltd.

TELECOM

Bharti Airtel Ltd.

Idea Cellular Ltd.

Stock Market Anecdotes

Irrational Markets

while the irrationality of markets offers opportunities, just remember

John Maynard Keynes “the market can stay irrational longer than you can stay solvent.”

How long an Event will impact Market

Monkey Story on Stock Markets

Once Upon A Time In A Village, A Man Appeared And Announced To The Villagers That He Would Buy Monkeys For $10/-

The Villagers Seeing That There Were Many Monkeys Around, Went Out To The Forest And Started Catching Them. The Man Bought Thousands At $10/- And As Supply Started To Diminish, The Villagers Stopped Their Effort. He Further Announced That He Would Now Buy At $20/- This Renewed The Efforts Of The Villagers And They Started Catching Monkeys Again.

Soon The Supply Diminished Even Further And People Started Going Back To Their Farms. The Offer Rate Increased To $25/- And The Supply Of Monkeys Became So Little That It Was An Effort To Even See A Monkey, Let Alone Catch It! The Man Now Announced That He Would Buy Monkeys At $50! However, Since He Had To Go To The City On Some Business, His Assistant Would Now Buy On Behalf Of Him.

In The Absence Of The Man, The Assistant Told The Villagers. Look At All These Monkeys In The Big Cage That The Man Has Collected. I Will Sell Them To You At $35 And When The Man Returns From The City, You Can Sell It To Him For $50/-

The Villagers Squeezed Up With All Their Savings And Bought All The Monkeys.

Then They Never Saw The Man Nor His Assistant, Only Monkeys Everywhere!! !

Welcome To The 'Stock' Market!!!!!

Ashutosh Joshi/The Wall Street Journal

The Grandmother With Faith in Indian Stocks

Ashalata Maheshwari, right, at her residence in Mumbai.

At a time when individuals in India are disenchanted with the stock market, Mumbai resident Ashalata Maheshwari, 77 years old, is a rare champion for stocks.

Ms. Maheshwari has been investing in Indian companies for five decades, and though many have gone bust over the years, shares in others have gained enough value to give her confidence that equities are the best investments over the long term.

“Stocks have given me the best returns because I have rarely sold them,” Ms. Maheshwari told The Wall Street Journal in an interview at her Mumbai home. “Patience is key to stock market investments,” she said.

The Reserve Bank of India says stocks comprise less than 5% of the savings of Indian households, which have traditionally invested in gold and real estate.

Many individuals turned to the stock market for the first time between 2007 and 2009 when India was booming and people had plenty of disposable income. But the financial downturn has hurt. India’s benchmark BSE S&P Sensex is off about 9% from record levels seen in early 2008.

Ms. Maheshwari is unfazed because stocks have risen over the long term. In the last 20 years, the BSE S&P Sensex has gained 11.4% on average annually. The gains are much higher if dividend income and bonus shares are taken into account. Over the same period, the value of gold has risen about 10% a year.

Ms. Maheshwari says her portfolio of 1,500 stocks is worth around 40 million rupees ($660,000). She says she owns most of the stocks for the dividends they pay, and plans to hold on to them for years.

Ms. Maheshwari says she is a hands-on investor who wades through companies’ financial statements. She has become a regular fixture at the annual general meetings of India’s largest firms, such as Reliance Industries Ltd. and Tata group companies, where she often asks for higher dividends and updates on planned projects.

To get her message across at these meetings, Ms. Maheshwari has occasionally burst into poem or song about a chief executive or directors. This has left a mark on many.

“[She] has been among those shareholders of Tata companies who, though individuals, are an institution,” Ratan Tata, the former chairman of the Tata group told The Wall Street Journal. “For as long as I can remember, she would be the most vocal lady shareholder-speaker in a bastion of men at AGMs. I believe she has inspired many women and youngsters to become engaged investors,” Mr. Tata said.

At Reliance Industry’s annual meeting in June, Ms. Maheshwari had a question for chief executive Mukesh Ambani, who earlier this year got Z-level security, the second-highest level of security in India.

Standing before an audience of around 1,000 Reliance shareholders and executives, Ms. Maheshwari said that if Mr. Ambani got “Z” security, shareholders should at least get “ABCD,” with A representing appreciation, B for bonus, C for cash, and D for dividends.

A Reliance spokesman said in June that Ms. Maheshwari’s and other investors’ demands were pending with the board. He didn’t respond to a recent call for comment. For last fiscal year, Reliance Industries paid a dividend of nine rupees a share.

Ms. Maheshwari says Reliance Industries is one of the best performing stocks in her portfolio, along with Tata Motors Ltd., software firm Tata Consultancy Ltd., engineering firm Larsen & Toubro Ltd. and toothpaste maker Colgate-Palmolive (India) Ltd. She says these stocks have risen by 10 times to 25 times since she bought them.

She says returns on stocks helped her to buy her home in Santacruz, a posh Mumbai neighborhood, for 80,000 rupees in 1972. “Today this house should be worth 50 million to 60 million rupees,” she said.

Ms. Maheshwari, a high school graduate, was introduced to stocks when she was 21. Her father-in-law gave her 1,000 shares of Grasim Industries Ltd., then a textile company, as a wedding gift in 1954.

“That time I didn’t even know what these pieces of paper meant,” she said, referring to the stock certificates.

Ms. Maheshwari says she realized their value after she started getting dividend checks regularly. “I decided to put more of my savings into stocks and made it a habit,” she said.

Over the years, her husband J.P. Maheshwari, who used to run a plastic products manufacturing business, started helping her.

Now, the two of them spend their days monitoring financial TV channels to get news on companies, stock markets and the economy, regularly trading on a pool of 100 to 200 stocks in Ms. Maheshwari’s portfolio.

She says she doesn’t always believe in analyst commentary and instead studies companies’ financial statements, annual reports, and dividend and bonus history before deciding on whether to invest in a stock or not.

“Balance sheets will always reveal the truth,” she said.

Ms. Maheshwari plans to be an active shareholder for many more years, and rues that there aren’t enough investors asking companies tough questions, especially at shareholder meetings.

“Investors should come prepared and throw valid questions to company managements… I don’t see that happening,” she said.

Seemingly Simple Strategy of "Buy and Hold a blue chip forever" is also risky.

Why holding a blue chip stock forever a very risky investing strategy

There are people who are keen to over simplify equity investing. Buy blue chips and hold on to them forever, they would say. As long as you have bought a good stock, you don't have to worry — you will get a great return. Such advice is a huge dis-service to keen new investors. Much as we love to hear it, there is no sure-fire way to make money in stocks. Think about it: if the return is higher than all other choices, how can it be easy? To assume that you can buy and hold and be rewarded for sheer laziness is preposterous.

I will take you back to 1985, the first stock market boom that I watched. The market leader was Century Mills. It was the largest single-unit textile mill in the country, located in the heart of the mill district of Parel-Worli in Mumbai. Set up in 1897 and run by the Birla family, it was the darling of the markets. Then there was Gujarat Narmada Valley Fertilisers. A revolutionary company that roped in farmers as shareholders to completely modify how fertilisers were made and sold. Scindia Shipping, with its debt and cyclical revenue was also a blue-chip. There were respectful references to Mukund Iron from the Bajaj family, for being an efficient steel maker. The 1980s belonged to the Indian companies that made it big in manufacturing.

Of the 30 bluest of blue chips included in the BSE Sensitive Index which was constructed in 1984 (back calculated to 1980) only seven remain today. Century mills stopped manufacturing in 2006 and the land is now being redeveloped commercially. GSFC, Scindia and 23 other blue chips of those days are significantly bruised or have closed shop.

An investor who bought these blue chips in 1980 held on to them for 35 long years will find that he is now left with a few duds. The biggest problem in equity investing is the hindsight bias. We all like to think that somehow we would have foreseen the decline of these companies and gotten out of them at the right time, and moved on to the new blue chips.

The truth is that we would have been clueless. Either we would have failed to see that our stocks are declining, given their illustrious past. Or we would be wary of the new claimants to the blue chip title and unwilling to buy them. It is a fallacy that we would have remained on top of the league by design.

I always dismiss the success stories about buying few stocks and making a pile on it, as luck. It is a piece of irrelevant and useless information to a new investor, when his uncle tells him how he bought the shares of Colgate at Rs 11 and is earning a fat dividend, or how his investment in Reliance Industries has paid for itself over the years. What matters is a replicable strategy.

Since no one has seen the future, even the best stock picking strategy can go wrong. It can only be a matter of chance that something picked up and held for years still remains good.

Then how is it that people talk of returns of 16-17 per cent per annum on equity? How do they use the Sensex to show how it has grown over a period of time, to deliver fantastic returns?

Two key differences here. One, Sensex is not a stock, it is a portfolio. Two, Sensex components have been consistently revised. When you do not stop at simply picking a stock, but picking many stocks to make a portfolio, you build in the benefit of diversification.

A portfolio is the first cushion for wrong selection. And then, you build in a discipline for revision. You admit that you could have gone wrong, or you accept that circumstances may change to make your today's blue chip tomorrow's dud. You therefore put in place the rules for throwing out what is not working and replacing it with what is working.

That is how the index revision committees work. When they hear about a scandal, as in case of Satyam, they throw it out of the index. When they find the new technology, telecom and banking stocks growing big in size and posting consistent profits, they replace them for the steel, auto, and shipping stocks in the index. So the idea of passively buying something and holding on it to for life, is actually a very risky investing strategy.

It is not a sure-fire way to equity riches, since the real process is one where you have to make decisions about what goes out and what comes in, and allow for errors while you do all that.

Should one invest in blue chips at all? Yes, the core portfolio of an investor should be made up of solid profit-making companies that are market leaders. This buffers the decisions you may make with new and unknown stocks. Such a portfolio of blue chips, also enables you to capture the equity returns over a long term. Buy the index itself (ETFs and index funds are the cheapest routes to buying blue chip equity portfolios) or trust diversified large cap equity funds to do the job for you (every fund house has this product). When you do so, allow yourself to appreciate that someone else is modifying the large cap portfolio to a discipline or a process, on your behalf. Money is not being made by simply sitting around.

If you do insist that you will build your own equity portfolio, blue chips is a good place to begin. However, be sure that the criterion for including them in your portfolio are written down like golden rules. When a stock in your portfolio slips, you have to make a decision. You can get one or both ends of the decision wrong — the stock you sold could get better, and the stock you bought could become worse. But those are the risks in equity investing, and you have to be sure that you enjoy the journey of analysis, observation, harsh lessons of failure, and fun moments of magic.

The next time you hear someone tell you his old story of a multi-bagger, unless it was a company he promoted and built with his own hands, it might be a good idea to simply snigger.

By Uma Shashikant (The author is Managing Director, Centre for Investment Education and Learning)

9 Feb, 2015 Economic Times

Model of surviving on dividends and sticking to Blue Chips Vs Pitfalls in Buy and Hold forever strategy

Stocks that have fallen down and not recovered while market has fallen and recovered between 2008 and 2013

Warren Buffett

Warren E. Buffett first took control of Berkshire Hathaway Inc., a small textile company, in April of 1965. A share was quoting at around $18 at that time. Forty-eight years later, the same share traded for $134,060, compounding investor capital at just under 21% per year -- a multiplier of 7,448 times

Warren Buffett annual letter : The latest one to include a section on investing advice

Berkshire Hathaway Inc. investors will be looking for details of how the conglomerate performed and the best advice chief executive Warren Buffett, a prominent American businessman, has to offer in his annual letter this Saturday.

Investors follow Berkshire because of Buffett's remarkable investing track record and because the conglomerate's results offer a glimpse into a variety of industries

. Buffett's letter is always well-read because of his track record, but this year he released a section focused on investing advice early so there may not be many surprises.

Warren Buffett seeks out a firm's intrinsic value and waits for the market to adjust accordingly over time, George Soros relies on short-term volatility and highly leveraged transactions

In the short run, investment success can be accomplished in a myriad of ways. Speculators and day traders often deliver extraordinary high rates of return, sometimes within a few hours. Generating a superior rate of return consistently over a further time horizon, however, requires a masterful understanding of the market mechanisms and a definitive investment strategy. Two such market players fit the bill: Warren Buffett and George Soros.

Warren Buffett Known as "the Oracle of Omaha," Warren Buffett made his first investment at the tender age of 11. In his early 20s, the young prodigy would study at Columbia University, under the father of value investing and his personal mentor, Benjamin Graham. Graham argued that every security had an intrinsic value that was independent of its market price, instilling in Buffett the knowledge with which he would build his conglomerate empire. Shortly after graduating he formed "Buffett Partnership" and never looked back. Over time, the firm evolved into "Berkshire Hathaway," with a market capitalization over $200 billion. Each stock share is valued at near $130,000, as Buffett refuses to perform a stock split on his company's ownership shares.

Warren Buffett is a value investor. He is constantly on the lookout for investment opportunities where he can exploit price imbalances over an extended time horizon.

Buffett is an arbitrageur who is known to instruct his followers to "be fearful when others are greedy, and be greedy when others are fearful." Much of his success can be attributed to Graham's three cardinal rules: invest with a margin of safety, profit from volatility and know yourself. As such, Warren Buffett has the ability to suppress his emotion and execute these rules in the face of economic fluctuations.

George Soros Another 21st century financial titan, George Soros was born in Budapest in 1930, fleeing the country after WWII to escape communism. Fittingly, Soros subscribes to the concept of "reflexivity" social theory, adopting a "a set of ideas that seeks to explain how a feedback mechanism can skew how participants in a market value assets on that market."

Graduating from the London School of Economics some years later, Soros would go on to create the Quantum Fund. Managing this fund from 1973 to 2011, Soros returned roughly 20% to investors annually. The Quantum Fund decided to shut down based on "new financial regulations requiring hedge funds to register with the Securities and Exchange Commission." Soros continues to take an active role in the administration of Soros Fund Management, another hedge fund he founded.

Where Buffett seeks out a firm's intrinsic value and waits for the market to adjust accordingly over time, Soros relies on short-term volatility and highly leveraged transactions. In short, Soros is a speculator. The fundamentals of a prospective investment, while important at times, play a minor role in his decision-making.

In fact, in the early 1990s, Soros made a multi-billion dollar bet that the British pound would significantly depreciate in value over the course of a single day of trading. In essence, he was directly battling the British central banking system in its attempt to keep the pound artificially competitive in foreign exchange markets. Soros, of course, made a tidy $1 billion off the deal. As a result, we know him today as the man "who broke the bank of England."The Bottom Line Warren Buffett and George Soros are contemporary examples of the some of the most brilliant minds in the history of investing. While they employ markedly different investing strategies, both men have achieved great success. Investors can learn much from even a basic understanding of their investment strategies and techniques.

Bill Gross: I’m not a great investor and Warren Buffett, George Soros may not be either

Warren Buffett was in market at the right.He used simple principles.If his track was extra-ordnianry it has to do with the time he entered than his skills.Perhaps it was the epoch that made the man as opposed to the man that made the epoch

“Am I a great investor? No, not yet.”So writes Bill Gross, manager of the world’s largest mutual fund, in his latest investment outlook.

Gross also said the most renowned investors from Warren Buffett to George Soros may owe their reputations to a favorable era for money management as expanding credit fueled gains in asset prices across markets.

The real test of greatness for investors is not how they navigated market cycles during that time, but whether they can adapt to historical changes occurring over half a century or longer, Gross, 67, wrote in the outlook entitled “A Man in the Mirror,” which is the name of a song by Michael Jackson.

Buffett, Soros, Fuss, yeah – me too, have cut our teeth during perhaps a most advantageous period of time . . . an investor could experience

“All of us, even the old guys like Buffett, Soros, Fuss, yeah – me too, have cut our teeth during perhaps a most advantageous period of time, the most attractive epoch, that an investor could experience,” Gross wrote. “Perhaps it was the epoch that made the man as opposed to the man that made the epoch.”

Gross, one of the co-founders in 1971 of Pacific Investment Management Co (PIMCO), is often referred to in the media as “the bond king.” He runs the US$289-billion Pimco Total Return Fund, which has advanced 7.9% over the past five years to beat 94% of peers.

Gross is examining his legacy as the bond shop he built over four decades is seeking to adapt to an environment that looks very different from the bull market that fueled Pimco’s growth to one of the largest money managers in the world. The prospect of elevated market volatility, an aging population and climate change could make investing far more challenging in the coming decades, Gross said.

‘New Normal’

Pimco in 2009 started an expansion into equities to prepare for an eventual end of the decades-long bond rally. Gross, whose firm coined the term “new normal” that year to describe an economic environment characterized by below-average growth, elevated unemployment and a declining role for the U.S. in the global economy, suggested those changes could potentially be part of a longer-lasting shift.

“What if zero-bound interest rates define the end of a total return epoch that began in the 1970s, accelerated in 1981 and has come to a mathematical dead-end for bonds in 2012/2013 and commonsensically for other conjoined asset classes as well?” Gross wrote. “What if quantitative easing policies eventually collapse instead of elevate asset prices?”

Soros is the legendary hedge-fund manager best known for a 1992 bet that the Bank of England would be forced to devalue the pound. Buffett is the chief executive officer of Berkshire Hathaway Inc. who built the firm over almost five decades through takeovers and prescient stock picks, and Daniel Fuss is a bond manager who runs the top-performing Loomis Sayles Bond Fund.

‘Achilles Heel’

Gross said investors such as Bill Miller, the stock picker who beat the Standard & Poor’s 500 Index for a record 15 years before his streak ended in 2005, are prone to exposing their “Achilles heel” the longer they stay in the money-management business. Miller may, in fact, be a great investor, although he would need five or six more years on top to prove it, Gross said. Peter Lynch, the Fidelity Investments manager who ran the Magellan fund, made a smart move by leaving when the “gettin’ was good,” according to Gross. Lynch earned the highest returns in the industry from 1977 to 1990, averaging annual gains of 29% before stepping down.

“There is not a Bond King or a Stock King or an Investor Sovereign alive that can claim title to a throne,” Gross said.

The Equity Cult is dead PIMCO Bill Gross and the Counter argument: Long Live Equities The cult of equity is dying. Like a once bright green aspen turning to subtle shades of yellow then red in the Colorado fall, investors' impressions of "stocks for the long run" or any run have mellowed as well. I "tweeted" last month that the souring attitude might be a generational thing: "Boomers can't take risk. Gen X and Y believe in Facebook but not its stock. Gen Z has no money." True enough, but my tweetering 95-character message still didn't answer the question as to where the love or the aspen-like green went, and why it seemed to disappear so quickly. Several generations were weaned and in fact grew wealthier believing that pieces of paper representing "shares" of future profits were something more than a conditional IOU that came with risk. Hadn't history confirmed it? Jeremy Siegel's rather ill-timed book affirming the equity cult, published in the late 1990s, allowed for brief cyclical bear markets, but showered scorn on any heretic willing to question the inevitability of a decade-long period of upside stock market performance compared to the alternatives. Now in 2012, however, an investor can periodically compare the return of stocks for the past 10, 20 and 30 years, and find that long-term Treasury bonds have been the higher returning and obviously "safer" investment than a diversified portfolio of equities. In turn it would show that higher risk is usually, but notalways, rewarded with excess return.Got Stocks? Chart 1 displays a rather different storyline, one which overwhelmingly favors stocks over a century's time – truly the long run. This long-term history of inflation adjusted returns from stocks shows a persistent but recently fading 6.6% real return (known as the Siegel constant) since 1912 that Generations X and Y perhaps should study more closely. Had they been alive in 1912 and lived to the ripe old age of 100, they would have turned what on the graph appears to be a $1 investment into more than $500 (inflation adjusted) over the interim. No wonder today's Boomers became Siegel disciples. Letting money do the hard work instead of working hard for the money was an historical inevitability it seemed.

Yet the 6.6% real return belied a commonsensical flaw much like that of a chain letter or yes – a Ponzi scheme.If wealth or real GDP was only being created at an annual rate of 3.5% over the same period of time, then somehow stockholders must be skimming 3% off the top each and every year. If an economy's GDP could only provide 3.5% more goods and services per year, then how could one segment (stockholders) so consistently profit at the expense of the others (lenders, laborers and government)?The commonsensical "illogic" of such an arrangement when carried forward another century to 2112 seems obvious as well. If stocks continue to appreciate at a 3% higher rate than the economy itself, then stockholders will command not only a disproportionate share of wealth but nearly all of the money in the world! Owners of "shares" using the rather simple "rule of 72" would double their advantage every 24 years and in another century's time would have 16 times as much as the sceptics who decided to skip class and play hooky from the stock market.

Cult followers, despite this logic, still have the argument of history on their side and it deserves an explanation. Has the past 100-year experience shown in Chart 1 really been comparable to a chain letter which eventually exhausts its momentum due to a lack of willing players? In part, but not entirely.Common sense would argue that appropriately priced stocks should return more than bonds. Their dividends are variable, their cash flows less certain and therefore an equity risk premium should exist which compensates stockholders for their junior position in the capital structure. Companies typically borrow money at less than their return on equity and therefore compound their return at the expense of lenders. If GDP and wealth grew at 3.5% per year then it seems only reasonable that the bondholder should have gotten a little bit less and the stockholder something more than that. Long-term historical returns for Treasury bill and government/corporate bondholders validate that logic, and it seems sensible to assume that same relationship for the next 100 years. "Stocks for thereallylong run" would have been a better Siegel book title.

Yet despite the past 30-year history of stock and bond returns that belie thereallylong term, it is not the future win/place perfecta order of finish that I quarrel with, but its 6.6% "constant" real return assumption and the huge historical advantage that stocks presumably command. Chart 2 points out one of the additional reasons why equities have done so well compared to GNP/wealth creation. Economists will confirm that not only the return differentials within capital itself (bonds versus stocks to keep it simple) but the division of GDP between capital, labor and government can significantly advantage one sector versus the other. Chart 2 confirms that real wage gains for labor have been declining as a percentage of GDP since the early 1970s, a 40-year stretch which has yielded the majority of the past century's real return advantage to stocks. Labor gaveth, capital tooketh away in part due to the significant shift to globalization and the utilization of cheaper emerging market labor. In addition, government has conceded a piece of their GDP share via lower taxes over the same time period. Corporate tax rates are now at 30-year lows as a percentage of GDP and it is therefore not too surprising that those 6.6% historical real returns were 3% higher than actual wealth creation for such a long period.

The legitimate question that market analysts, government forecasters and pension consultants should answer is how that 6.6% real return can possibly be duplicated in the future given today's initial conditions which historically have never been more favorable for corporate profits.If labor and indeed government must demand some recompense for the four decade's long downward tilting teeter-totter of wealth creation, and if GDP growth itself is slowing significantly due to deleveraging in a New Normal economy, then how can stocks appreciate at 6.6% real? They cannot, absent a productivity miracle that resembles Apple's wizardry.

Got Bonds?

My ultimate destination in thisInvestment Outlooklies a few paragraphs ahead so let me lay its foundation by dissing and dismissing the past 30 years' experience of the bond market as well.With long Treasuries currently yielding 2.55%, it is even more of a stretch to assume that long-term bonds – and the bond market – will replicate the performance of decades past.The Barclay's U.S. Aggregate Bond Index – a composite of investment grade bonds and mortgages – today yields only 1.8% with an average maturity of 6–7 years. Capital gains legitimately emanate from singular starting points of 14½%, as in 1981, not the current level in 2012. What you see is what you get more often than not in the bond market, so momentum-following investors are bound to be disappointed if they look to the bond market's past 30-year history for future salvation, instead of mere survival at the current level of interest rates.

Together then, a presumed 2% return for bonds and an historically low percentagenominalreturn for stocks – call it 4%, when combined in a diversified portfolio produce anominalreturn of 3% and an expected inflation adjusted return nearzero.The Siegel constant of 6.6% realappreciation, therefore, is an historical freak, a mutation likely never to be seen again as far as we mortals are concerned.The simple point though whether approached in realornominal space is that U.S. and global economies will undergo substantial change if they mistakenly expect asset price appreciation to do the heavy lifting over the next few decades. Private pension funds, government budgets and household savings balances have in many cases been predicated and justified on the basis of 7–8% minimum asset appreciation annually. One of the country's largest state pension funds for instance recently assumed that its diversified portfolio would appreciate at a real rate of 4.75%. Assuming a goodly portion of that is in bonds yielding at 1–2% real, then stocks must do some very heavy lifting at 7–8% after adjusting for inflation. That is unlikely. If/when that does not happen, then the economy's wheels start spinning like a two-wheel-drive sedan on a sandy beach. Instead of thrusting forward, spending patterns flatline or reverse; instead of thriving, a growing number of households and corporations experience a haircut of wealth and/or default; instead of returning to old norms, economies begin to resemble the lost decades of Japan.

Some of the adjustments are already occurring. Recent elections in San Jose and San Diego, California, have mandated haircuts to pensions for government employees. Wisconsin's failed gubernational recall validated the same sentiment. Voided private pensions of auto and auto parts suppliers following Lehman 2008 may be a forerunner as well for private corporations.The commonsensical conclusion is clear: If financial assets no longer work for you at a rate far and above the rate of true wealth creation, then you must work longer for your money, suffer a haircut on your existing holdings and entitlements, or both. There are still tricks to be played and gimmicks to be employed. For example – the accounting legislation just passed into law by the Congress and signed by the President allows corporations to discount liabilities at an average yield for the past 25 years! But accounting acts of magic aside, this and other developed countries have for too long made promises they can't keep, especially if asset markets fail to respond as they have historically.

Reflating to Prosperity

The primary magic potion that policymakers have always applied in such a predicament is to inflate their way out of the corner. The easiest way to produce 7–8% yields for bonds over the next 30 years is to inflate them as quickly as possible to 7–8%! Woe to the holder of long-term bonds in the process! Similarly for stocks because they fare poorly as well in inflationary periods. Yet if profits can be reflated to 5–10% annual growth rates, if the U.S. economy can grow nominally at 6–7% as it did in the 70s and 80s, then America's and indeed the global economy's liabilities can be "reflated" away. The problem with all of that of course is that inflation doesn't create real wealth and it doesn't fairly distribute its pain and benefits to labor/government/or corporate interests.Unfair though it may be, an investor should continue to expect an attempted inflationary solution in almost all developed economies over the next few years and even decades.Financial repression, QEs of all sorts and sizes, and even negative nominal interest rates now experienced in Switzerland and five other Euroland countries may dominate the timescape. The cult of equity may be dying, but the cult of inflation may only have just begun.

William H. Gross

Managing Director

The counter Argument

DEAR PIMCO: Would Bill Gross Maybe Like To Update His Analysis Of Stocks?

Even brilliant people occasionally make boneheaded mistakes, and one of the world's most prominent investors appears to have made a big one.

Yesterday,Bill Gross, the bond king at bond giantPIMCO,published an analysis of of the stock market that instantly grabbed everyone's attention.

Arguing that the "cult of equities" is dying or dead (true--and, ironically, a bullish observation), Gross went on to ridicule the idea that stocks will have the same long-term returns in the future as they have had in the past--for one simple reason:

If stocks appreciate at ~7% a year forever, while GDP only grows at ~3%, the stock market will soon be worth more than the entire world.

At first blush, this seems like an obvious but profound observation, one that would make every equity strategist, scholar, and financial advisor who has ever cited the ~7% long-term stock return (after adjusting for inflation) look and feel like a moron.

Alas, it's wrong.

And after chewing through the analysis, in fact, most observers came away thinking that Bill Gross should probably stick to bonds.

Why is Gross wrong?

Because stocks actually havenot"appreciated" at ~7% a year.

Stocks havereturned~7% a year.

Why is this distinction important? Because there is a big difference between "appreciate" and "return." And Bill Gross, importantly, used the word "appreciate":

If stocks continue toappreciateat a 3% higher rate than the economy itself, then stockholders will command not only a disproportionate share of wealth but nearly all of the money in the world! Owners of "shares" using the rather simple "rule of 72" would double their advantage every 24 years and in another century's time would have 16 times as much as the sceptics who decided to skip class and play hooky from the stock market.

Again, stocks have not, in fact, "appreciated" at ~7% per year for the past couple hundred years. Stocks have only "appreciated" about 2% per year.

That is to say, the prices of stocks, after adjusting for inflation, have only risen about 2% per year for the past couple of centuries.

So where has the rest of the return come from?

Dividends.

Over the past century, about 4 points of the ~7% annual return of stocks has come from dividends.

Companies have paid out cash to their shareholders, and these shareholders have either used the cash to buy more shares (from someone else--not usually from the company) or used the cash to buy other stuff. Either way, the dividend part of the stock "return" is then recycled back into the economy.

This is a very fundamental mistake. And for an investor with Gross's stature, responsibilities, and following, it's highly embarrassing. Here's hoping he acknowledges and corrects it.

Addendum:By the way, Bill Gross is probably absolutely right that stocks will return less in the future than they have in the past, but not for the reason he suggests. The reason stocks will likely return less in the future is that 1) stocks are still overvalued relative to historical averages, 2) dividends are much lower than historical averages, and 3) profit margins are much higher than average, suggesting that they will soon drop. All of these factors suggest that equities will return about ~2%-3% real over the next decade instead of the ~7% average. But this has nothing to do with the flawed idea that stocks can't return more than GDP.

Bill Gross also makes another very important point about how corporations and shareholders have become greedy in recent years and now pay an all-time-low percent of GDP as wages. This is a big problem, one that will have to change if the economy is to heal itself. I've discussed this issue frequently: As companies pay employees more, margins will drop, which will hurt stock performance (see point 3 above). But, again, this has nothing to do with the claim that stocks can't return more than GDP.

ByHenry Blodget|Daily Ticker – Wed, Aug 1, 2012

East India company shares crash on London stock Exchange on news of attack by Hyder Ali, Sultan of Mysore For almost ten years following Plassey, East India Company shares had become the focus of intense international speculative activity, pumped up by successive announcements of ever-grander acquisitions in the East.

Between February 1758 when news of the victory at Plassey reached London and December 1768, when the Company bought the land for the Bengal Warehouse, the Company’s shares had doubled to stand at £276. But this was to bethe peak of the boom.

Five months later, in May 1769, news reached London that not only had a French fleet entered the Indian Ocean, but that Hyder Ali, Sultan of Mysore, had invaded the Company’s possessions in south India. The share price fell 16 per cent in a single month, and would continue a downward course for the next 15 years, reaching the depths of £122 in July 1784, a fall of 55 percent.

Eventhough East India company emerged stronger after Hyder Ali attack, the fall triggered by it could not be reversed for next 40 years until 1824.

MULTI BAGEERS

For years, these two Lucknowmen burnt their fingers in the stock market: they picked wrong companies in their desperate hunt for multibagger returns, and the ones on which they got it right, they sold out too early!

Today, the Mittal brothers laugh when they talk about that phase; they look at it as learning. Over time, they have grown as investors and made far more money than what they lost back then.

Ayush Mittal is just 33 and his brotherPratyush Mittal, 29. Over the past decade or so, they have developed a flair for spotting potential value bets among smaller companies and made big money on them.

Their father SP Mittal, now 60, has been a full-time stock investor since 1980s.

Based in Lucknow, a hot bed for Mughlai cuisine consisting of dishes developed in Medieval India at the centre of the Mughal Empire, the Mittal brothers picked sea food manufacturing company Avanti Feeds in 2011 at Rs 7 (adjusted price). Today, that stock trades at Rs 1,700, indicating a 24,185 per cent rise in just six years. And it is still part of their portfolio. Mittals believe collaborative research can guarantee extraordinary returns in the stock market. Anyone with investing discipline and hard work can generate good returns on Dalal Street, they claim.

The two have since created a tool, named www.screener.in, for investors to do their own research before betting on a stock.

Their father S P Mittal himself made it big in his heydays: picking Cipla in 1985 and DLF in the 1990s. He sold DLF in 2007 after its listing on BSE but still holds Cipla in his portfolio.

Ayush and Pratyush are CA by qualification. They have been investing in stocks since their early 20s.

They invested in Astral Poly at about Rs 25 in 2011 and exited it a few months back at about Rs 425. Today, the stock trades at over Rs 600. The company is a leader in CPVC plumbing pipes and has been a big beneficiary of the switch from GI pipes to CPVC pipes.

ETMarkets.com could not independently verify Mittal brothers' holdings at present or back then.

Investment strategy

Mittal brothers say they prefer midcap and smallcap companies. They burn midnight oil, trying to identify stocks that can grow at above-normal pace and multiply wealth over time. Usually, such names are not very popular, they claim. investors looking for quality business, fundamentals and past track record are important, says Ayush Mittal.

"One has to do some bit of homework, and it is possible to come across promising companies run by some fantastic entrepreneurs," he said.

And to spot multibaggers, it is essential to understand the underlying business model of a company.

"An investor should look at them like a part owner and try to understand the business and the unique proposition that can drive the company to success," Ayush said.

Sometimes it is possible to get a quality company at throwaway price due to wrong perception or bad mood of the market, he smirks.

Multibagger returns

The Mittal brothers claim a number of stocks delivered them multibagger returns over the years. Here is a list of stocks that they are still holding in their portfolio.

Advice for new investors

The stock market is like an ocean; it will give you what you seek, says Ayush Mittal.

"You can seek quick money by trading or you can create a lot of wealth by focusing on the longer term and partnering with good companies early. Doing the latter is easier, more knowledgeable and more rewarding," he insists.

He has a simple tip for new investors. Look around you; most of the products you are using are sold by listed companies. A look at their long-term price charts would tell you that they are massive wealth creators. Look atMaruti Suzuki, Hero MotoCorp, Jockey (Page Industries), Eicher (Royal Enfield) and HDFC Bank – names they grew bigger right in front of you.

"Try to observe good products, businesses around you, check out their financials and if it makes sense, become a part owner when things are in your favour," says he.

"Don't come to market with the intention of buying today and selling in a few days, weeks or months. Try to invest in companies for years," advises Ayush Mittal.

Mittal brothers believe big wealth creation happens when a small or mid-sized company transitions into its next phase. Usually, it happens due to a differentiated business model, focused management and high growth rates. This all can lead to huge re-rating in valuations and create multibagger returns.

One crucial element to look out for is cash flow. Participate in companies that throw out cash. The Mittals prefer companies that have a smaller equity base, do not raise capital from market and have low debt-equity ratios.

They say they met with failure early in life for picking wrong companies that looked great in terms of various valuation ratios, but all of that turned out to be fraudulent or manipulated.

Not allocating enough capital to a stock was another mistake we kept on making in many instances. "In some cases, we sold some excellent ideas too early," Ayush recalls.

Sector wise views and Analysis of stock Market moves

USFDA observations :

Dec 2016 : Divi's Laboratories received form 483 with five observations during its routine Visakhapatnam (Unit-II) inspection which was carried out between November 29- December 6 by US Food and Drug Administration (USFDA). Divi's Laboratories ended 21.87% per cent lower at Rs 866.10. It hit a 52-week low of 821.35 and a high of Rs 1,109.50 on Friday.

The five observations are explained by the USFDA highlighted that no proper control was exercised over a computer system, facility equipment were not maintained to ensure purity quality strength, and documentation and records are not maintained or were inaccurate falsified. Divi's set up its second manufacturing facility at Visakhapatnam (Unit-II) in the year 2002 on a 350- acre site. The site has 14 multi-purpose production blocks. The company manufactures APIs and intermediates for generics among others at the manufacturing plant.

Leveraged Companies stocks wakeup to reality suddenly,once in a while : Aug 2015 Amtek Auto’s market capitalization fell by Rs. 3,000 crores in 1 month during Aug 2015

Leverage Effect

While Amtek Auto was profitable, in none of the historical years since 2005 did the company generate enough cash flows for the bond and the equity shareholders. For example: In FY 2014, the company generated cash flow from operations (CFO) of Rs. 1,119 crores and had debt of Rs. 7,789 crores on its Balance Sheet.Amtek Auto’s Debt increased from Rs. 1,274 crores in FY 2007 to Rs. 7,779 crores in FY 2014, 30% CAGR in the last 7 years. Assuming a 5 year loan, repayment of 20% of the principal and 12% p.a. interest rate translates to Rs. 2,489 crores cash flow to debt holders for the captioned year. This translates to a shortfall of Rs. 1,370 crores (1,119 - 2,489) for the providers of debt. When principal and interest repayment to debt-holders is circumspect, the question of providing cash flow to equity shareholders is at best illusory.

Dismal May IIP: Capital goods shares falter after a strong 1-month rally : 13th July 2015

Shares of capital goods firms eased in early trade Monday following a disappointing performance from the segment in the recently released May IIP numbers.

As per the data released by the government on Friday post market close, capital goods segment grew at a dismal 1.8 percent in May compared with 6.8 percent in April, an indication that revival in investments has been inconsistant.

This lends credence to the belief that presently these projects are isolated and confined to specific companies,” said rating agency CARE in a note last week.

Amid concerns of a slow pick-up in projects, investors seemed to be trimming their exposure to some of the listed companies which had sizzled in past one month on hopes of continuing revival in the segment.

While the benchmark Sensex was almost flat with a positive bias, the BSE Capital Goods index was down 0.6 percent at 18,317.96.

At 10.25 am, shares of engineering & construction major L&T fell 1.2 percent to Rs 1,848.45, BHEL also declined 1.2 percent to Rs 265.60, Kalpatru Power eased 0.7 percent to Rs 269.70 and Suzlon Energy was down 0.2 percent at Rs 23.15. Others such as Havells India, Bharat Electronics and Sadbhav Engineering were trading a tad lower. Several of the stocks in the capital goods space clocked significant gains in the past one month, with the BSE Capital Goods Index surging nearly 9 percent as against 3 percent rise in the benchmark Sensex.

ET Now 12th Aug 2015 : Q&A on Metal Stocks