Taxation of religious and charitable trusts

Special provisions for religious and charitable trusts

i. The newly introduced provisions of section 12AA of the Act provides for a procedure to be followed for grant of registration to a trust or institution.

ii. According to

which, the person in receipt of the income should make an application in Form

No. 10A for registration of the trust or institution to the Commissioner before

the expiry of a period of one year from the date of the creation of the trust or

the establishment of institution, whichever is later.

iii. However, where an

application for registration is made after the expiry of the aforesaid period,

the provisions of sections 11 and 12 will apply from the date of the creation

of the trust or the establishment of the institution if the Commissioner is,

for reasons to be recorded in writing, is satisfied that the person in receipt

of the income was prevented from making the application within the aforesaid

period for sufficient reasons. If the Commissioner is not so satisfied, the

provisions of section 11 and 12 will apply from 1st day of the financial year

in which the application is made.

iv. Along with Form

no. 10A (in duplicate), file the original (or certified copy of) Trust Deed, together with

one copy thereof, under which the trust is set up (original copy of the deed if

filed shall be returned).

v. Two copies of

accounts (i.e. Balance Sheet, income & Expenditure A/C., and Receipts &

Payment A/c.) for the years, prior to the financial year in which application is

made, are also to be filed along with application (if applicable). It should be

noted that here, only the copies of accounts of the trust since its inception

or during the last three years, whichever is less, are required to be filled.

vi. The Commissioner

shall call for documents and information and hold enquiries regarding the

genuineness of the Trust or Institution. After he is satisfied about the

charitable or religious nature of the objects and genuineness of the activities

of the trust or institution, he will pass an order granting registration and if

he is not so satisfied, he will pass an order refusing registration subject to

the condition that an opportunity of being heard shall be provided to the

applicant before an order of refusal to grant registration is passed by the

Chief Commissioner or Commissioner and the reasons for refusal of registration

shall be mentioned in such order.

vii. With effect from

June 01, 1999, an order on an application for registration of a trust or

institution is to be made by the Commissioner only and not by the Chief

Commissioner. However, in case trust falls under the jurisdiction of an income

tax authority having its headquarters at Mumbai, Chennai, Kolkata or Delhi, the

application is to be made to the Director of Income Tax (Exemptions).

viii. The order

granting or refusing registration has to be passed within six months from the

end of the month in which the application for registration is received by the

Commissioner and a copy of such order shall be sent to all the applicants. The

order is effective until withdrawn.

ix. It is also

provided that the grant of registration shall be one of the conditions for

grant of income-tax exemption u/s. 11 & 12 of the Income Tax Act, 1961.

x. The Taxation Laws

(Amendment) Act, 2006 has modified conditions as to registration of trust by

amending section 12A providing that the accounts of the trust or institution

for that year should be audited by a chartered accountant where the total

income of the trust or institution as computed under this Act without giving

effect to the provisions of section 11 and 12 exceeds the maximum amount which

is not chargeable to income-tax in any previous year and such audit report is

furnished along with the return of income for the relevant assessment year with

effect from the 1st day of April, 2006.

*Deferment of provisions for new registration procedure of Charitable Trusts and Institutions u/s 12AB/10(23C)/80G:*

~The Finance Act, 2020 prescribed a new electronic registration procedure for Charitable Trusts and Institutions under section 12AA/ 12AB / 10(23C)/ 80G.

~Originally was made applicable from 1st June 2020 : Subsequently extended to 1st October 2020 :Finally withdrawn from Finance Act, 2020 and made applicable from 1st April 2021.

~ So, New Scheme of electronic Registration deferred and made applicable w.e.f. 1st April 2021. Old Scheme would continue uptill 31st March 2021.

Amendments applicable from A.Y. 2020-21:*

~Audit Report in Form No. 10BB shall be uploaded one month prior to the due

date of submission of return of income. For A.Y. 2020-21 – uptill 31-12-2020.

~Income by way of Corpus Donation: By insertion of an Explanation, it has been clarified that w.e.f. A.Y. 2020-21, income of an entity covered by section 10(23C)(iv)/(v)/(vi)/(via) shall not include income in the form of voluntary contributions which are received with a specific direction that they shall form part of the corpus of the recipient.

~Corpus Donation given to other entities: Shall not be taken as application of income of the entity giving donation from the A.Y. 2020-21, if the following conditions are satisfied-

a) is given by an entity covered by section 10(23C)(iv)/(v)/(vi)/(via);

b) is given voluntarily with a specific direction that it shall form part of the

corpus of recipient; and

c) is given to an entity covered by section 10(23C)(iv)/(v)/(vi)/(via) or to a trust registered u/s. 12AA.

Taxation of Trusts ( other than exempt)

The taxability of the Trust depends upon the type of the trust. In the case of a non-discretionary trust, all income is taxable in the hands of the beneficiaries. On the other hand, in the case of a discretionary trust, in which the shares of the beneficiaries are unknown and indeterminate, it is taxed in the hands of trust at the maximum marginal rate.

Association of persons (AOP)

The income tax Act prescribes a specific mode for calculation of income and taxability in the case of Association of Persons.

Let's first discuss what is an Association of Persons.

Let's first discuss what is an Association of Persons.

An association of persons means an association in which two or more persons join in a common purpose or common action. The term person includes any company or association or body of individuals, whether incorporated or not. An association of persons may have companies, firms, joint families as its members – M.M Ipoh v CIT [1968] 67 ITR 106(SC).

Now lets see how income of Association of Persons (AoP)/ Body of Individuals(BoI) is determined.

Computation of Income of AoP

The total income under the different heads i.e. Income from house property, Profits or gains of business or profession, Capital gains, and income from other sources shall be worked out ignoring incomes exempt under Sections 10 to 13A.

From this make adjustments for the following:

i. If salary, commission, bonus or remuneration is paid by AoP/BoI to members, it will be added back. It may be noted that remuneration paid for actual services is also disallowed. This is due to the express provision in Section 40(ba).

ii. If interest is paid by AoP/BoI to members, it will be added back. But the following should be kept in mind:

Additional points to be kept in mind while disallowing interest:

Where interest is paid by an AoP/BoI to any member who has also paid interest to the AoP/BoI, the amount of interest to be disallowed shall be limited to the amount by which the payment of interest by the AoP/BoI to the member exceeds the payment of interest by the member to AoP/BoI.

If individual is member in representative capacity:

(a) Interest paid by the AoP/BoI to such individual or by such individual to AoP/BoI except as member in a representative capacity, shall not be taken into account;

(b) Interest paid by the AoP/BoI to such individual or by such individual to the AoP/BoI as member in a representative capacity and interest paid by the AoP/BoI to the person(s) so represented to the AoP/BoI, shall be taken into account.

Let me elucidate with an example:

Mr. William is a member of an AoP on behalf of his HUF i.e. in representative capacity. AoP pays interest on capital Rs. 1,50,000 to Mr. William in individual capacity. This amount will be deductible for the AoP as Mr. William is member in representative capacity but payment is made in individual capacity. Had Mr. William received interest on behalf of his HUF, such payment would've been disallowed in the hands of AoP.

If individual is member in individual capacity:

Interest paid by the AoP/BoI to such individual shall not be taken into account, if such interest is received by him on behalf, or for the benefit, of any other person.

Example: Mr. Varun is a member of an AoP i.e. in individual capacity. He receives interest on capital Rs. 1,50,000 made by his wife. This means he has received interest inrepresentative capacity. Hence it will be allowed in the hands of AoP. Had Mr. Varun been a member on behalf of his wife, such interest received would have been disallowed by virtue of Section 40(ba).

Also, deductions under Sections 80G, 80GGA, 80GGC, 80-IA, 80-IAB, 80-IB, 80-IC, 80-ID, 80-IE and 80JJA are to be adjusted (if any).

Total income thus obtained is taxed either at rates applicable to individual or at the maximum marginal rate, or a rate higher than maximum marginal rate.

Calculation of Tax of AoP

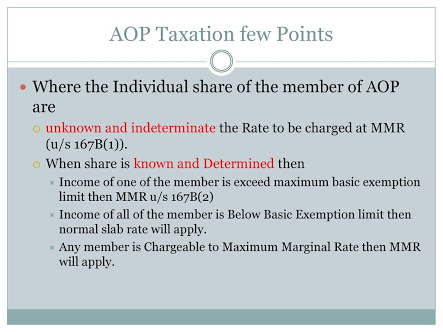

Tax of AoP/BoI shall depend on whether shares of members are determinable or not.

Shares of members are determinable:

a. If no member of AoP/BoI has income exceeding maximum amount not chargeable to tax:

The tax is chargeable on the total income of an AoP/BoI at the same rate as is applicable in the case of an individual.

b. If any member of AoP/BoI has income exceeding maximum amount not chargeable to tax:

In this case, AoP is taxed at maximum marginal rate.

And finally, if the total income of any member of the AOB/BOI (whether or not it exceeds the maximum amount not chargeable to tax in the case of an individual) is chargeable to tax at a rate higher than the maximum marginal rate, tax shall be charged

i. on that portion of the total income of the AOP/BOI which is relatable to such member at such higher rate

ii. and the balance of the total income of the AOP/BOI shall be taxed at the maximum marginal rate, 33.99%.

B. Shares of members are indeterminable:

Tax is charged on the total income of the AOP/BOI at the maximum marginal rate. However if any member is charged at a higher rate than maximum marginal rate, the income shall be taxed at such higher rate.

Calculation of Tax of members:

The assessment of the members of AOP or BOI depends on whether the AOP or BOI is chargeable to tax at the maximum marginal rate or rates applicable to individual or is not chargeable to tax at all.

Lets discuss it here below:

(i) Where AOP or BOI is chargeable to tax at a maximum marginal rate or any higher rate, the share of profit of a member is not included in his total income.

(ii) Where AOP or BOI is taxed at rates applicable to individual, the share of profit of a member from AOP or BOI is to be included in the total income of the member. But, the member is entitled to a rebate of tax on the entire share of profit at the average rate of tax applicable to total income.

(iii) Where AOP or BOI is not chargeable to tax at all, the share of profit of a member from AOP or BOI is included in his total income and he will pay tax on it. He is not entitled to any rebate of tax on such profits.

Taxation of partnership firm and its partners

Profits can't be taxed in the hands of partners even if profits are not taxed in the hands of firm due to exemptionWhere income chargeable to tax for a firm was nil due to certain deductions and exemptions, some assessing officers levied tax on the profit credited to its partners. This led to disputes and some taxpayers challenged this in courts.

“After looking into the issue, the Central Board of Direct Taxes (CBDT) has decided to clarify that such income in the hands of partners will be completely exempt,” said a senior finance ministry official.

The official said the partners that had already paid taxes on such income might be allowed to get refunds or adjustments against their future tax liability (but there are only a few such cases).

The move came after CBDT received representations in connections with interpretation of provisions of Section 10 (2A) of the Income-Tax Act. According to this section, inserted by the Finance Act, 1992, a tax partner is not liable to tax again on his share in the total income of the firm.

“The position is clear but the language of the section in the law created difficulty... The ambiguity will be cleared with this clarification. It will certainly provide a lot of relief to promoter companies and others from the consequences of unintended taxation,” said Deloitte Partner N C Hegde.

The profit of a partnership firm is divided among its partners in sync with their partnership deal. For the purpose of computation of income tax, identities of a partner and the firm are co-terminus. This means assets and liabilities are not different. The profits are credited to a partner’s account and he can plough it back into the business. It is more of a book entry, as no cash is generally drawn out of the company. Therefore, the income of partners was made tax exempt in 1993 to avoid double taxation.

As some assessing officers interpreted the section differently and started levying taxes on partners’ profits, clarifications were sought as to what amount would be exempt in the hands of partners in cases where a firm had claimed exemptions or deductions. The firm is taxed at 30 per cent plus surcharge and applicable tax and the partners’ profit is also taxed at the same rate.

“The income of a company is to be taxed in the in the hands of the company alone. This can, under no circumstances, be taxed in the hands of its partner,” says a CBDT circular that is likely to be made public soon.

However, partners’s interest income from capital in account and the remuneration they receive from the company will continue to be taxable according to the provisions of the I-T Act.Summary

The law in case of partnership taxation A partner is not liable to be taxed again on its share in a partnership company. Since the income of the firm is already chargeable to tax, taxing again in the hands of partners could lead to double taxation

The problem in case firms profits are exempt and hence tax is not chargeableSome tax authorities misinterpreted it and started taxing the profits in the hands of partners where a firm’s tax liability became nil due to certain exemptions and deductions

The clarification CBDT will clarify that the entire profit credited to partners’ accounts in a firm will be exempt from tax, even if the firm’s taxable income becomes nil on account of exemptions