Fully paid bonus shares are not a gift distributed of capital under profit. No new funds are raised. Earlier there was also a lot of confusion & chaos between the two fiercely debated concepts of taxation laws i.e. Capital & Revenue Expenditure which was finally settled after the case which come up in SC in 2006, named Commissioner of Income Tax v. General Insurance Corporation. Now it is also settled law that a bonus issue in the form of fully paid share of the company is not income for the Income Tax purpose. The undistributed profit of the company is applied and appropriated for the issue of bonus shares

Shares with Differential Rights

The Companies Amendment Act, 2000 has allowed companies to issue shares with differential rights. Industry had been demanding legislative changes for quite some time so as to enable companies to issue shares with differential voting rights. With the dematerialization of the stock markets, it is not always possible for the company to have a day-to-day break-up of its shareholding and who the major shareholders are. Many industrialists felt that their companies were in danger of hostile takeovers by outsiders. Therefore, there was a demand for allowing companies to issue equity shares without voting rights but without losing other benefits such as dividend, bonus shares, rights, etc. Accordingly, the Companies Amendment Act, 2000 has made the suitable legislative changes to allow companies to issue such shares. These rights may be differential with respect to dividend, voting or any other matter, subject to rules made by the Central Government and conditions specified therein.

The Ministry of Law, Justice and Company Affairs, Government of India has vide notification number G.S.R.167 (E) dated 9 March 2001 notified the Companies ((Issue of Share capital with differential voting Rights) Rules, 2001 to be followed by companies for issue of shares with differential voting rights. These rules have come into effect on the date of their publication in the Official Gazette.

Conditions to be satisfied

Every company limited by shares may issue shares with differential rights as to dividend, voting or otherwise, if -

1. the company has distributable profits in terms of Section 205 of the Companies Act, 1956 for preceding three financial years preceding the year in which it was decided to issue such shares.

2. the company has not defaulted in filing annual accounts and annual returns for three financial years immediately preceding the financial year of the year in which it was decided to issue such shares.

3. the company has not failed to repay its deposits or interest thereon on due date or redeem its debentures on due date or pay dividend.

4. the Articles of Association of the company authorizes the issue of shares with differential voting rights.

5. the company has not been convicted of any offence arising under, Securities Exchange Board of India Act, 1992, Securities Contracts (Regulation) Act, 1956, Foreign Exchange Management Act, 1999.

6. the company has not defaulted in meeting investors’ grievances.

7. the company has obtained the approval of share holders in a General Meeting by passing resolution as required under the provisions of sub-clause (a) of sub-section (1) of section 94 read with sub-section (2) of the said section.

8. in case of a listed public company, approval of share holders through Postal Ballot has been obtained for the same.

9. the notice of the meeting at which resolution is proposed to be passed is accompanied by an explanatory statement stating :–

a. the rate of voting rights which the equity share capital with differential voting right shall carry;

b. the scale or in proportion to which the voting rights of such class or type of shares will vary;

c. the company shall not convert its equity capital with voting rights into equity share capital with differential voting rights and the shares with differential voting rights into equity share capital with voting rights;

d. the shares with differential voting rights shall not exceed 25% of the total share capital issued;

e. that a member of the company holding any equity share with differential voting rights shall be entitled to bonus shares, right shares of the same class;

f. the holders of the equity shares with differential voting rights shall enjoy all others rights to which the holder is entitled to excepting right to vote as indicated in (a) above.

Companies Amendment Act 2017

The Parliament has passed Companies (Amendment) Bill, 2017 to strengthen corporate governance standards, initiate strict action against defaulting companies and help improve ease of doing business in the country,

The bill provides for more than 40 amendments to Companies Act, 2013. It will help in simplifying procedures, make compliance easy and take stringent action against defaulting companies.

Key Features of Bill

Group company structure and compliance procedures: The bill has changed definitions relating to 'holding company', 'subsidiary company', 'associate company'. It will have impact on group company structure and compliance procedures.

Compliance procedures and approval mechanism: It enhances scope of compliance procedures and approval mechanism of Related Party Transaction of related parties.

Shares on private placement basis: It amends this provision in parent Act. It will have impact on both – private companies and public companies.

Maintenance of Register of significant beneficial owners in a company: The bill adds this new provision. Besides, changes provisions relating to board meetings and shareholders' meetings, based on operational and compliance issues faced by the corporates.

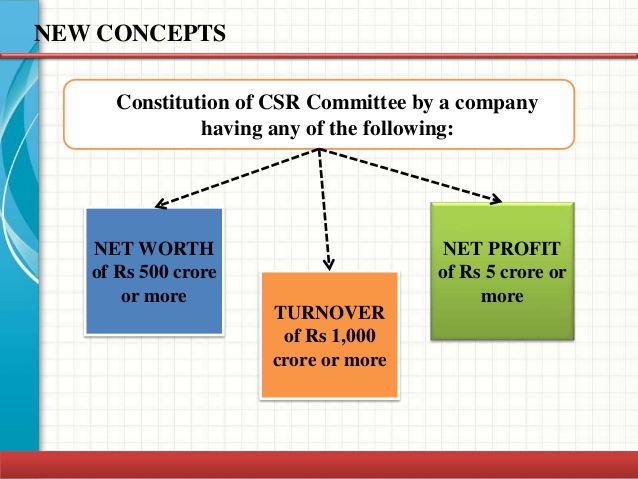

Corporate Social Responsibility (CSR): The amendment to CSR provisions are particularly related to its applicability and constitution of CSR. It takes into account the interpretational and operational issues.

Resident Director and Independent Director:It provides for clarity in applicability and role of Resident Director and Independent Director. Further it elaborated 'Pecuniary relationship' in relation to independent directors.

Loans to Directors: The bill substitutes entire section relating to 'Loans to Directors' under the Companies Act, 2013. It introduces certain checks and balances by way of approval process and for enabling 'loans to directors', in certain cases.

Managerial Remuneration: It liberalises provision related to Managerial Remuneration. It replaces requirement of Central Government approval by requirement of approval of shareholders, secured creditors and non-convertible debenture holders, as the case maybe.

Auditors Report: It mandates requirement that Statutory Auditor of company to report in its Auditors Report on compliance of provisions of managerial remuneration and whether remuneration paid to any director is in excess of prescribed limits.

FAQs on Companies Act 2013

Q1. What is SPICE?

A1. SPICE refers to “Simplified Proforma for Incorporating Company Electronically”. It is a simplified integrated process for incorporating a company in Form No. INC-32 along with e-MOA in Form No. INC-33 and e-AOA in Form No. INC-34. It has been recently introduced by the MCA and is effective from 1 October 2016.

Q2: In case the subscriber to the MOA is a foreign national residing outside India, his signatures and address etc. shall be witnessed by a Notary Public/Embassy/Consulate offices of Embassies as per the Rule 13 of the Companies (Incorporation) Rules, 2014. In such cases, how can the DSC of such a witness be affixed?

A2: In such cases, SPICe (INC-32) shall be filed along with the manually signed and duly attested MOA and AOA.

Q3: Whether every company is required to follow the SPICe process for incorporation of a company?

A3: As per Companies (Incorporation) Fifth Amendment Rules, 2016, all companies except Part I companies and a company having more than

7 subscribers/promoters are required to follow the SPICe process for incorporation with effect from 1 January 2017.

Q4: Can a company apply for name availability certificate by filing

Form INC-1 prior to filing of SPICe form?

A4: Yes, an applicant can make an application in Form INC-1 for name availability as per Rule 9 of the Companies (Incorporation) Rules,

2014, and file incorporation documents through SPICe mode on

approval of the name. However, such name shall be reserved for a period of 60 days from the date of making an application.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, name shall be reserved for a period of 20 days from the date of approval or such other period as may be prescribed shall be substituted.

Q5: Can a company be incorporated without a registered office?

A5: Yes, a company may be incorporated without having a registered office address by providing an address for correspondence in the incorporation form. However, as per Section 12 of the CA, 2013 read with Rule 25 of the Companies (Incorporation) Rules, 2014 on or from the 15th day of its incorporation and at all time thereafter, a company is required to have a registered office. The company which has not intimated address of its registered office at the time of incorporation is required to intimate to ROC of the same within 30 days of incorporation.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, a Company can have its registered office within 30 days of its incorporation as against 15 days as per the present requirement.

Q6: In case of an overseas subscriber and director, are the documents required to be notarised and apostilled for incorporation of a company?

A6: As per Rule, 13 of the Companies (Incorporation) Rules, 2014, where the subscriber to the MOA or a director to be appointed is a foreign national residing outside India, the MOA, AOA, proof of identity as well as address proof shall be attested in the following manner which is based on the country where the subscriber/ director reside or the registered office is situated in case of a body corporate being the subscriber:

1. Residing in a country which is part of the Commonwealth - by a Notary (Public) in that part of the Commonwealth;

2. Residing in a country which is party to the Hague Apostille Convention, 1961 - by a Notary (Public) and duly apostilled in accordance with the said Hague Convention; and

3. Residing in a country which is not party to the Hague Apostille Convention, 1961 - the documents shall be notarized before the Notary (Public) of such country and the certificate of the Notary (Public) shall be authenticated by a Diplomatic or Consular Officer empowered in this behalf under Section 3 of the Diplomatic and Consular Officers (Oaths and Fees) Act,

1948 (40 of 1948) i.e. attested by Public Notary and authenticated by Indian Embassy in the country of residence.

Q7: What is the due date to intimate the ROC for change in the situation of registered office of the company?

A7: As per Section 12(4) of the CA, 2013 read with Rule 27 of the

Companies (Incorporation) Rules, 2014, notice of every change in the situation of registered office of the company is required to be given to the ROC within 15 days of the change in Form INC-22.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, every change in the situation of registered office of the company is required to be given to the ROC within 30 days of the change.

Q8: What is OPC?

A8: As per Section 2(62) of the CA, 2013, OPC means a company which has only one person as a member.

Q9: Can a non-resident become a member of an OPC?

A9: In terms of Rule 3 of the Companies (Incorporation) Rules, 2014, only a natural person who is an Indian citizen and resident in India is eligible to incorporate an OPC. Therefore, a non-resident cannot become a member or nominee of an OPC.

For the purposes of this rule, the term “resident in India” means a person who has stayed in India for a period of not less than one hundred and eighty two days during the immediately preceding one calendar year.

Q10: How many OPCs can be incorporated by a person or in how many OPCs, he shall be eligible to be a nominee?

A10: As per Rule 3(2) of Companies (Incorporation) Rules, 2014 no person is eligible to incorporate more than one OPC or become nominee in more than one such company.

Rule 3(2) of the Companies (Incorporation) Rules, 2014 was substituted vide Notification dated 27 July 2016, Companies (Incorporation) Third Amendment Rules, 2016, as per which a natural person shall not be member of more than an OPC at any point of time and the said person shall not be a nominee of more than an OPC.

Q11: Can a company registered under Section 8 merge with another company with dissimilar objects?

A11: As per Section 8(10) of CA, 2013, a company registered under Section 8 can only be merged with another Section 8 company which has similar objects.

Q12: Is a Section 8 company required to seek permission of Central

Government (“RD”) for alteration of its AOA prior to getting the

same approved by the members by means of special resolution in general meeting?

A12: Yes, as per Section 8 (4)(i) of CA, 2013, Section 8 Company is required to obtain prior approval of Central Government (power delegated to “RD”) for alteration of its articles. However, members may pass the resolution for alteration of articles prior to the approval, but it shall be effective only post approval from the Central Government (“RD”).

Q13: How will the surplus be treated in case of winding up of Section

8 Company?

A13: As per Section 8(9) of CA, 2013 (applicable w.e.f. 15.12.2016), any asset remaining after satisfaction of the debts will be transferred to another company registered under Section 8 of the CA, 2013 having similar objects, subject to such conditions as the NCLT may impose, or the same may be sold and proceeds thereof will be credited to the Insolvency and Bankruptcy Fund formed under Section 224 of the Insolvency and Bankruptcy Code, 2016.

Q14: What is Small Company?

A14: As per Section 2(85) of the CA, 2013, a Small Company, other than public company, means a company where the:

(a) paid-up share capital of the company does not exceed INR 50

Lakhs or such higher amount as may be prescribed which shall not be more than five crore rupees; and

(b) turnover as per its last profit and loss account does not exceed 2 Crores or such higher amount as may be prescribed which shall not be more than twenty crore rupees:

Note: No higher amount has been prescribed as yet.

Further, holding company, subsidiary company, company registered under Section 8 or a company or body corporate governed by any special act will not be considered as a small company.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, the limit of paid up capital and turnover is proposed to be increased to INR 10 Crores and INR 100 Crores respectively.

Q15: Is it mandatory for the name of the company to be indicative of the nature of its business?

A15: No, it is not mandatory for the name to be indicative of the nature of its business.

Q16: Can a company have multiple and varied objects under its MOA?

A16: The Object Clause of the MOA of a company defines the objects or business it can carry and there is no bar under Section 4 (1) (c) of CA, 2013 on a company from having multiple objectives. As a matter of practice, the authorities do not approve more than four to five objects in the Object Clause of the MOA.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, the Company may engage in any lawful act or activity for the time being in force. In case, company proposes to pursue any specific objective, MOA shall state the said object for which company is incorporated.

Thus, as per the proposed Companies Amendment Bill, 2016, the question on multiple object or varied object would not arise.

Q17: Is a company required to alter its AOA as per the new format under the CA, 2013?

A17: As per the provisions of Section 5(6) of the CA, 2013, AOA of the company shall be in respective forms specified in Table F, G, H, I and J in Schedule I.

Also, as per the provisions of Section 5(9) of CA, 2013, provisions pertaining to AOA shall not apply to the AOA of company registered under any previous company law unless amended under the CA,

2013.

It is not necessary, but advisable that subsequent to any amendment to the AOA, the AOA is aligned as per the format specified under the CA, 2013.

Q18: Is a company required to pass a special resolution for altering its MOA?

A18: As per the provisions of Section 13(1) of the CA, 2013, a company is required to pass special resolution for altering its MOA except for the alteration of capital clause of MOA which could be altered by passing ordinary resolution as per the provisions of Section 61 of the CA,

2013.

Q19: Is an approval from Central Government (“RD”) required for alteration of MOA relating to change in place of registered office from one state to another?

A19: As per Section 13(4) of the CA, 2013, the alteration of MOA relating to change in place of registered office from one state to another shall not have any effect unless it is approved by the Central Government. As the powers of Central Government on this aspect are delegated to RD, the company will have to make an application and obtain the approval from the RD.

Q20: In case of shifting of registered office from one state to another there is a requirement of filing the order with each of the ROC’s. Is it possible to file two forms with a single CIN?

A20: No, it is not possible to file order approving the change of registered office with two different ROC’s with the same CIN.

As per Section 13 (7) of CA, 2013 read with Rule 31 of the Companies (Incorporation) Rules, 2014, the order of the RD approving the change of registered office from one state to another has to be filed in Form INC-28 with the ROC of each of the state within 30 days from the receipt of the certified copy of the order. Given the practical challenge, that the company cannot file Form INC-

28 twice with the same CIN, the form is required to be filed with the

ROC under whose jurisdiction the registered office was originally situated. The company will then have to file the Form INC-28 again with the new ROC where the registered office of Company is shifted.

Q21: What is the limit on the number of members for formation of association or partnership of persons?

A21: Section 464 of the CA, 2013 provides that no association or partnership can be formed with the number of members exceeding hundred (100) subject to the Rules prescribed under the CA, 2013. Rule 10 of Companies (Miscellaneous) Rules, 2014 provides that no association or partnership can be formed with the number of members exceeding fifty (50).

Therefore, the limit of number members for formation of association or partnership of persons is fifty (50).

Q22. Will the notifications, circulars, rules, orders issued for certain type of companies under Companies Act 1956 still be applicable for those companies under the Companies Act 2013?

A22: Section 465 (2) of the CA, 2013 provides that the notification, circular, rules, orders issued under CA, 1956, insofar as it is not inconsistent with the provisions of CA, 2013, be deemed to have been done or taken under the corresponding provisions of the CA, 2013. It further

provides that it shall continue to be in force, if it was in force at the commencement of the CA, 2013 and shall have effect as if made, directed, passed, given, taken, executed, issued or done under or in pursuance of the CA, 2013.

Considering the aforesaid, notifications, circulars, rules, orders issued for certain type of companies under the CA, 1956 will also be applicable for those companies under the CA, 2013.

Q23. Is a Small Company required to prepare Cash Flow Statement?

A23: As per Proviso to Section 2(40), exemptions have been granted to Small Company, OPC and Dormant Company with effect from 1st April, 2014. Therefore, it is not mandatory for a Small Company to prepare Cash Flow Statement.

Q24: Is it mandatory for a company to have a common seal?

A24: No, as per the Companies (Amendment) Act 2015, the companies are not mandatorily required to have common seal. Further, the existing companies may amend their AOA to this effect.

Capital and Allied Matters

Q25: Is a private company required to follow the rules pertaining to issue of shares with differential voting rights?

A25: As per notification No. GSR 464(E), dated 5th June, 2015 issued by MCA, Section 43 pertaining to kinds of share capital is not applicable to a private company, if same is provided in the MOA and AOA of that private company and hence, private company can issue shares with differential voting rights without following the conditions prescribed for issue of shares with differential voting rights.

Q26: Is it mandatory to issue share certificate under the common seal of the company?

A26: No, it is not mandatory to issue share certificates under the common seal of the company. As per the Companies (Amendment) Act, 2015 read with Companies (Share Capital and Debentures) Second Amendment Rules, 2015, every share certificate shall be issued under the common seal, if the company has a common seal.

Q27: Who is required to sign the share certificate?

A27: As per Section 46 of the CA, 2013, read with Rule 5(3) of the Companies (Share Capital and Debentures) Rule, 2014, a share certificate can be signed in the following manner:

a. Company other than OPC:

(i) If a company has a common seal, the share certificate is required to be signed by two Directors and Secretary or any person authorized by the Board for the purpose.

(ii) If a company does not have a common seal, then the share certificates shall be signed by two directors or a Director and the Company Secretary, where the company has appointed a Company Secretary.

b. OPC:

(i) If a company has a common seal, the share certificate is required to be signed by one Directors or a person authorized by the Board of Directors of the company and Secretary or any other person authorized by the Board for the purpose.

(ii) If a company does not have a common seal, then the share certificates shall be signed by a person in whose presence the seal is required to be affixed.

Q28: What are the modes available for issue of further shares?

A28: As per Section 23 of the CA, 2013, following modes are available for issue of further shares:

1. Public Companies:

a) Public offer through issue of prospectus;

b) Private Placement/ Preferential allotment;

c) Issue of shares to employees under a scheme of employees’

stock option; and

d) Right issue/ bonus issue

2. Private Companies:

a) Right issue/ bonus issue;

b) Issue of shares to employees under a scheme of employees’

stock option; and

c) Issue of shares to any person through preferential allotment/

private placement.

Q29: Can subsidiary company hold shares in its holding company?

A29: As per Section 19 of the CA, 2013, subsidiary company cannot hold shares in its holding company and any such holding shall be void except in following circumstances:

a) where the subsidiary company holds such shares as the legal representative of a deceased member of the holding company;

b) where the subsidiary company holds such shares as a trustee;

c) where the subsidiary company is a shareholder even before it became a subsidiary company of the holding company.

Q30: Can a company issue shares at a discount?

A30: As per Section 53 of CA, 2013, no company shall issue shares at a discount other than issue of sweat equity shares. Any shares issued by a company at a discounted price shall be void.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, a company may issue shares at a discount to its creditors when its debt is converted into shares in pursuance of any statutory resolution plan or debt restructuring scheme in accordance with any guidelines or directions or regulations specified by the Reserve Bank of India under the Reserve Bank of India Act,

1934 or the Banking (Regulation) Act, 1949.

Q31: Is a company required to obtain shareholders’ approval for preferential issue of shares?

A31: Yes, as per Section 62(1)(c) read with Rule 13(1) of the Company (Share Capital and Debenture) Rules, 2014, a company is required to obtain shareholders’ approval by way of special resolution in the general meeting of the company.

Q32: What is the maximum number of persons to whom private placement offer can be made?

A32: As per Section 42 of CA, 2013, a company can issue securities to such persons not exceeding fifty or such higher number as may be prescribed.

As per Rule 14 of Companies (Prospectus and Allotment of Securities) Rules, 2014, the limit of number of persons to whom the securities are to be issued cannot exceed two hundred person in aggregate in a financial year.

Q33: Who are exempted from being included in the limit of 200 persons to whom private placement offer is issued?

A33: As per Section 42 of CA, 2013 read with Rule 14 of the Companies (Prospectus and Allotment of Securities) Rules, 2014, any offer made to the qualified institutional buyers or the employees of the company under the employee stock option scheme are exempted from being considered in determining the maximum limit.

Q34: Is a share valuation report required in case of Right Issue of

Shares?

A34: Share valuation report is not required in case of right issue of shares.

However, in case of issue of shares to non-resident, valuation is required to be carried out as per the provisions of FEMA.

Q35: Can Board of Directors of a company take a decision to issue

Preference Shares?

A35: No, as per Rule 9(1)(a) of Companies (Share Capital and Debentures) Rules, 2014, preference shares can only be issued after obtaining approval of shareholders through a special resolution in general meeting. Hence, Board of Directors can only recommend to the shareholders along with a detailed explanatory statement for approval.

Q36: Can a private company issue debentures to public?

A36: No, a private company cannot issue debentures to public. The definition of a ‘private company’ as laid down in Section 2 (68) of the CA, 2013 prohibits a company from inviting public to subscribe to any securities issued by it. Given the prohibition to subscription by the public, a private company can issue debentures only through private placement.

Q37: Is a company required to intimate the ROC post redemption of preference shares?

A37: Yes, as per Section 64 of the CA, 2013, a company is required to intimate the particulars of redemption to the ROC in Form SH-7 within

30 days of redemption of preference shares.

Q38: What is the form for filing return of allotment with the ROC post allotment of securities?

A38: As per the provisions of Section 39(4) of the CA, 2013 read with Rule

12 of the Companies (Prospectus and Allotment of Securities) Rules,

2014, a Company is required to file a return of allotment within 30 days from the date of allotment of shares in Form PAS-3 with the ROC along with the list of allottees.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, in case of allotment of shares issued through private placement procedure, the return of allotment shall be filed with the ROC within 15 days from the date of allotment.

Q39: Is it mandatory to get the securities listed in case of a public offer?

A39: Yes, as per Section 40 of the CA, 2013, it is mandatory for companies to make an application to one or more recognised stock exchange or exchanges and obtain permission for the securities to be dealt with in such stock exchange or exchange before making a public offer.

Q40: Section 40(1) of the CA, 2013 requires a company to make an application to the stock exchanges for listing of securities and obtaining permission prior to making an offer. The requirement under Section 73(1) of the CA, 1956 was only to make an application. Hence, is it now required to obtain prior permission from the stock exchanges or is making an application a sufficient compliance?

A40: As per Section 40(1) of the CA, 2013, it is specifically provided that every company which desires to make public offer should make an application to one or more stock exchanges and take prior permission for dealing in securities. Hence, company intending to make a public offer is required to make an application and obtain approval of shareholders prior to making an offer.

Q41: What is the offer period for rights issue?

A41: As per Section 62(1)(a)(i) of the CA, 2013, the rights issue offer shall be kept open for a minimum period of 15 days and maximum period of 30 days. However, in case of a private company, offer period may be reduced by obtaining consent in writing or through electronic mode of 90% of the members of private company. [This exemption is available to private company vide notification No. GSR 464(E) dated

5th June 2015].

Q42: Can a company pass the resolution for issue of securities by way of circulation?

A42: As per Section 179(3) of the CA, 2013, resolution with regard to issue of securities should be discussed and passed at a duly convened Board meeting and hence, resolution cannot be passed through circulation.

Q43: Can a company convert the existing shares into shares with differential voting rights and vice versa?

A43: No, as per Rule 4(3) of Companies (Share Capital and Debenture) Rules 2014, company cannot convert its existing shares into shares with differential voting rights and vice versa.

Q44: What is meant by sweat equity shares and to whom can a company issue sweat equity shares?

A44: As per Section 2(88) of the CA, 2013, sweat equity shares means shares issued at a discount or for consideration other than cash to the Directors and employees for providing know-how or making available rights in the nature of intellectual property rights or value addition.

As per Rule 8(1) of the Companies (Share Capital and Debentures) Rules, 2014, sweat equity shares can be issued to employees of the company as classified below:

permanent employee of the Company who has been working in India or outside India, for at least one year;

a Director of the Company, whether a whole time Director or not;

an employee or a director as specified above of a subsidiary or of a holding of the company

Q45: What is the lock-in period for sweat equity shares?

A45: As per Rule 8(5) of the Companies (Share Capital and Debentures) Rules, 2014, sweat equity shares issued to the employees or Directors of the Company shall be locked-in for a period of 3 years from the date of issue and the same shall be stamped or mentioned in any other prominent manner on the share certificate.

Q46: What is the cap on issue of sweat equity shares?

A46: The cap on issue of sweat equity shares is as follows:

(i) In a year, issue shall not exceed 15% of the existing issued equity share capital or issue value of INR 5 crores whichever is higher;

(ii) At any time, issue shall not exceed 25% of the total paid up equity capital of the Company but a start-up company can issue sweat equity shares not exceeding 50% of its paid up capital up to five years from the date of its incorporation [The Companies (Share Capital and Debentures) Third Amendment Rules, 2016].

Q47: Are all kinds of companies required to obtain approval of shareholders by means of a special resolution for issuing shares under ESOP?

A47: As per Section 62(1)(b) of the CA, 2013, all companies other than private companies are required to obtain approval by means of a special resolution in general meeting for issuing shares under ESOP. As per notification No. GSR 464(E) dated 5 June 2015, in case of private companies, an ordinary resolution by the shareholders would suffice the requirement for issue of shares under ESOP.

Q48: Can an employee who is also a promoter of a company eligible to obtain sweat equity shares and employee stock of option?

A48: As per Rule 12 of Companies (Share Capital and Debentures) Rules,

2014, employee who is also a promoter or person belonging to the

promoter group is specifically excluded from obtaining shares issued under ESOP. In case of a start-up company as defined in notification number GSR 180(E) dated 17th February, 2016 issued by the Department of Industrial Policy and Promotion, Ministry of Commerce and Industry Government of India, Government of India, this condition shall not apply up to five years from the date of its incorporation or registration. [The Companies (Share Capital and Debentures) Third Amendment Rules, 2016].

However, in case of sweat equity shares, the said exclusion is not specified in the provisions. Thus, an employee who is also a promoter of a company is eligible to get sweat equity shares and not the employee stock option.

Q49: Will all the employees of the company be eligible to participate in the ESOP?

A49: No, only those employees as determined by the management of the company shall be eligible to participate in the ESOP.

Q50: Has Section 66 pertaining to reduction of capital been enforced?

A50: Section 66 of the CA, 2013 for reduction of capital has been enforced with effect from 15 December 2016 and accordingly, every company is required to follow the provisions prescribed thereunder for reduction of share capital.

Q51: What is meant by the term “Buy back of Shares” and funds utilized for buy back?

A51: “Buy back” is a concept by which a company purchases its own shares or other specified securities by following the procedures laid down in Section 68 of the CA, 2013. The company can utilize free reserves, securities premium account or proceeds of the issue of fresh issue shares or other specified securities to purchase its own shares.

Q52: What is the limit prescribed for buy back of shares?

A52: As per the provisions of Section 68(2) of the CA, 2013, in case a special resolution has been passed by the members of the company at the general meeting, the company can buy back shares not exceeding 25% of the aggregate of paid-up capital and free reserves of the company and in case of buy back of equity shares in any financial year, it should not exceed 25% of its total paid-up equity capital in that financial year.

Provided that the company can buy back 10% of the total paid-up equity capital and free reserves after obtaining approval of Board. In such a case, approval of the shareholders’ by means of a special resolution will not be required.

Q53: Can a company buy back its shares if it is not authorized by its

AOA?

A53: As per the provisions of Section 68(2) of the CA, 2013, a company cannot buy back its shares if it is not authorized by its AOA.

Q54: What is the time limit for completion of buy back?

A54: As per the provisions of Section 68(4) of the CA, 2013, every buy back shall be completed within a period of one year from the date of passing of the special resolution or resolution passed by the Board, as the case may be.

Directors

Q55: What is DIN?

A55: DIN is a unique identification number issued to a prospective director by the DIN cell of Ministry of Corporate Affairs (“MCA”). An individual should hold a DIN before being appointed as a director in any Company.

Q56: Is it mandatory for a director to hold digital signature?

A56: A director who is already holding a DIN can obtain a digital signature, though it is not mandatory. If a person is not holding DIN and intends to be appointed as a Director in a Company, he should obtain a digital signature for making an application for obtaining DIN to the DIN cell.

Q57: Who can be appointed as director?

A57: As per the provisions of Section 152 of the CA, 2013, an individual holding a valid DIN and not disqualified from being appointed as Director under Section 164 of the CA, 2013, is eligible to be appointed as Director. He shall give his consent to act as a director in writing along with the disclosure of his interest and a declaration that he is not disqualified to become a director under CA, 2013.

Q58: What are the broad steps involved in appointment of a director?

A58: The broad steps involved in appointment of a director are: Obtain DSC;

Obtain DIN by filing Form DIR-3;

Declaration that he is not disqualified from being appointed as the Director in form DIR-8;

Written consent of director for his appointment in form DIR-2; Interest of the Director if any, in any other entity in form MBP-

1;

Approval of Board of directors by Board Resolution;

Approval of Shareholders by shareholders Ordinary

Resolution;

Intimation of appointment of director to ROC in Form DIR-12

Q59: Can a director be appointed by the Board of a company?

A59: Although, as per the provisions of Section 152 of the CA, 2013, the directors of the Company are required to be appointed by the shareholders of the Company in general meeting, the Board of the Company, if authorised by the AOA of the company can appoint director under following circumstances:

Appointment of additional director; Appointment of nominee director; Appointment of alternate director;

Appointment of director for filling casual vacancy

Q60: What shall be the effective date of resignation of a director?

A60: As per the provisions of Section 168(2) of the CA, 2013, the resignation of a director shall take effect from the date on which the notice is received by the company or the date specified in the notice, whichever is later.

Q61: What are the procedures to be carried out by a director at the time of resignation from the company?

A61: As per the provisions of Section 168 of the CA, 2013 read with Rule

15 and Rule 16 of the Companies (Appointment and Qualification of Directors) Rules, 2014, a director may resign from his office in the following manner:

(i) by giving a written notice to the Board; and

(ii) shall forward a copy of his resignation along with detailed reasons to the ROC in Form DIR-11 within 30 days of resignation.

In case of resignation of a foreign director, such a foreign director can authorize in writing a practising chartered accountant or cost accountant in practice or company secretary in practice or any other resident director of the company to sign Form DIR-11 and file the same on his behalf with the ROC.

The Company on receipt of the notice of resignation from the Director shall:

(i) take the same on record;

(ii) intimate the ROC in Form DIR-12 within 30 days; and

(iii) place the fact of such resignation in the Board’s Report laid in the immediately following general meeting of the company.

Q62: How long will the director be liable for the offences occurred during his tenure?

A62: The director shall be liable for the acts / transactions occurred during his tenure even after resignation and disassociation with the company.

Q63: Who are KMPs and whether their appointment requires additional compliance?

A63: KMP has been defined under Section 2(51) of the CA, 2013, to mean: Chief Executive Officer or Managing Director or Manager; Company Secretary;

Whole Time Director; Chief Financial Officer

The following companies, are required to appoint KMP and their appointment shall be intimated to the ROC in Form DIR

12 and the return of their appointment shall be filed in Form

MR 1:

Listed company;

Public company having paid up share capital of INR 10 crores or more

Provided that as per Rule 8A of the Companies(Appointment and Remuneration Managerial Personnel), Rules, 2014, a company other than those mentioned above needs to appoint a whole time Company Secretary if its paid-up share capital is rupees five crore or above.

Also, after the Companies (Appointment and Remuneration of Managerial Personnel) Amendment Rules, 2016, MR-1 is not required to be filed for Chief Executive Officer, Company Secretary and Chief Financial Officer w.e.f. 30.06.2016.

Q64: Can a director be removed from the Company?

A64: Yes, shareholders of the Company may by passing an ordinary resolution in general meeting remove a director, but after giving a reasonable opportunity of being heard pursuant to Section 169 of the CA, 2013. A special notice would be required for passing such resolution. Once shareholders remove a director from the Board, the Board of Directors cannot reappoint him.

Board Related Matters

Q65: Are all companies required to hold Board Meetings every quarter?

A65: As per Section 173 of the CA 2013 and Secretarial Standards 1, all companies – whether private limited companies or public companies are required to hold at least four meetings of its Board of Directors in each quarter every year where the gap between two consecutive board meetings is not more than one hundred and twenty days.

As per the notification No. GSR 466 E dated 05 June 2015, in case of a Section 8 company, the Board of Directors of the company shall hold at least one meeting within six calendar months.

In case of an OPC, if there is only one director on the Board of

Director, the quarterly board meetings are not required to be held.

However, if the OPC has more than one director or in case of small or dormant companies, it will suffice the requirement, if they hold at least one meeting in each half of the calendar year and the gap between two meetings should not be less than ninety days. Further, any business which is required to be transacted at the meeting of the Board of Directors of a company, it shall be sufficient if, in case of such OPC, the resolution by such director is entered in the minutes book.

Q66: Can a Company restrict a director from participating in a meeting through video conferencing if he has not given an intimation of participating in the video conference meetings at the beginning of the year?

A66: No, a company cannot restrict a director from participating in a meeting through video conference if he has not given intimation at the beginning of the year. An intimation given to the company or chairman on receipt of the notice calling the board meeting would suffice the requirement for attending the meeting through video conferencing.

Q67: What are the matters which cannot be considered at a meeting held through video conferencing or other audio visual means?

A67: As per Rule 4 of the Companies (Meetings of the Board and its Powers) Rules, 2014, following matters shall not be considered through video conferencing or other audio visual means:

(i) Approval of annual financial statements;

(ii) Approval of board’s report;

(iii) Approval of prospectus;

(iv) Audit Committee Meetings for consideration of financial statement including consolidated financial statement, if any, to be approved by the Board of Directors pursuant to Section 134(1) of the CA, 2013;

(v) Approval of the matter relating to amalgamation, merger, demerger, acquisition and takeover.

However, as per The Companies (Amendment) Bill, 2016, which is yet to be notified, has proposed participation of Directors on certain items at Board Meetings through video conference or other audio visual means if there is quorum through physical presence of Directors.

Q68: Is the notice calling for the board meeting required to state that the meeting is being convened at a short notice?

A68: Yes, as per Secretarial Standards-1 effective from 1 July 2015, a company is required to state the fact that the board meeting is convened at a short notice in the notice calling the meeting. However, the CA, 2013 is silent in this regard.

Q69: Can a director interested in the contract participate in the board meeting or be counted for quorum as per Section 174 of CA

2013?

A69: As per provisions of Section 188 of the CA 2013, if any director is directly or indirectly, concerned or interested in a contract or arrangement or proposed contract or arrangement then such director shall disclose the nature of his concern or interest at the meeting of the Board in which the contract or arrangement is discussed and shall not participate in such meeting.

However, in case of a private limited company, as per notification No. GSR 464E dated 5th June 2015, an interested director can participate and vote in a board meeting after disclosing his interest in the particular transaction. The interested director, will be included for the purpose of determining the quorum of the meeting.

Q70: Can meetings of the Audit Committee be held through video conference?

A70: Yes, the meetings of Audit Committee can be held through video conference except the meeting where financial statements including consolidated financial statements is considered for approval under Section 134(1) of CA, 2013.

Q71: Is a company required to obtain approval of the Audit Committee for all the transaction entered into with related parties?

A71: Yes, as per Section 177 of CA, 2013 read with Rule 6 and 6A of the Companies (Meetings of Board and its Power) Rules, 2014, a company is required to obtain approval of the Audit Committee for all the transactions entered into with related parties. Also, the Audit Committee has an option to grant omnibus approval which shall be valid for a period of one financial year.

However, as per the Companies (Amendment) Bill, 2016 which is yet to be notified, proposes to insert following amendments:

Ratification by Audit Committee of transactions involving amount not exceeding INR 1 Crores within 3 months of transaction;

Consequences of non-ratification of the transactions; Exemption from approval of audit committee to transaction

between a holding company and its wholly owned subsidiary.

Q72: Which powers of the board are required to be exercised at a duly convened board meeting?

A72: As per Section 179 of CA, 2013 read with Rule 8 the Companies (Meeting of Board and its Powers) Rules 2014, following powers of the Board can be exercised by means of a resolution passed at a duly convened Board meeting:

(a) To make calls on shareholders in respect of money unpaid; (b) To authorise buy back of securities;

(c) To issue securities, including debentures, whether in or outside India;

(d) To borrow monies;

(e) To invest the funds of the company;

(f) To grant loans or give guarantee or provide security in respect of loans;

(g) To approve financial statements and the Board’s report; (h) To diversify the business of the company;

(i) To approve amalgamation, merger or reconstruction;

(j) To take over a company or acquire a controlling or substantial stake in another company;

(k) To make political contributions;

(l) To appoint internal auditors and secretarial auditor; (m) To appoint or remove KMP;

As per the notification dated 5 June 2015, in case of a Section 8

Company, matters referred to in point no. (d), (e) and (f) may be decided by the Board by circulation instead of at a meeting.

Q73: Can a private company grant loan to its directors?

A73: Sec 185 of the CA 2013 restricts loans to directors including private limited companies. However as per the notification dated 6th Jun

2015, a private company may grant loan to its directors subject to fulfilment of all of the following conditions:

No body corporate has invested in the share capital of the company;

Borrowings from banks/financial institutions/any other body corporate is less than twice the paid up share capital of the company and fifty crores whichever is lower; and

There is no subsisting default in repayment of existing borrowings at the time of the transaction.

Q74. Can loan be given by a holding company to its wholly owned subsidiary company or a guarantee given or security provided by a holding company to any loan made to its wholly owned subsidiary?

A74: Yes, as per the proviso to Section 185(1) loan given by a holding company to its wholly owned subsidiary company or a guarantee given or security provided by a holding company in respect of any loan made to its wholly owned subsidiary company is exempt from the purview of Section 185 of CA, 2013 provided the same is utilised for the principal business activities by the subsidiary.

Q75: Is a private company exempt from Section 186 of CA, 2013?

A75: A private company is not exempt from the applicability of Section 186 of CA, 2013.

Q76: Is loan to an employee covered within the ambit of Section 186 of the CA, 2013?

A76: As per General Clarification No.04/2015 issued by the Ministry of Corporate Affairs dated 10 March 2015, loans and/or advances made by the companies to their employees, other than the managing or who-time director are not governed by the requirement of Section 186 of the CA,2013. This clarification will however, be applicable if such loans/advances to employees are in accordance with the conditions of service applicable to employees and are also in accordance with the remuneration policy, in cases where such policy is required to be formulated.

Further, as per the Companies (Amendment) Bill, 2016 which is yet to be notified, proposes to exclude ‘employees’ from the definition of

‘any person’.

Q77: Will salary advances made by the Company for only one or two months (without interest) come within the preview of “Loan”?

A77: There is a difference between advance and loan. Loan is lending of money with absolute promise to repay whereas advance is to be adjusted against supply of goods and services. Advance given to employees against current month’s salary will not be in the nature of loan and the same will not fall within the purview of Section 186.

Q78: Is unanimous consent of the board required for entering into a transaction under Section 186?

A78: Yes, as per Section 186(5) of the CA, 2013, consent of all the directors present at the meeting is required for entering into a transaction.

Q79: When is the approval from the public financial institutions not required for entering into transactions under Section 186?

A79: As per the proviso to Section 186(5) of the CA, 2013, approval of public financial institutions is not required under the below circumstances:

The amount involved in the transaction does not exceed 60%

of the paid up share capital, free reserves and securities

premium account and 100% of its free reserves and securities premium account, whichever is higher; and

There is no default in repayment of loan installments and interest to public financial institutions.

Q80: What is the due date for making entries in the new format of Register of Loans, Guarantees, Security and Acquisition? Also, is a company required to update the transactions covered under Section 372A of the CA 1956?

A80: Since, 1 April 2014 it is mandatory for a company to maintain the Register of Loans, Guarantee, Security and Acquisition made by the company in Form MBP-2. Also, as per the clarification issued by MCA vide Circular No. 15/2014, registers maintained by companies pursuant to Section 372A (5) of the CA, 1956 may continue as per the requirement under these provisions and the new format prescribed (MBP-2) shall be used for transactions entered on and from 1 April

2014.

Q81: Which are the transactions covered under Section 188 of the CA,

2013?

A81: The following transactions are covered under Section 188 of the CA,

2013:

Sale, purchase or supply of goods or materials;

Sale or disposal of or buying of property of any kind; Leasing of property of any kind;

Availing of or rendering any services;

Appointment of an agent for purchase or sale of goods, materials, services or property;

Related party’s appointment to any office or place of profit in the company or its subsidiary or associate company;

Underwriting of subscription of any securities or derivatives;

Q82: Can Company provide interest free loans?

A82: No, the Company shall not provide any loan without interest. As per Section 186(7) of the CA, 2013, no loan shall be given at a rate lower than the prevailing yield of one year, three year, five year or ten year Government Security closest to the tenor of the loan.

Q83: Which are the transactions that would not require approval of the shareholders under Section 188?

A83: As per Section 188(1) of the CA, 2013, following transactions do not require approval of the shareholders under Section 188 of the CA,

2013:

Transactions in ordinary course of business and on arm’s length basis;

Transactions between holding company and wholly owned subsidiary company whose accounts are consolidated and laid before shareholders at AGM.

Q84: Can a member of a private company interested in a particular transaction participate and vote at a general meeting?

A84: Yes, an interested member of a private company can participate and vote at general meeting on matters requiring approval for related party transaction pursuant to exemption Notification No. GSR 464(E), dated 05th June, 2015.

Q85: Can a Director who is also a member of a private company participate and vote at a meeting for the transaction related to payment of remuneration to such directors?

A85: Yes, an interested Director who is also a member of a private company can participate and vote at meeting to approve the transactions related to payment of remuneration to such Director.

Q86: In what circumstances is the prior approval of Board required for entering into specified contracts or arrangements with related parties under Section 188?

A86: As per Section 188 of the CA 2013, Board’s approval is required for the contracts or arrangements with related parties specified in Section 188(1) (a) to (g) which are either not in ordinary course of business or not at arm’s length basis. Further, in the case the transactions exceed the prescribed threshold, prior approval by ordinary resolution of the company shall be required for entering into such contract or arrangement with related party.

Q87: As per the second proviso to Section 188 (1) of the CA, 2013, no member of the company shall vote on such ordinary resolution, to approve any contract or arrangement which may be entered into by the company, if such member is a related party.

What is the meaning of related party in such cases?

A87: The MCA vide General Circular No. 30/2014 dated 17 July 2014 has clarified that ‘related party’ referred to in the second proviso has to be construed with reference to the contract or arrangement for which the said ordinary resolution is being passed. Thus, the term ‘related party’ in the above context refers only to such related party with whom the contract or arrangement is being proposed and for which the said ordinary resolution is being passed.

However, as per the Companies (Amendment) Bill, 2016 which is yet to be notified, proposes to remove non-participation of related party shareholder of a public Company, in passing of the resolution of such public Company in which 90% or more members, in number, are relatives or promoters of related parties.

Q88: Which are the transactions exempted from being entered in Register of Contracts and Arrangements in which the directors are interested?

A88: The following transactions are exempted from being entered in the Register of Contracts and Arrangements in which the directors are interested:

Sale/purchase/supply of any goods/services, if the value does not exceed five lakh rupees in the aggregate in any year

Transaction by a banking company for the collection of bills in the ordinary course of its business

Q89: Which are the different type of companies required to adopt vigil mechanism?

A89: Pursuant to Section 177(9) of the CA, 2013 read with Rule 7 of the Companies (meetings of Board and its Power) Rules, 2014, Vigil Mechanism is required to be adopted by the following companies:

Every listed company;

Companies which accept deposits from the public;

Companies which have borrowed money from banks and public financial institutions in excess of fifty crore rupees.

Management and Administration

Q90: When should a company convene its first AGM?

A90: As per Section 96 of the CA, 2013, the first AGM of a company should be held within a period 9 months from the date of close of first financial year.

Example – If a company’s financial year ends on 31 March, the first AGM of the company shall be held latest by 31 December of that year.

Q91: Can AGM be held at a place situated outside the limit of city, town or village in which the Registered Office is situated?

A91: As per the provisions of Section 96(2) of the CA, 2013, AGM cannot be held at a place situated outside the limit of city, town or village in which the Registered Office is situated. Provided in case of Government companies, AGM can be held at a place which the Central Government may approve i.e. a Government Company can convene its AGM at a place other than limit of city, town or village in which the Registered Office is situated if the Central Government may approve.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, AGM of an unlisted company may be held at any place in India if consent is given in writing or by electronic mode by all the members in advance.

Q92: Can AGM be convened at shorter notice?

A92: Yes, as per Section 101(1) of the CA, 2013, AGM can be convened after giving a shorter notice subject to consent in writing or in electronic mode is received from 95% of the members entitled to vote thereat.

Q93: What shall be the Quorum of an AGM?

A93: As per Section 103 of the CA, 2013, quorum for the AGM of a private limited company is 2 members personally present, but in case of public limited company, quorum for AGM is based on the number of members in the Company, as stated below:

Quorum required

Total number of member in the

Company

(members to be personally present)

5

Less than 1000

15

1000 to 5000

30

More than 5000

Q94: Can EGM be held at a place situated outside India?

A94: No, EGM of a company cannot be held outside India.

However, as per the proposed Companies Amendment Bill, 2016 which is yet to be notified, EGM of a company, other than a wholly owned subsidiary of a company incorporated outside India, shall be held at a place within India.

Q95: Who can be appointed as proxy?

A95: As per Section 105 of the CA, 2013, proxy need not be a member of the company and any person can be appointed as a proxy.

Q96: What are the restrictions on a proxy during the shareholders meeting?

A96: As per Section 105 of the CA, 2013, at a shareholders meeting, a proxy can vote only through poll and not by show of hands. Also a proxy is not entitled to speak at the meeting.

Q97: Can a member of Section 8 Company appoint any other person as its proxy?

A97: No, as per Rule 19 of Companies (Management and Administration) Rules, 2014, a member of Section 8 Company can appoint only another member of the same company as its proxy.

Q98: For how many members can a person be appointed as a proxy?

A98: As per Section 105 of the CA, 2013, read with Rule 19 of the Companies (Management and Administration) Rules, 2014, a person can act as proxy on behalf of maximum 50 members and holding voting rights on shares not more than 10% of total share capital.

In case of a person holding proxy for a member, holding voting rights on shares for more than 10% of total share capital, he/she cannot hold a proxy for another member in the same company.

Q99: Can one member appoint more than one proxy?

A99: Yes, a person can appoint more than one proxy.

Q100: When can a proxy be appointed? Can a person be appointed as a permanent proxy for a member?

A100: As per the provisions of Section 105 of the CA, 2013, proxy can be appointed by a member any time after the notice is issued, but the same should reach the company 48 hours before the scheduled meeting. A person cannot be appointed as a permanent proxy for a member.

Q101: Can a director appointed as a Chairman at the meeting of the Board for the purpose of convening such meeting be considered as a person holding the positon of Chairman of the Company?

A101: A director appointed as a Chairman at the meeting of the Board for the purpose of convening such meeting cannot be considered as a person holding the positon of Chairman of the company. In case a company is willing to designate a director as Chairman of the company, a separate resolution with this affect is required and the necessary intimations shall be given to the ROC.

Q102: What is the period prescribed for preserving the annual returns prepared under the CA, 2013?

A102: Pursuant to Rule 15(3) of the Companies (Management and Administration) Rules, 2014, the Copies of annual returns prepared under Section 92 and copies of all certificates and documents required to be annexed thereto shall be preserved for a period of eight years from the date of filing with the ROC.

Q103: What are the requirements of signing of Annual Return?

A103: Pursuant to the provisions of Section 92 of the CA, 2013 read with

Rule 11 of the Companies (Management and Administration) Rules,

2014, annual return shall be signed in the following manner:

(i) In case of a Small Company and OPC, the annual return shall be signed by Company Secretary or where there is no Company Secretary, by the Director of the Company.

(ii) In case of other companies, the annual return shall be signed by a Director and the Company Secretary, or where there is no Company Secretary, by a Practising Company Secretary.

Q104: What are the certification requirements of Annual Return?

A104: Pursuant to Section 92(2) of the CA, 2013 read with Rule 11(2) of the Companies (Management and Administration Rules, 2014, the Annual Return of the following companies shall be certified by a Company Secretary in whole time practice in Form No. MGT-8:

Every listed company;

Every company having paid up share capital of INR 10 crore or more;

Every company having turnover of INR 50 crore or more

Q105: Is the extract of the Annual Return required to be attached to

Board’s Report in terms of Section 134 (3)(a) of the CA, 2013?

A105: An extract of the annual return in form MGT-9 relating to the financial year to which the Board’s Report relates shall be attached therewith in terms of Section 134 (3)(a) of the CA, 2013.

Q106: In case the AGM is not held, what is the time limit for filing the

Annual Return?

A106: As per Section 92(4) of the CA, 2013, in case the AGM of a company is not held, the Annual Return has to be filed within 60 days from the last date on which AGM should have been held together with the statement specifying the reasons for not holding the AGM.

Q107: Which registers should include the index of names?

A107: As per Section 88(2) of the CA, 2013, the following registers should include an index of names:

Register of members;

Register of debenture holders; Register of any other security holders.

Provided that an index is not mandatory if the number of members

are less than 50

Q108: What is the duration for preservation of Statutory Registers?

A108: As per Rule 15 of the Companies (Management and Administration) Rules, 2014, the Statutory Registers are to be preserved in the following manner:

----------------------------------------------

Accounts

.

.

Q109: What shall be the first financial year of the newly incorporated company or body corporate?

A109: As per Section 2(41) of the CA, 2013, the first financial year of a company means a period beginning from the date of incorporation and ending on 31 March of the following year.

Q110: In case any existing auditor incurs disqualifications as per the CA 2013, what is the procedure to be followed for appointment of new auditor? Is the company also required to follow the procedures relating to removal of auditor as prescribed in the CA, 2013?

A110: As per Section 141(4) the CA, 2013, an auditor once disqualified shall vacate office and which in turn results in casual vacancy. The casual vacancy can be filled by the board of directors within 30 days of such disqualification and the process relating to removal of Auditors is not required to be followed.

It may be noted that the auditor so appointed holds office only till the conclusion of the next AGM.

Q111: How does the requirement of rotation of auditor apply to a company having a calendar year end or June Year-end?

A111: Appointment/re-appointment of auditor takes place at the AGM and is valid until the conclusion of the next AGM irrespective of the year end. The period of five years will be counted from AGM to AGM.

Q112: Who shall sign the Financial Statements of a Company?

A112: The Financial Statements of a company is required to be signed as per the provisions of Section 134 of the CA, 2013 by:

The chairperson of the company (if he is authorised by the Board) or by two directors (out of which 1 shall be Managing Director/ Chief Executive Officer if any); and

Chief Financial Officer and Company Secretary wherever they are appointed

However, the Companies (Amendment) Bill, 2016 which is yet to be notified, enables Chairperson if he is authorized or two directors out of which one shall be MD, if any and the CEO, the CFO and the

Company Secretary, wherever they are appointed, to sign the financial statements of the company.

Q113: Can a company maintain books of account in any place other than Registered Office?

A113: As per the provisions of Section 128 of the CA, 2013 read with Rule

2A of the Companies (Accounts) Rules, 2014, a company may maintain books of account and other relevant papers may be kept at such other place in India as the Board of Directors may decide and where such a decision is taken, the company shall, within seven days thereof, file with the ROC a notice in Form AOC-5 giving the full address of that other place.

Q114: If the Notice of the AGM is circulated at a short notice, can the financial statements also be sent along with the notice?

A114: Yes, a company holding a general meeting after giving a short notice as provided under Section 101 of the CA, 2013 may also circulate financial statements at such short notice.

However, the Companies (Amendment) Bill, 2016 which is yet to be notified, proposes to enable the Company to send copy of the financial statements at a period lesser than 21 days if 95% of the members entitled to vote at the meeting agrees for the same.

Q115: What is the duration for preserving the Books of Account?

A115: As per Section 128(5) of the CA 2013, the books of account shall be preserved by the company for 8 financial years preceding the financial year.

Q116: Is it required to attach Board’s Report to the consolidated financial statements?

A116: Yes, as per Section 134 (3) of the CA, 2013, the Board’s Report shall be attached to the consolidated financial statements.

Q117: Are the standalone financial statements of the associates/joint ventures required to be placed on the website too?

A117: As per fourth proviso to Section 136(1) of the CA 2013, every company having a subsidiary or subsidiaries shall place separate audited accounts in respect of each of its subsidiary on its website, if any. Therefore, there is no requirement of placing standalone financial statements of associates/joint ventures on the website of the company.

However, the Companies (Amendment) Bill, 2016, inserts the following provisions w.r.t foreign subsidiary.

If a Listed Company which has a foreign subsidiary and:

If the foreign subsidiary is statutorily required to prepare consolidated financial statement under the law of any country, the requirement shall be met if such consolidated accounts are placed on the website;

If the foreign subsidiary is not required to audit its financial statements, the Listed Company may place the unaudited financial statement on its website and if the language is not English, a translated copy of the same shall be placed on the website.

Q118: Can a branch office of the company maintain its books of account in the location of branch office?

A118: Yes, as per Section 128(2) the CA, 2013, the Company may maintain books of account relating to the transactions effected at the branch office at branch provided summarised returns are periodically sent to the registered office.

Q 119: Whether the subsidiary of a company under liquidation is required to consolidate its accounts as per Section 129 of the CA, 2013?

A119: Since the holding company under liquidation is not required to have the accounts prepared as per Section 129 the CA, 2013, its subsidiary company’s accounts shall not be consolidated with the aforesaid holding company. However, the reasons for not consolidating must be explained in the notes as required by Schedule III.

Q120: Is it required to comply with Accounting Standards while preparing the financial statements?

A120: Yes, as per Section 129(1) of the CA, 2013, the financial statements should be prepared in accordance with the accounting standards. Further, as per Section 129 (5) of the CA, 2013, in case of deviation from accounting standards, the financial statements must disclose the fact of such deviation and reasons for the same along with its financial effects.

Q121: What are the modes available for the company to maintain the books of account?

A121: The Company may maintain books of account either physically or electronically. In case the books of account is maintained

electronically, the back-up of the books of account and other books and papers of the company shall be kept in servers physically located in India on a periodic basis.

Q122: Can a company keep the books and registers at a place other than registered office of the company?

A122: Yes, as per Proviso to Section 128 (1), the books may be kept at such other place in India as the Board of Directors may decide after passing resolution in the duly held Board Meeting of the company.

Audit and Auditors

Q123: Which companies are required to appoint Internal Auditor?

A123: As per Section 138 of the CA, 2013 and Rule 13 of Companies (Accounts) Rules, 2014, the following companies are required to appoint an internal auditor:

listed company;

every unlisted public company having at any point of time during the preceding financial year -

o paid up share capital of INR 50 crores or more; or

o turnover of INR 200 crores or more; or

o outstanding loans or borrowings from banks or public financial institutions for more than INR 100 crores; or

o outstanding deposits of INR 25 crore rupees or more

every private company having at any point of time during the preceding financial year -

o turnover of INR 200 crores or more; or

o outstanding loans or borrowings from banks or PFI for more than INR

100 crores

Q124: Who can be appointed as Internal Auditor of the Company?

A124: As per the provisions of Section 138 of the CA, 2013 read with Rule

13 of the Companies (accounts) Rules, 2014, a “Chartered Accountant” or “Cost Accountant” whether engaged in practice or not, or such other professional as may be decided by the Board of Directors of the company can be appointed as internal auditor of the Company. The internal auditor may or may or may not be an employee of the company.

Q125: Can internal Auditor be appointed by way of a circular resolution?

A125: No, as per Section 179 the CA, 2013 read with applicable rules, Internal Auditor shall be appointed at the duly convened board meeting of the Company.

Q126: Can the Statutory Auditor and Cost Auditor be the same person or firm?

A126: As per the proviso to the Section 148(3) the CA, 2013, the person appointed under Section 139 the CA, 2013 as an auditor of the company shall not be appointed for conducting the audit of cost records.

Q127: When should the first auditors be appointed?

A127: As per Section 139 of the CA, 2013, the first auditors should be appointed by the Board within 30 days of the registration of the company and in case of failure of the Board to appoint such auditors, the auditors shall be appointed by the members in general meeting. Further, such auditor shall hold office till the date of the conclusion of the first AGM.

Q128: What is the term of appointment of an individual and a firm as a statutory auditor?

A128: As per Section 139(2) the CA, 2013 read with Rule 5 of Companies (Audit and Auditors) Rules, 2014, the following companies shall not appoint an individual as statutory auditor for more than one term of 5 years and a firm as statutory auditor for more than two terms of 5 year each:

Listed company;

All unlisted public companies having paid up share capital of INR 10

Crores or more;

All private limited companies having paid up share capital of INR 20

Crores or more;

All companies having paid up share capital below the threshold limit mentioned in the aforesaid two points, but having public borrowings from financial institutions, banks or public deposits of INR 50 Crores or more

Q129: Is there any transition period provided for complying with the provisions of Section 139 (2) of the CA, 2013 relating to rotation of auditors?

A129: As per Companies (Removal of Difficulties) Third Order, 2016 dated

30th June, 2016 issued by the MCA, the classes of companies stated under Q128 are required to comply with the provisions of Section

139(2) the CA, 2013 relating to rotation of auditors not later than the

AGM to be held in the year 2017.

Q130: Which are the classes of companies required to comply with the provisions relating to rotation of auditors?

A130: As per Section 139(2) of the CA, 2013 read with Rule 5 and Rule 6 of Companies (Audit and Auditors) Rules, 2014, the following companies are required to rotate their auditors on expiry of the term:

Listed company;

All unlisted public companies having paid up share capital of INR 10

Crores or more;

All private limited companies having paid up share capital of INR 20

Crores or more;

All companies having paid up share capital below the threshold limit mentioned in the aforesaid two points, but having public borrowings from financial institutions, banks or public deposits of INR 50 Crores or more

Q131: In case of Companies which have already appointed auditors in CA, 1956, how should the period of 5 years and 10 years for rotation of auditors be computed?

A131: As per Rule 6(3) of the Companies (Audit and Auditors) Rules, 2014, the period for which the individual or the firm has held office as auditor prior to the commencement of the CA, 2013 shall be taken into consideration for the purpose of rotation of auditors.

For example, in case of listed and prescribed companies, if an individual has completed four years as an auditor on April 01, 2014, he can continue for 3 years in the same company.

Further, if the auditor is required to appointed again, he may do so after the cooling period of five years from the completion of term of five years.

Q132: Can a company remove its auditor?

A132: As per Section 140(1) of the CA, 2013 read with Rule 7 of Companies (Audit and Auditors) Rules, 2014, a company may remove its auditor before the expiry of the term by obtaining prior approval of the Central Government and passing a special resolution in general meeting.

Q133: Is there limit on the number of audits an auditor may undertake?

A133: As per Section 141(3)(g) of the CA, 2013, an auditor cannot undertake audit of more than twenty companies.

In case of private companies, while calculating the limit of 20, one person companies, dormant companies, small companies and private

companies having paid up share capital less than one hundred crore rupees shall be excluded. [Notification No. GSR 464(E), dated 5th June, 2015]

Q134: Who shall fix the remuneration of Auditors?

A134: As per Section 142(1) of the CA, 2013, the remuneration of the auditor of a company shall be fixed in its general meeting or in such manner as may be determined by the Board of Directors, which shall include any out of pocket expenses incurred for the purpose and in connection with the audit. Provided further, that the Board may fix the remuneration of the first auditor appointed by it.

Q135: Is it the duty of the auditor to confirm on internal financial controls?

A135: As per Section 143(3)(i) of the CA, 2013 the auditor is required to state the adequacy of internal financial control systems and its operating effectives.

However, as per the Companies (Amendment) Bill, 2016 which is yet to be notified, it is proposed that the auditors are required to report on Internal Financial Control with reference to financial statements.

Q136: Who shall appoint an auditor of a Government Company?

A136: As per Section 143(5) of the CA, 2013, the auditor of a Government Company shall be appointed by the Comptroller and Auditor General of India (“CAG”). Further, w.e.f. 4th September 2014, auditor of any other company owned or controlled directly or indirectly by Central Government or State Government and partly by Central Government and partly by one or more State Governments shall also be appointed by CAG.

Q137: Which services are not to be rendered by auditor of a company?

A137: As per Section 144 of the CA, 2013, an auditor shall not provide any of the following services:

(a) Accounting and Book keeping services

(b) Internal Audit