Earnings - Savings = Expenses (Right).

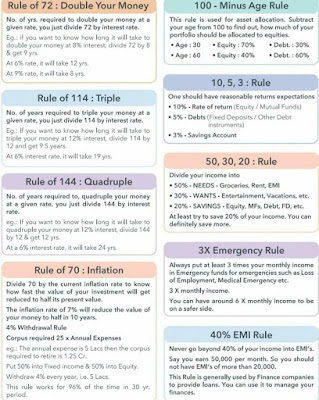

No. of yrs required to double your money at a given rate, U just divide 72 by interest rate

Eg, at 8% interest, divide 72 by 8 and get 9 yrs..so money 💰will double in 9 yes.

At 6%, it will be 12 yrs.

#Rule of 114

No. of years required to triple your money at a given rate, U just divide 114 by interest rate.

For example, if you want to know how long it will take to triple your money at 12%, divide 114 by 12 and get 9.5 years

At 6% interest rate, it will take 19yrs.

#100 minus your age rule

This rule is used for asset allocation. Subtract your age from 100 to find out, how much of your portfolio should be allocated to equities

Age 30

Equity : 70%

Debt : 30%

Age 60

Equity : 40%

Debt : 60%

#40℅ EMI Rule

Never go beyond 40℅ of your income into EMIs.

Say if you earn, 50,000 per month. So you should not have EMIs more than 20,000 .

This Rule is generally used by Finance companies to provide loans.

You can use it to manage your finances.

#Rule of 70

Divide 70 by current inflation rate to know how fast the value of your investment will get reduced to half its present value.

Inflation rate of 7% will reduce the value of your money to half in 10 years.

Twenty Commandments for Personal Finance

Avoid peer pressure

Waren Buffet avoided peer pressure by not staying in posh locality and large bunglow

2. I am quite serious when I say that I do not believe there are, on the whole earth besides, so many intensified bores as in these United States. No man can form an adequate idea of the real meaning of the word, without coming here.

3. I buy expensive suits. They just look cheap on me.

4. I don't look to jump over 7-foot bars: I look around for 1-foot bars that I can step over.

5. I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years.

6. If a business does well, the stock eventually follows.

7. If past history was all there was to the game, the richest people would be librarians.

8. In the business world, the rearview mirror is always clearer than the windshield.

9. It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you'll do things differently.

10. It's better to hang out with people better than you. Pick out associates whose behavior is better than yours and you'll drift in that direction.

11. It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

12. Let blockheads read what blockheads wrote.

13. Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it.

14. Of the billionaires I have known, money just brings out the basic traits in them. If they were jerks before they had money, they are simply jerks with a billion dollars.

15. Only buy something that you'd be perfectly happy to hold if the market shut down for 10 years.

16. Only when the tide goes out do you discover who's been swimming naked.

18. Price is what you pay. Value is what you get.

19. Risk comes from not knowing what you're doing.

20. Risk is a part of God's game, alike for men and nations.

21. Rule No.1: Never lose money. Rule No.2: Never forget rule No.1.

22. Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

23. Someone's sitting in the shade today because someone planted a tree a long time ago.

24. The business schools reward difficult complex behavior more than simple behavior, but simple behavior is more effective.

25. The investor of today does not profit from yesterday's growth.

26. The only time to buy these is on a day with no "y" in it.

27. The smarter the journalists are, the better off society is. For to a degree, people read the press to inform themselves-and the better the teacher, the better the student body.

28. There seems to be some perverse human characteristic that likes to make easy things difficult.

29. Time is the friend of the wonderful company, the enemy of the mediocre.

30. Wall Street is the only place that people ride to in a Rolls Royce to get advice from those who take the subway.

31. We believe that according the name 'investors' to institutions that trade actively is like calling someone who repeatedly engages in one-night stands a 'romantic.'

32. We enjoy the process far more than the proceeds.

33. We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.

34. When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact

36. Why not invest your assets in the companies you really like? As Mae West said, "Too much of a good thing can be wonderful".

37. Wide diversification is only required when investors do not understand what they are doing.

38. You do things when the opportunities come along. I've had periods in my life when I've had a bundle of ideas come along, and I've had long dry spells. If I get an idea next week, I'll do something. If not, I won't do a damn thing.

39. You only have to do a very few things right in your life so long as you don't do too many things wrong.

40. Your premium brand had better be delivering something special, or it's not going to get the business.

excel spreadsheet for this helps a lot, but a simple diary or notebook will

also do. Create an earnings page where you list down all your income sources.

The other page will be your expenses page.

- Where you spent your money?

- When did you spend your money?

- How much did you spend?

- What did you spend it on?

- Was it a need based spend or a want based spend?

needs?

You have a set of assets and liabilities and some assets still to be created.

Now the classic dilemma starts : Clear the old debts or keep them as it is and Invest this amount in a new asset or investment avenue

Psychology plays a part in whatever decision we make, including investment in stocks. Sometime our built in psychology is helpful and many a times it is not. When psychology is not helpful we call them psychology traps. Investment in stocks is also guided by few psychology traps which influences us in making bad investment choices and lose money.

Usually people fall in love with their investment decisions and cling to shares, whose market value has declined and immediate chances of recovery are remote, but will not take decisions either to withdraw or reduce their exposures.

They hold on to this belief that their past decisions of these investments were infallible, and the stocks will turn around. Most investors have such shares in their portfolio, which they keep on clinging to despite making losses with no chances of recovery in foreseeable future.

Remedy from this trap lies in taking a detached view while reviewing the portfolio, basing decisions on market reality and avoiding the ego trip.

Many investors while deciding on a stock, consult fellow investors, and accept such views which approve their own choice and reject the contrary views. Such selective approval often lead to bad decisions, but the investor holds on to it as his/her choice has been confirmed by other investors.

Avoiding such traps will be possible if the investor while seeking approval from other fellow investors should be rationally looking into the background of these investors. Alternately, the investors may take into consideration both supportive and opposing views and then make the decision to invest or not.

Psychological Trap No.4: Copying Mindset

One should, therefore, avoid investment decisions, which are made by blindly following successful investors.

The classic example is of Long Term Capital Management Company (LTCM) which went bust in late 1990s, which was founded in 1994 by John W. Meriwether, the former vice-chairman and head of bond trading at Salomon Brothers. Members of LTCM's board of directors included Myron S. Scholes and Robert C. Merton, who shared the 1997 Nobel Memorial Prize in Economic Sciences.

Various Charges

1) Application Fee: Covers the preliminary expenses of a bank for conducting verification. Rs 1,000-Rs 5,000.

2) Processing Fee: Covers the cost of the credit appraisal. Fee depends on borrower's profile, income and the type of loan. Rs 10,000-1% of loan.

3) Administrative fee: Some lenders split the processing fee into two parts. The one charged after the loan is sanctioned is called admin istration fee.

4) Technical evaluation Fee: For high-value properties, two valuations are done, and the lower of the two is considered for sanctioning a loan. Some PSU lenders charge a fee for doing this evaluation.

5) Legal fee: Most lenders engage firms to scrutinise borrowers' legal documents. Generally, banks include this cost in the processing fee, but some PSU lenders charge it separately.

6) Franking fee on sale agreement: In some states, there is a stamp duty payable on the property agreement with the builder/seller. 0.1% of cost-Rs 20,000.

7) Franking fee on loan agreement: Some states, Maharashtra and Karnataka, for instance, levy a fee on the loan amount. 0.1-0.2% of loan.

8) Notary fee: If you are an NRI, then your KYC and the POA (power of attorney) needs to be notarised by the Indian embassy or a local notary available abroad.

9) Intimation of registration fee: Intimation to the subregistrar's office is a new process. Followed only in Maharashtra. Rs 1,300.

10) Indemnity cost: The borrower needs to indemnify the lender for certain risks, for instance, if the builder faces a delay in receiving an approval or the property tax is yet to be paid fully by the seller, or some other.

11) Adjudication fee: To start the process for a home loan application, if you are the POA-holder of an NRI, the notarised POA needs to be adjudicated here in India before submission to the lender.

12) Fire insurance fee: Most lenders who are into bankassurance insist on this.

13) Documentation fee: For getting the loan agreement signed, getting the ECS mandate activated and a few other formalities, some lenders charge this fee. Rs 500-Rs 2,000.

Refinancing Home loan or simply put balance transfer to new bank

- interest rate (most popular)

- Option of lowering tenure if one has monthly surplus

- Increase the loan tenure to reduce EMI payments

- Shift from floating rate to fixed rate, or vice-versa

- His current EMI = Rs 46,094

- Outstanding principal = Rs 36,34,030

- Outstanding interest payment = Rs 30,37,655

If Mr. Sharma refinances his loan at 10.50 per cent interest rate for the remaining 12 years:

- New EMI = Rs 44,486

- Total interest payments = Rs 27,71,902

- Potential savings = Rs 8,62,128

- Loan amount: EMI payments are a combination of principal repayment and interest paid on the principal amount. So while one opts for the refinancing, it is the outstanding principal that is being transferred. One has to revisit the amortization schedule of the loan to assess the outstanding loan amount and interest paid till now.

- Interest rate: Interest rate is the governing factor in defining the EMI payments. It is important to analyze the beneficial interest rate before refinancing. Generally, it is advisable to continue with the existing loan unless there is difference of at least 0.75-1.00 per cent between the current interest rate and refinancing rate. If there is drop in interest rates is expected in near future, it is advisable to refinance your high fixed rate loans. If you expect rise in interest rates, it is advisable to go for fixed rate refinancing.

- Loan tenure: Loan tenure is inversely proportional to the EMI payments. Higher the loan tenure, lesser the EMIs, and lesser the tenure, the higher the EMIs. Similarly, the total interest paid is directly proportional to the tenure. The higher the tenure, the higher the total interest paid. So if one has an increase in salary, but does not have a substantial amount to go for prepayment, refinancing the home loan at lesser tenure is advisable.

| ||||||||||||

| ||||||||||||

| ||||||||||||

| ||||||||||||

| ||||||||||||

The Actual Period

|

The 44 (or 55) days begin at the start of your statement period and end when your payment for that purchase is due. In total, this interest-free period is made up of the monthly statement period plus the time you get to pay your statement balance.

|

When To Start

|

Get a longer interest-free period by making purchases at the start of your statement period.

|

How To Keep It Going

|

Always pay your closing balance in full by the due date to avoid interest charges and retain your interest-free period in the next statement cycle. If you choose to rotate the balance by paying minimum due amount, you may not get interest free period on further payments

|

Person Specific

|

Each person’s statement cycle is different. Check yours to see when your month begins.

|

Paying your bill regularly is a good thing, but paying only the minimum due is not. It casts doubts about your financial stability.

Maxing out your Credit limit

It’s ideal not to use more than 60% of your credit limit. If you max out your credit, it’s taken as a sign that you rely too much on credit.

Skipping payment due to a dispute

If there’s a dispute regarding some charges, don’t skip paying the bill. It spells double trouble! Once the dispute is settled, the Credit Card issuer will reverse the disputed amount to your account.

Rejected Applications

If your Credit Card application gets rejected for whatever reason, especially more than once, it will damage your Credit Score. So, make sure you provide the correct information to avoid rejection.

In the year 2020, market regulator SEBI issued guidelines to make multi-cap funds more true-to-label by enforcing minimum exposure to large, mid and small-cap stocks. While a few AMCs (asset management companies) adjusted their multi-cap funds as per the mandate, several converted their existing multi-cap funds to flexi-cap schemes so that they could continue with their large cap-heavy portfolio allocations. As of end-April 2021, the market had around 25 flexi-cap funds with Rs 1,59,480 crores of AUM, and 12 multi-cap funds with Rs 19,846 crore in AUM.

New fund offers in both, multi and flexi-cap schemes, have continued to hit the market as AMCs try to ensure their presence in both categories. With both fund categories designed to invest across large, mid and small-cap funds, differentiating between multi and flexi-cap schemes can seem like a confusing task for retail investors.

Is it only a difference of the degree to which each invests across market capitalization? How large can this difference be? And what can be the possible impact on risk and return?

The capitalisation spectrum

The mid and small-cap segments in the capital market offer a larger universe of less-discovered stocks to choose from. This means two things: 1) fund managers have greater scope to use bottom-up strategies to identify potential winners and, 2) these segments of stocks can face liquidity issues as they may not be frequently traded.

Another important aspect is the ‘beta’ of mid and small-caps. Mid and small-caps can be disproportionately impacted by market movements, which means they are usually more volatile than large cap stocks. Because of these characteristics, investing in mid and small caps is considered a relatively high risk-high reward venture, requiring a long-term mind set.

The difference between multi-cap and flexi-cap funds

The key difference between multi and flexi-cap funds is of the degree to which they are exposed to mid and small-caps. More importantly, this difference can become quite large depending on market conditions. Flexi-cap funds can dial down their exposure to mid or small caps right down to zero, if the fund manager deems it necessary; however, in the case of multi-cap funds, this exposure can never go below 25 percent each for mid and small-cap stocks.

To understand this better, let’s look at the SEBI mandated difference as well as the actual current portfolio allocation of multi and flexi-cap funds.

Current Market Cap Allocation in Multi and Flexi-cap Funds

The allocation chart clearly shows that, on average, flexi-cap schemes are currently maintaining a large-cap heavy allocation, while multi-cap funds are focusing on small cap stocks to generate alpha.

Deciding suitability

In our view, both fund categories have a clear mandate, and will adopt distinct strategies to cater to investors with different risk profiles and return expectations.

The multi-cap category offers fund managers the scope to showcase their stock-picking skills and the potential to create alpha. The mandatory exposure across capitalisation does, however, pose a risk – the fund manager has limited scope to reduce exposure to any segment of market cap that is expected to do poorly at any point in time. The onus of managing the liquidity challenges that come with investing in small-cap stocks is on the AMC and its risk management frameworks.

Investors who are happy with a fixed allocation as their optimum exposure across capitalisation, and have a relatively high risk appetite can consider multi-cap funds. These investors would also need to have a longer investment horizon to allow for the fund’s strategies to bear fruit.

The flexi-cap category does not have any fixed minimum allocation across market capitalisation, making the fund manager’s conviction and skill at judging the right allocation important. The fund manager evaluates the growth potential of different companies, regardless of their market cap and invests in them. Flexi-cap managers can track when a particular market segment has become unattractive, and change the allocation to an alternative market segment that has performed well recently.

Investors who prefer flexible exposure across market capitalisation can thus consider flexi-cap funds. However, they should evaluate whether the fund is managed dynamically according to the prevalent opportunities in the market, and has delivered consistent performance that can meet their investment goals.

You have worked for money and accumulated a sum, now let the money work for you

While the prospect of further rate cuts by the RBI are boosting sentiments in the stock and bond markets, it is also making traditional fixed income investors nervous. Sooner or later banks and other institutions will bring down the rates on offer, signalling an end to near double-digit rates you are enjoying on various deposits at present. But there are ways to side step the rate cuts and continue enjoying higher returns for some more time.

Lend to corporates While bank fixed deposits and recurring deposits would be the obvious choice for many, those with a slightly higher risk appetite and looking for a higher yield may opt for any of the corporate fixed deposits or debentures available. Experts reckon investors can lock in to current high yields before rates on these instruments also start going down. Vivek Rege, MD, VR Wealth Advisers, says, "In the midst of falling interest rates, you may not get such opportunities for a while." For instance, investors can get anywhere between a 50-200 bps (0.5%-2%) higher yield on the range of company FDs, compared to traditional bank fixed deposits. Fixed deposits from non-bankingfinance companies (NBFCs) are offering 9.5% to 11% for three year tenure under the non-cumulative interest payout option (See chart). Certain manufacturing companies are offering slightly higher coupon rates, in the region of 12% on three-year fixed deposits. The interest earned on these company deposits is taxable at the rate applicable to your income tax slab. If corporate FDs are not your cup of tea, you may consider putting your money in non-convertible debentures. Although there are hardly any fresh issues in the market currently, you can purchase any of the existing instruments listed on the stock exchange. Make sure toinvest only in those instruments which are not maturing within the next one or two years. Since rates are expected to fall quite a bit in the coming year, opting for a NCD which will mature only 12-18 months from now will expose you to reinvestment risk, where you will be forced to park the maturity proceeds at a lower rate. For instance, Shriram Transport Finance NY bonds offering a coupon rate of 11.25% under the cumulative payout option has a residual maturity of 1.52 years. The yield-to-maturity (YTM) on these bonds is 10.6%. On the other hand, the Shriram Transport Finance NU bonds with same coupon have a residual maturity of 2.55 years. They are currently offering a YTM of 10.72%.  A big benefit of opting for NCDs is the possibility of capital appreciation in these instruments as the rates fall. This offers you a chance to sell them at a profit, instead of holding on to them till maturity. Raghvendra Nath, MD, Ladderup Wealth Managment, says, "With bond yields likely to come off by 1-1.5% in the coming months, investors could fetch decent capital gains on their NCD holdings." Besides, NCDs are a tax-efficient option as these are eligible for long term capital gains after one year. This means your gains will be taxed at a lower rate of 10% instead of at the rate corresponding to your income tax slab. However, the interest curearned on these NCDs will be taxable as per the tax slab of the investor. Keep in mind though that these NCDs are not easily tradeable despite being listed on the exchanges. As Nath says, "Liquidity can become a constraint for retail investors in NCDs." The trading volumes in some cases are very low, which makes it difficult for the buyer or seller to enter or exit at the desired price point. So you may end up buying at a higher price and selling at a much lower price than what you were looking for.

Credit quality is crucial

In both cases, investors must give due importance to the credit quality of the issuer. While your bank fixed deposits offer the highest degree of safety, company FDs and NCDs carry a much higher degree of risk as these are unsecured instruments. Invest only if you are convinced that the issuing company's financials are strong. Rege cautions, "Do not get swayed by the higher yield. Ensure the company's business model and financials are on a strong footing." This can be gauged from the credit rating assigned to the paper by the rating agency. 'AAA' or similar rated papers offer highest degree of safety, but fetch lower return. 'AA' and lower rated papers come with attractive coupon rates, but imply a higher degree of risk.

Investors need to be careful especially when dealing with some lesser known names in the manufacturing space. Nath reiterates, "You may take a call on lower quality paper provided you are dealing with marquee names in the manufacturing space, which boast of sustainable business."

By Sanket Dhanorkar, ET Bureau | 9 Feb, 2015,

|